APA

ISO 690-2

Harvard

Haga clic en un formato de citación

Advisors in Corporate Governance of Family Firms*

Consultores em Governança Corporativa de Empresas Familiares

Cuadernos de Administración, vol. 34, 2021

Pontificia Universidad Javeriana

Maria-Andrea Trujillo a maria.trujillo@cesa.edu.co

Colegio de Estudios Superiores de Administración (CESA), Colombia

Maximiliano González

Facultad de Administración, Universidad de los Andes, Colombia

Alexander Guzmán

Colegio de Estudios Superiores de Administración (CESA), Colombia

Received: 16 September 2018

Accepted: 22 June 2021

Published: 15 October 2021

Abstract:

This study examines how specialized advisors impact the implementation of good governance practices at the firm and family level. We applied a qualitative case study approach using four cases in four different industries with diverse levels of management sophistication. This revealed that firms’ governance structure outputs, such as a board of directors and general shareholder meetings, and the family governance outputs, for instance, family protocols and family councils, substantially improve with an advisors’ intervention. We highlighted the important but seldom studied in the academic literature of advisors’ role in designing a better governance structure at the business and family level and its implementation. We also stressed the importance of building confidence, transparency, and trust between the advisor and the family.

JEL Codes: G30, G32.

Keywords:Family firms, corporate governance, family governance, advisors.

Resumen:

Este estudio examina el impacto de los asesores especializados en la implementación de prácticas de buen gobierno a nivel de empresa y familia. Aplicamos un enfoque cualitativo de estudio de casos en diversas industrias con diferentes niveles de sofisticación en la gestión. Los hallazgos muestran que los resultados sobre el gobierno corporativo de las empresas como la junta directiva y las asambleas generales de accionistas, y los resultados sobre el gobierno familiar como los protocolos familiares y los consejos familiares, se robustecen sustancialmente con el acompañamiento de asesores. Destacamos la importancia, pero rara vez estudiado en la literatura académica, del papel de los asesores en el diseño de una mejor estructura de gobierno a nivel empresarial y familiar y su implementación. También enfatizamos la importancia de generar seguridad, transparencia y confianza entre el asesor y la familia.

Códigos JEL: G30, G32.

Palabras clave: Empresas familiares, gobierno corporativo, gobierno familiar, asesores.

Resumo:

Este estudo examina como os consultores especializados impactam a implementação de boas práticas de governança corporativa e familiar. Aplicamos uma abordagem qualitativa de estudo de casos usando quatro casos em quatro indústrias diferentes, com diversos níveis de sofisticação de gestão. Isso revelou que os resultados da estrutura de governança das empresas, como um conselho de administração e assembleias gerais de acionistas, e os resultados da governança familiar, por exemplo, protocolos de família e conselhos de família, melhoram substancialmente com a intervenção de consultores. Destacamos o importante, mas raramente estudado na literatura acadêmica, do papel dos consultores na concepção de uma melhor estrutura de governança corporativa e familiar e sua implementação. Também enfatizamos a importância de construir segurança, transparência e confiança entre o conselheiro e a família.

Códigos JEL: G30, G32.

Palavras-chave: Empresas familiares, governança corporativa, governança familiar, consultores.

Introduction

Corporate governance seeks to reduce the risk of losses for all the stakeholders in a specific firm (Shleifer & Vishny, 1997; Tirole, 2001). There is an incorrect assumption that such practices are unnecessary for small and medium-sized family firms, even though agency problems may reduce their likelihood of survival. Block (2012) asserts that the issues that arise in family businesses - sibling rivalry, the desire of children to be different from their parents, marital problems or differences in objectives related to the development of the company - increase conflicts of interest, hinder the coordination of management teams and lead to decisions that are not optimal (Dyer, 1994; Schulze, Lubatkin, Dino et al., 2001, Schulze, Lubatkin, & Dino, 2003; Eddleston & Kellermanns, 2007, Villalonga, Amit, Trujillo et al., 2015).

Multilateral agencies have highlighted the relevance of good governance practices for economic development in Latin America, recognizing its importance for large, listed firms, and for small and medium-sized, closely-held and family-owned enterprises, which represent the largest proportion of firms in the region. Hence, although seldom studied in the academic literature, the role of advisors is of particular relevance because they can serve as a bridge between small and medium-sized firms and corporate governance best practices, specifically in emerging economies (Reay, Pearson, & Gibb, 2013). The main contributions made by advisors are commonly in strategic advice, networking, and their role as coach or mentor of the family.

Our approach, sought to highlight how small and medium.sized family firms develop good governance practices through a qualitative case study. In particular, we assessed the different ways advisors in a firm help to mitigate agency problems. We conducted in-depth interviews with the advisors and managers of four firms. The role of advisors in this process is crucial given that they bring to the table expertise and skills not necessarily present in small or medium-sized firms. This paper aims to contribute to the unexplored field of advisors’ services to family firms (Strike, 2012). Based on the need to explore these contributions in more detail, this paper aims to offer an understanding of the value added of advisors in the implementation of good governance practices and their outcomes both at the firm level and at the family level.

Our findings indicate that managers perceive that firms’ governance structures improved significantly and that the support of the advisors was a key factor for understanding what corporate governance means and for the identification and implementation of various governance mechanisms, such as a board of directors and general shareholder meetings. At the family front, the advisory process we studied also generated measurable outputs such as family protocols and councils. These cases suggest that advisors play a vital role in guiding and supporting companies wishing to overcome structural problems and implement good governance practices at the firm and family level.

This paper contributes to the literature on family firms in several ways. First, although the cases are restricted to Colombia, our paper facilitates a better understanding of the relevance of corporate governance on family firms elsewhere. Second, the cases here demonstrate how advisors represent a bridge between policymakers and agencies that promulgate good governance standards and codes and the firms called to implement them. Finally, we highlight the importance of building confidence, transparency, and trust between the advisor and the family to obtain the desired corporate governance outcomes.

The organization of this paper is as follows. The following section presents the theoretical framework. The second section briefly describes the methodology and the family firms involved in this study. The third section discusses the progress achieved by these firms with support from the advisors on their boards and general meetings of shareholders. The fourth section brings to the discussion advances regarding family governance practices on these firms. The last section presents a final comment.

Corporate governance implementation: The strategic role of advisors

The role of advisors is vital in family businesses, but little is known from the academic literature on what works and what does not in terms of advisory intervention (Astrachan & McMillan, 2006). Strike (2012) divides the academic discussion on how advisors influence corporate governance in family firms into five dimensions: type of advisors (formal versus informal); specific attributes of the advisors such as trustworthiness, commitments, and competence; the process of choosing the correct advisors; the process of advising, in terms of types and length of interventions and different advising models; and the outcome of the advisory process.

In this paper, we focus our analysis on the outcome of the advisory process. As in the other dimensions, there are only a few published papers that specifically analyze these outcomes. Following Strike (2012), our discussion is organized around the outcomes discriminating between firm outcomes and family outcomes.

Firm outcomes

The general shareholder assembly is the principal governing body in any firm. Apostolides (2007) argues that the general meeting of shareholders should be structured around three specific functions: legal formality in terms of approval of proposals can be implemented only with majority shareholder approval; communication that informs shareholders regarding the company’s financial results and other relevant aspects; and accountability in terms of the response of senior management and the board of directors to shareholder concerns. Several authors have highlighted these functions, including Lawton & Rigby (1992) and Strätling (2003). Assemblies play a crucial role in firms seeking to professionalize their governance practices.

The operational arm of the general shareholder assembly is the board of directors. This body is designed to control top management and ensure that shareholders’ wealth is maximized. Fama (1980) stresses the importance of having independent and external board members who can serve as professional referees that have no working relationships with the company and with no relation to the shareholders. Fama & Jensen (1983) again argue that boards should be composed of experienced professionals but must also include managers of the company to make the most of internal information flows and facilitate decision-making.

External directors play a dual role on the board. In addition to protecting the interests of shareholders, they advise managers during the decision-making processes (Villalonga, Trujillo, Guzmán et al., 2019; Bennedsen, 2002). For example, Barbera & Hasso (2013) posit the importance of having external directors verify and validate a firm’s results. This paper shows that for small and medium-sized firms, the hiring of external directors increases the likelihood of steady sales growth and survivability.

The role of advisors in setting and improving these governing bodies has proved essential in family firms. Strike (2013) and Michel & Kammerlander (2015) point out the importance of the ‘most trusted advisor’ in the context of the family firm board of directors. Adendorff, Boshoff, Court et al. (2005) argue that these advisors’ principal role is to disentangle family goals to business goals. In this regard, Blumentritt (2006) shows that an advisor’s presence in the board of directors significantly increases strategic planning. Another outcome usually mentioned in the literature regarding advisors is the diversity of knowledge that elevates advisors into the decision-making process (Mustakallio, Autio, & Zahra, 2002).

Another dimension discussed is how advisors on the board could mitigate the influence of the firms’ founder. Although the empirical evidence is not conclusive in this matter (Feltham, Feltham, & Barnett, 2005; Fahed-Sreih & Djoundourian, 2006), advisors, in fact, provide different visions and bring diverse experience and expertise to the board discussion. Boards also benefit the founder who wishes to relinquish the company as a family legacy because a robust governance structure will allow descendants to lead the business efficiently.

Family outcomes

Agency problems exist not only within family businesses but also within the family itself. Just asking a family member if the business is facing difficulties or conflicts of interest involving the family, the answer will invariably be yes. Schulze et al. (2001) present problems typical in family businesses, along with features that make it challenging to implement mechanisms that could be easily incorporated into the governance structures in other types of companies. For example, founders have a propensity to give their children important economic benefits, including allowing them to hold managerial positions in the business even if they are not suited for them. In addition, middle managers who do not belong to the founding family and aspire to occupy a higher position thanks to their good performance will seek employment in non-family firms.

Additionally, Schulze et al. (2001) highlight different theoretical contributions under which altruism by parents can encourage opportunistic behavior by children, which affects the economic welfare of the entire family. According to these authors, a typical family business gives family members job security or employment assurance, regardless of their performance, as well as other benefits that they would not receive in another company. For Schulze et al. (2001), good corporate governance practices are necessary for family businesses as in companies with a dispersed ownership.

Schulze et al. (2003) indicate the existence of conflicts of interests in family businesses run by second-generation family members. When ownership is concentrated within a few relatives (siblings or children of the founder), different governance problems arise. For example, given that the relative in a management position is generally not the founder or head of the family, it may be harder to obtain the support of senior family executives regarding investments or opportunities they consider beneficial to the company. In addition, the family manager may exacerbate family conflicts by promoting their children and spouse first, rather than the children and spouses of the other owners. Furthermore, members of the third generation may also want to enter the company. Equal shareholding between different siblings can lead to struggles for corporate control, generating political maneuverings and escalating family disputes. All this can have undesirable consequences on investment decisions and corporate finance.

Block (2012) argues that only moderate coordination problems in companies with a founder CEO may occur because there are fewer information asymmetries or differences between the founder and the management team. However, the issues outlined by other researchers (Dyer, 1994; Schulze et al., 2001, 2003; Eddleston & Kellermanns, 2007) –such as sibling rivalry, generational conflicts, marital problems, and differences regarding the objectives related to the development of the company– hinder coordination with management and lead to decisions that are not optimal.

Conversely, some actions can mitigate agency conflicts within families and facilitate the positive effect family members can have on their businesses. Eddleston & Kellermanns (2007) show that families may affect the sustainability of their businesses either positively or negatively. The difference lies in the relationship established among the family members; some have troubled relationships while others develop participatory strategic processes that can lead to a culture of cooperation and collaboration in decision making. Eddleston & Kellermanns (2007) suggest that transparency and the establishment of participatory mechanisms can mitigate conflicts of interest in family firms.

Just as business growth leads to establishing governing bodies such as boards to facilitate the management of complex organizations, the growth of founding families makes it necessary to implement mechanisms to manage conflicts of interest related to the business. Leon-Guerrero, McCann, & Haley Jr. (1998) found that business practices focused on families are related to generational changes. For example, adopting protocols or family mission statements, family councils, training family members for positions in the company, and prenuptial agreements are more closely related to the number of generations in the family than to company size measured by sales.

Martin (2001) points out the relevance of another governing body in family businesses; the annual family meeting or assembly, to address purely family matters. However, issues related to family and business can be discussed if there is no family council. Nevertheless, the family assembly aims to preserve unity and communication between family members, creating opportunities to share and enjoy the bonds of relationships. Martin says that families in a multigenerational stage require an additional formal structure, such as the family council, to handle family-business relationships. The councils offer opportunities to discuss company results, the appointment of family members to the board, and training strategies for the younger generation. According to Heck, Hoy, & Poutziouris (2008), optimal integration of family and business is a major issue for family firms, and the family council is a helpful governance body in this regard.

Family assemblies are meaningful to the extent that they include all founding family members, which the council cannot and should not do. Blumentritt, Keyt, & Astrachan (2007) highlight how the family council represents the family, regulates family affairs, sets policy or family protocol, and sometimes works on decisions pertaining to the distribution of wealth through social initiatives.

Assemblies and family councils play a crucial role in determining strategy and business competitiveness. A vision shared by all family members connected with the company leads to better strategic decision-making and better economic performance (Mustakallio et al., 2002; González, Guzmán, Pombo et al., 2012). However, such a vision involves a high level of social interaction among family members and becomes difficult as the family grows and covers two or more generations. The use of family institutions such as informal meetings, assemblies, and family councils integrates the needs of the founding family and connects family members with the company. In this matter, advisors could serve as agents that put on the table issues and different opinions among family members and, more importantly, set goals and compromises (Lane, Astrachan, Keyt et al., 2006; Thomas, 2002; Sorenson, 1999).

Another important instrument of governance in family businesses is the family protocol (Guzmán, Trujillo, del Hierro et al., 2020). For Blondel, Carlock, & Heyden (2005), the development of a book of rules and guidelines for family businesses clarifies the family’s behavior in relation to their company. It facilitates a decision-making process and consistency that adheres to parameters of justice.

Usually, all these mechanisms, such as family assemblies, councils, protocols, and succession plans, are designed and implemented by professional advisors. Advisors will press to generate a better family environment that fosters the creation of business opportunities in a healthy family environment (Kaye, 1998). They could help families manage family conflicts (Swartz, 1989), but of course, this intervention is not necessarily in the absence of resistance from the family-CEO or some family members (Poza, Hanlon, & Kishida, 2004). Measurable outcomes in this regard include fewer family conflicts and increased trust among family members (Jaffe & Lane, 2004).

In the context of trust, it is easier for families to discuss important issues such as succession plans, family protocols dealing with delicate matters such as retirement, sibling’s business relationships, and financial decisions (González et al., 2013, 2014), among others. We know very little about how advisors influence the outcome of these crucial issues in the family-business relations (Astrachan & McMillan, 2006).

Voordeckers, Van Gils, & Van den Heuvel (2007) find that family firms approaching a generational change are more likely to have outside directors because of the added value that outside directors deliver in a succession as advisors or arbitrators. However, Bartholomeusz & Tanewski (2006) find that family firms are likely to have a lower proportion of independent directors on their boards because families maintain a close position of control with little opportunity for external discipline. In another paper, Salvato & Corbetta (2013) state that advisors can significantly improve the process of succession by taking a decisive role in advising and mentoring the founders’ heirs.

Cases of study and methodology

Building on efforts at the regional level, the Superintendence for Commercial Societies (SSOC)1 began implementing good governance practices for privately held firms in Colombia. In 2009 the SSOC, Confecámaras, and the Bogotá Chamber of Commerce developed the Guide to Colombian Corporate Governance for Closely-Held and Family Firms. Subsequently, Confecámaras and the Chamber of Commerce of Bogotá worked to execute these practices in some selected firms. Among the actions undertaken was the Corporate Governance Training Program for advisors that began in 2010. The program selected a team of advisors through a rigorous process to implement these practices. This section describes the firms whose experiences are highlighted in this paper and the case study methodology (the Appendix has detailed information about this program and its background).

Cases

We chose four family firms, pioneers in the implementation of good governance practices, as our research subjects. Following Eisenhardt’s (1989) and Creswell’s (1998) proposals, we limited the number of cases to four. Multiple cases allow wider exploring of research questions and theoretical evolution (Baxter & Jack, 2008; Eisenhardt & Graebner, 2007; Stake, 1995). According to Eisenhardt (1991), the amount of a case study depends upon how much new information the cases bring and how much is known. And Dyer & Wilkins (1991) state that the page length, the number of cases or the length of the researchers’ stay in the field per se, is not the key issue. The important issue is instead if the researcher is capable to describe and understand the context of the scene in question so well that the context can be understandable to the reader and to produce theory in relationship to that context. Several family business studies employed the case method, among them Dunn (1999); Dyck, Mauws, Starke et al. (2002); Miller, Steier & Le Breton-Miller (2003); Lambrecht (2005) and Cater & Justis (2009).

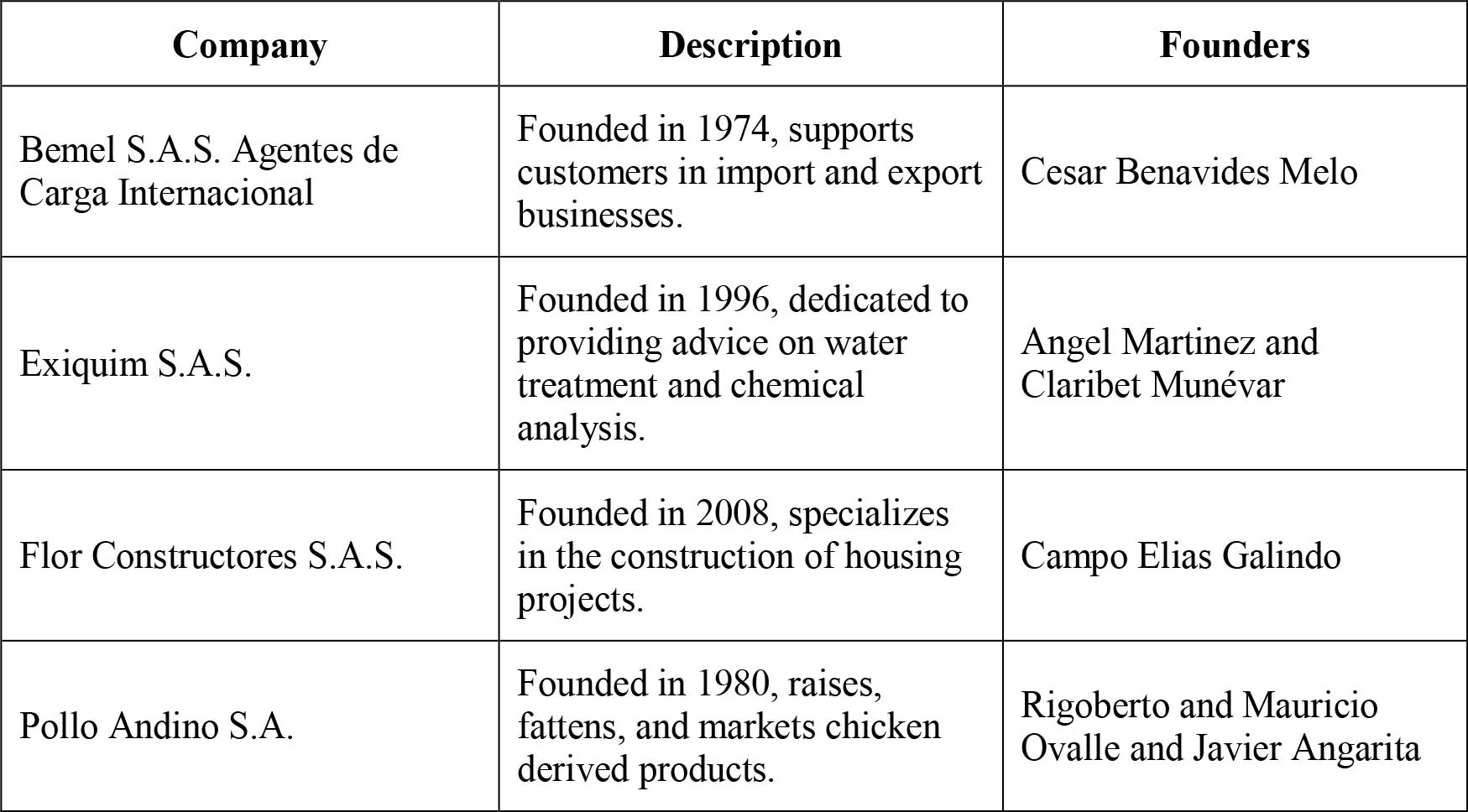

We interviewed five family business owners (four of them acting as managers) and two consulting teams advising these four family firms. The firms belong to different industrial sectors, including a supplier on water treatment and chemical analysis, a construction company for housing projects, a maritime transportation business, and a poultry company. These firms shared locations in Bogotá, but two have expanded to other regions. The companies were founded between 1974 and 2008, as presented in table 1.

Case study approach

Since we are building our work through the case study methodology using four firms, it is important to highlight that this method does not seek to provide “proof” of specific hypotheses, nor empirically validate theoretical postulates. Here the goal is to validate our ideas conceptually, using what we have learned from these cases.

Yin (2003) put it in this way:

A common concern about case studies is that they provide little basis for scientific generalization […] case studies, like experiments, are generalizable to theoretical proposition and not to populations or universes. In this sense, the case study, like the experiment, does not represent a “sample,” and in doing a case study, your goal will be to expand and generalize theories (analytic generalization) and not to enumerate frequencies (statistical generalization) (Yin, 2003, p. 10).

Howorth & Ali (2001) point out that case study research supports researchers in answering how and why questions, using the reference point of involved actors, instead of using predetermined solutions imposed by the researchers.

The primary data collection method involved in-depth interviews, supplemented by observation of the participants and a review of the company documents.

In-depth interviews

In-depth interviews are one of the most common methodologies in the qualitative field. At present, it is used in such diverse areas as sociology, psychiatry, and social sciences. Several disciplines have relied on in-depth interviews as a methodological tool with a high degree of rigor to collect evidence that underpins the object of study. For Brinkmann & Kvale (2015), interviews are intentional conversations or an “interchange of views between two persons conversing about a theme of mutual interest” (p. 4). An interview aims to build a narrative from the opinions, motivations, and experiences of respondents. This allows an understanding of their vision of the world, with context and interpretations based on their knowledge. Tracy (2020) states that those conversations require strategic thinking and planning to ensure useful and quality data and avoid bias in terms of who conducts the conversation. Hence, we created a semi-structured interview with a flexible guide of questions to stimulate discussion rather than dictate it. This approach encourages interviewers to listen, reflect, adapt to dynamic conditions, and sometimes control the conversation with the interviewee. Among the advantages of semi-structured interviews are that they allow emergent understandings of the main topics and mitigate the possible constraints embedded in a rigid script. This allows a collaborative scenario rather than a formal question-answer protocol.

In this part of the study, we were focused on respondents’ perceptions about the process of advisory in corporate governance. Specifically, we wanted to explore how family firms and advisors perceive the key issues regarding implementing good governance practices. For each one of our subjects, we asked open-ended questions concerning the individual, the company, and the involvement of the family and advisor teams in the implementation of good corporate governance practices.

Our discussion guide with the firms’ management was structured with the following questions: (i) How important was the role of advisor, if any, in implementing corporate and family governance structures and mechanisms? (ii) What specific inputs from the advisors were crucial to create or strengthen governance bodies such as the general shareholder assembly and board of directors? (iii) What is the role, if any, of external directors on the board? (iv) What family governance mechanisms were implemented following the advisory process? (v) What value at the firm and family level was created? (vi) What role did the advisor play, if any, in the design and the implementation process of these governance mechanisms at the firm and the family level?

The interviews with the advisors were more general and open because our intention was to learn their perception on family openness and willingness to adopt these governance practices and the outcomes in the advisory process.

Although the scripts are the baseline for the interviews, at the outset of the interviews, following McCracken (1988), who recognized the importance of knowing about the person behind a company position, aspects associated with their careers, their role, and tenure in the firm, and even some of their considerations about their present situation, among other inquiries, we asked grand tour questions, to set up the interview environment.

As a summary, we conducted ten semi-structured interviews, four of them with top-level corporate managers and some family members, and six interviews with advisors. The interviews lasted between 60 and 90 minutes, were conducted in person, and were backed up by note-taking.

Firm governance

This section highlights how the support from advisors was instrumental in setting up good corporate governance practices at the firm level, traditionally associated with larger corporations. In this section, we focus on the primary outcomes of the advisory process at the firm level: board of directors and general shareholder meetings.

Boards

While recognizing the importance of the board of directors, three family businesses were able to create boards with the support of the advisors under the corporate governance program. For example, Bemel established its board of directors with the founder as chairman, one of his sons, and one external member. This is consistent with the recommendation of Salvato & Corbetta (2013), where the ‘temporary share leadership’ is an important management strategy to increase the probability of success in this transition and to have a better and more formal governance structure. So far, management perceives that the board has two main functions: advising and supervision.

In the case of Flor Constructores, the board was established with four members of the family and one external member. Board members are appointed for up to three years, and the board composition is planned to be reviewed annually. In the second stage following the first three years, the board will consist of two external members and three shareholders. Manuel Galindo, the manager of the company and son of the founder, is not a member of the board. He states that the support provided by the board has been valuable for decision-making. In addition to advisory functions, the board has oversight of his duties.

The process at Pollo Andino has been similar to that of Bemel and Flor Constructores. When the three founders decided to hire an external manager and leave their positions within the company’s senior management, it became desirable to establish a board. This governing body was created immediately after the family protocol was implemented; a document that will be discussed in the following section. According to its advisor, it is recommended to have the founders participate in the board after their retirement because the management team and the board itself could benefit from their experience, expertise, and knowledge in the decision-making process. In this case, Rigoberto Ovalle, a founder of the firm and former financial manager before he retired, was appointed as chair of the board along with two other founders an external expert on business strategy, and an external advisor. They later extended the number of seats to include an external marketing expert. Another feature of Pollo Andino’s board of directors was the occasional presence of heirs in board meetings (with no voting power). External members have expressed satisfaction with the thoroughness of the current work performed by the board. This provides evidence that the quality of the services provided through diverse board composition is much richer and more valuable than a more homogenous group (Su & Dou, 2013).

As for Exiquim, the company has never had a board, and its corporate regulations do not require to have one. However, its founders and managing partners have changed their perception of this governing body following the advisory process to implement good practices. Previously, they viewed boards as merely a mechanism for monitoring a manager without an ownership stake in a company, a situation that did not reflect the reality of their business. Nevertheless, the founders, Angel Martinez and Claribet Munévar are now aware of the advisory role that a board can play. For example, the board may be the ideal setting for getting other family members involved in the company, especially members of the second generation, as recommended in Salvato & Corbetta (2013).

Annual general shareholders meetings

Before the advisory process, Cesar Benavides, the founder of Bemel, and his sons usually discussed business issues that are typically part of the general shareholder assembly, such as year-end financial results, risks, and other strategic issues, in an informal way during family meetings. Currently, they initiate formal general shareholder assembly protocols to help focus the discussion on strategic issues, auditor’s reports, dividend policies, potential risks, among others. The general assembly is now a formal governance body that has gained legitimacy and importance in the firm, which is consistent with Strike (2013), Michel & Kammerlander (2015), and others that highlight the relevance of this governance body shaping actions and decision in the context of family firms. In addition, through this process, the general assembly of shareholders is endowed with all due formality. Today the company has high standards of disclosure, especially for shareholders. For management control, they use tools such as balanced scorecards and rigorous follow-up to the company’s strategic planning, which is consistent with the idea of Reay et al. (2013) that advisors could serve as a bridge between state-of-the-art management tools and day-to-day decision-making.

A similar process was in progress at Flor Constructores where management was preparing the first annual shareholder assembly following the corporate governance consulting process. The manager, Manuel Galindo, considered the assembly important for several reasons. The agenda included, for example, financial statements for the closure of all the projects completed over the past two years, improving corporate transparency. Together with the accountant, the manager performed a comprehensive review and clarification of the figures. The company was also planning to elect an auditor for the first time. Other vital decisions involved changes in the firm’s ownership structure, which included opening the equity to new shareholders, and regulating the function of the board.

The cases of Pollo Andino and Exiquim are rather particular. Pollo Andino’s founders had the policy to avoid at all costs the involvement of their families in the company’s day-to-day activities. However, after this corporate governance advising process, they were open to establishing specific protocols to allow family members to participate in the company. Now, members of the founding families are invited to the shareholders’ meetings organized after the consulting process.

For Exiquim, the only family members are the founders and their children. Nevertheless, their prior experience in large companies motivated them to have the shareholders’ meetings conducted with all the necessary legal requirements and not just as another formality. The founders have been very diligent throughout the entire process of organizing the general shareholder assemblies. At the last meeting, the shareholders (the founders and their children), the auditor, and two external advisers in corporate governance were present.

Hitherto, we have highlighted the progress of four family firms regarding the outcomes of traditional bodies of corporate governance - boards of directors and general shareholders meetings. However, family firms have characteristics that differentiate them from other companies, and there are governance bodies explicitly designed to mitigate agency problems within family businesses. Therefore, other important outcomes of this advisory process refer to family governance.

Family governance

The previous section highlighted the importance of the implementation of specific governance mechanisms at the firm level. Herein, we stress the changes made at the family level.

Exiquim

According to the in-depth interviews, the main contribution of this advisory process for Exiquim founders is strengthening strategic planning and work/family relationships. Before the consultation process, the heirs of Angel and Claribet had not had any contact with the company. The advisors decided to mediate, seeking to create awareness with the heirs about managing a family business. The consulting program enabled the founders to instigate succession planning. It has also led to an orderly involvement by the children, who now show an interest in the family business.

Exiquim currently implements corporate and family governance mechanisms as suggested by the family firm literature. They developed a family protocol, which included guidelines for forming the family assembly and family council and clear policies about family involvement in company management. Family assembly seeks to maintain harmony between family members. Thus, it includes relatives who are not shareholders of the company but are important for Claribet, Angel, and their children. In contrast, the family council is made up exclusively of the founding family. According to Claribet, the heirs’ prior reluctance to learn about the company business was related in some way to improper handling of the company-family relationships, and she emphasized the need to tackle this in the family protocol.

The overall conclusion for Exiquim can be summarized as follows: in family businesses, the manager is a temporary custodian of the firm and the family legacy. The main reason for implementing corporate governance is to mitigate future conflicts and provide a smooth transition to the next generation.

Bemel

In 1998, Carlos Benavides, the founder, and CEO of Bemel decided to restructure the ownership architecture, leaving as shareholders only the family members involved in managing Bemel; specifically, the father and the two younger children. At that time, the company had five employees, including the partners; now, there are 160 employees in several cities throughout Colombia and two offices in Panama.

In the first decade of 2000, family conflicts surfaced in the company. The founder had begun to delegate most of their functions to the sons, especially to Rodrigo, and had distanced themselves somewhat from the company’s operation. Meanwhile, Carlos brought a former college roommate into the company as his aide. Very efficient and dedicated to the company, this external executive naturally began acquiring power within the organization. A power struggle between the founder’s two sons and the non-family executive developed, with the most troublesome tensions between the two brothers.

As a result of the conflicts, Carlos moved to Panama in 2007 and established the company’s branch there. He returned to Colombia in 2009 just as the governance consulting process began. Previously, the family had not created a space to sit down and discuss the family business. Family members had received some financial information regarding Bemel, but those not involved in the company knew little about its governance.

A significant advantage of this governance advisory process was the active participation of the founder. When those siblings who were not involved in the company asked why they were not shareholders, he explained to them that the children who had needed financial support the most and were working for the company from the beginning were ultimately more entitled to receive stock. The advisory process enabled this family to improve communication and move forward with understanding and respect. By openly discussing family matters, members were able to overcome uncomfortable events from the past.

One of the main results of the family governance process in Bemel was the enactment of the family protocol. Carlos recalls that when the advisors presented the protocol model, they decided to modify it to reflect their family values and character. At that time, power in the company was split between Rodrigo and Carlos. However, a change in Rodrigo’s life forced him to retire in late 2009. This was the second management succession in less than ten years, but this transfer of authority was more formal than previously, from father to sons. It is important to remember that, as noted previously, the Bemel board was created during the consulting process, with the founder acting as chair.

The family protocol clarified the rules regarding the family-business relationship; through this process, the family agreed on limits to be respected and the mechanisms they can use to express their views. Within the protocol, policies regarding ownership were included to respect the family’s will and comply with restrictions imposed by the legal framework. The protocol restricts the access of in-laws into the company, and Carlos believes that this is one of the most critical points in the document.

The consulting process also led to the formation of a family council. This body includes members of the family that traditionally were not involved in the company; they now have a voice but no vote since they are learning about the company and its processes. The council allows potential partners to become briefed so that in the future, they can contribute to the success of the company. According to Carlos, the family council is a setting where family members present their business ideas and request financial support.

As perceived by the family, this governance advisory process has increased the company’s chance of survival over time. If the differences between Carlos and Rodrigo had not been overcome, and if misunderstandings concerning changes in the ownership structure had not been clarified, resentments would have affected the company’s stability in the future.

Pollo Andino

From the outset of Pollo Andino, company roles were distributed based on the natural abilities of each of the founders: Rigoberto oversaw administrative work, Mauricio was in sales, and Javier oversaw the production process. Eventually, they hired a plant manager along with other specialized personnel as the company grew. Family conflicts and power struggles emerged early on in the company, the founders married, and two of the wives established business relationships with Pollo Andino that culminated in conflicts.

Rigoberto recalls that the partners had initially agreed to hire family members under the belief that the company assets would be better safeguarded. However, the conflicts that emerged and other problems among shareholders led the founders to veto permitting any family member enter the company management. Therefore, from Pollo Andino’s first decade of operation and prior to the governance advisory process, founding family members had minimal access to business information.

Informality was the rule in the company during the 1980s, especially concerning the decision-making process. Conflicts of interest emerged as the company grow in the 1990s. Each founder took charge of their area and set their own rules. Decision-making was no longer coordinated, and the company operated under an ongoing power struggle as each founder sought to implement matters in their way. Moreover, in the 1990s, the company made strategic investments to increase production capacity and achieve vertical integration with other related businesses. Founders had also invested in a chicken hatchery and food production for poultry. According to Rigoberto, the company’s growth caused the operation to be more complex and gave each independent partner more power. There were also differences among the employees of each partner because senior management was in conflict and subordinates supported their own managers.

In 2007 Rigoberto decided to leave the company. He first informed his three children and wife and then the other founders. Mauricio also expressed his desire not to continue with his role as sales manager, so they decided to hire an outsider. Mauricio began working with Rigoberto in general management while looking for a replacement for the latter. It was then that they decided to participate in the corporate governance advisory program. The process began with an assessment of the situation through meetings with members and their families. This created a setting where families and partners expressed their feelings regarding issues they disagreed with and expected to have been rectified.

The first result of the corporate governance process was the family protocol. This simple process, which created no disagreements among the partners, established the conditions required for children to work in the company, namely: a minimum of five years’ experience, bilingualism, and to compete with non-family candidates during the selection process.

The company hired a new general manager in August 2007 and accomplished the full transfer of all functions over the next six months, giving Rigoberto time to prepare leaving his CEO post. Rigoberto asserts that he thought he was prepared to take this step but in reality, he was not; the loss of status and detachment of functions generated a discontent that remains today. However, both Mauricio and Rigoberto were aware of their limitations as senior managers.

Finally, according to Rigoberto, harmony among the founding members was restored thanks to this advisory process, which is notably one of the main outputs.

Flor Constructores

Manuel Galindo, a founder, and current manager of the company and the advisor who guided the company through the implementation of good governance practices mentioned that at the outset of Flor Constructores, the eldest son worked hand-in-hand with his parents, and the ownership structure was divided between them. The other two children subsequently received ownership shares of the company generating corporate governance problems of such magnitude that it led the company into grave financial problems.

The consultant that helped Flor Constructores design the company’s family governance structures recalls that the two younger children, along with their spouses, decided to create a separate consortium but corporate governance problems arose again. In particular, they did not exercise rigorous financial control; for example work budgets were not met or were not adjusted to reality, and they faced problems of co-administration.

Thanks to the corporate governance consulting process, the family protocol was enacted, which clarified the role of family shareholders. It established a transparent selection process for family members wishing to take up positions in the company. It also established a transparent compensation system for family members working at the company. Although setting up a complete family governance system was far from finished, they agreed that after the process, they had enhanced the channels of communication and information disclosure between family members. The family still holds informal meetings, but it is currently in the process of forming a family council with formal family protocols.

Concluding remarks

Advisors have played a defining role in the firms that we have analyzed in this paper. As suggested by theory, the advice, support, and hands-on help in the implementation process performed by the advisors have been key aspects for a positive change in the family businesses that we reviewed. Well thought out guidance that considers the business aspects and the family environment, have helped these firms adopt better governance structures at the firm and the family level. This paper shows how advisors, through trust, repeated interaction, and involvement in the implementation process with family and managers grow into important actors, seldom studied in the academic literature, in the development of a family business. For the four firms studied in this paper, the advisor becomes an integral part of the history and development of the firms, and they might play an important role in increasing the likelihood of its sustainability (Reay et al., 2013). Consistent with this vital role of the advisor in the family business development, these four cases taught us that advisors and families must be in the same frequency to succeed, where confidence, transparency, and trust, must be built working together and actively participating in the implementation process. This is the main difference between the consulting process with other non-family firms.

Ethical considerations

Authors confirm that the research does not raise ethical issues, indirect risks or implications to the participants in relation to the project.

Authors’ contributions

Authors are in alphabetical order and contributed equally to this work.

Financing

Funding from CESA School of Business and the University of the Andes School of Management Research Committee is fully acknowledged.

Interest conflicts

The authors have no relevant affiliations or financial involvement with any organization or entity with a financial interest in or financial conflict with the subject matter or materials discussed in the manuscript.

References

Adendorff, C., Boshoff, C., Court, P., & Radloff, S. (2005). The impact of planning on good governance practices in South African Greek family businesses. Management Dynamics: Journal of the Southern African Institute for Management Scientists, 14(4), 34-46. https://hdl.handle.net/10520/EJC69698

Apostolides, N. (2007). Directors versus shareholders: Evaluating corporate governance in the UK using the AGM scorecard. Corporate Governance: An International Review, 15(6), 1277-1287. https://doi.org/10.1111/j.1467-8683.2007.00646.x

Astrachan, J. H., & McMillan, K. S. (2006). The United States. In F. W. Kaslow (ed.), Handbook of family business & family business consultation: A global perspective (pp. 347-363). Binghamton, NY: International Business Press. https://doi.org/10.4324/9780203824726

Barbera, F., & Hasso, T. (2013). Do we need to use an accountant? The sales growth and survival benefits to family SMEs. Family Business Review, 26(3), 271-292. https://doi.org/10.1177/0894486513487198

Bartholomeusz, S., & Tanewski, G. A. (2006). The relationship between family firms and corporate governance. Journal of Small Business Management, 44(2), 245-267. https://doi.org/10.1111/j.1540-627X.2006.00166.x

Baxter, P., & Jack, S. (2008). Qualitative case study methodology: Study design and implementation for novice researchers. The Qualitative Report, 13(4), 544-559. https://doi.org/10.46743/2160-3715/2008.1573

Bennedsen, M. (2002). Why do firms have boards? (No 3-2002). Working paper. Copenhagen Business School. https://doi.org/10.2139/ssrn.303680

Block, J. (2012). R&D investments in family and founder firms: An agency perspective. Journal of Business Venturing, 27(2), 248-265 https://doi.org/10.1016/j.jbusvent.2010.09.003

Blondel, C., Carlock, R. S., & Heyden, L. V. D. (2005). Fair process: Striving for justice in a family business. Family Business Review, 18(1), 1-21. https://doi.org/10.1111/j.1741-6248.2005.00027.x

Blumentritt, T. (2006). The relationship between boards and planning in family businesses. Family Business Review, 19(1), 65-72. https://doi.org/10.1111/j.1741-6248.2006.00062.x

Blumentritt, T. P., Keyt, A. D., & Astrachan, J. H. (2007). Creating an environment for successful non-family CEOs: An exploratory study of good principals. Family Business Review, 20(4), 321-335. https://doi.org/10.1111/j.1741-6248.2007.00102.x

Brinkmann, S., & Kvale, S. (2015). Doing Interviews, 2nd ed. Thousand Oaks, CA: Sage Research Methods.

Cater III, J. J., & Justis, R. T. (2009). The development of successors from followers to leaders in small family firms: An exploratory study. Family Business Review, 22(2), 109-124. https://doi.org/10.1177/0894486508327822

Creswell, J. (1998). Qualitative inquiry and research design: Choosing among five traditions. Thousand Oaks, CA: Sage Publications.

Dunn, B. (1999). The family factor: The impact of family relationship dynamics on business-owning families during transitions. Family Business Review, 12(1), 41-60. https://doi.org/10.1111/j.1741-6248.1999.00041.x

Dyck, B., Mauws, M., Starke, F. A., & Mischke, G. A. (2002). Passing the baton: The importance of sequence, timing, technique, and communication in executive succession. Journal of business venturing, 17(2), 143-162. https://doi.org/10.1016/S0883-9026(00)00056-2

Dyer, W. G. (1994). Potential contributions of organizational behavior to the study of family-owned businesses. Family Business Review, 7(2), 109-131. https://doi.org/10.1111/j.1741-6248.1994.00109.x

Dyer Jr, W. G., & Wilkins, A. L. (1991). Better stories, not better constructs, to generate better theory: A rejoinder to Eisenhardt. Academy of Management Review, 16(3), 613-619. https://doi.org/10.5465/amr.1991.4279492

Eddleston, K. A., & Kellermanns, F. W. (2007). Destructive and productive family relationships: A stewardship theory perspective. Journal of Business Venturing, 22(4), 545-565. https://doi.org/10.1016/j.jbusvent.2006.06.004

Eisenhardt, K. M. (1991). Better stories and better constructs: The case for rigor and comparative logic. Academy of Management Review, 16(3), 620-627. https://doi.org/10.5465/amr.1991.4279496

Eisenhardt, K. (1989). Building theories from case study research. Academy of Management Review, 14(4), 532-550. https://doi.org/10.5465/amr.1989.4308385

Eisenhardt, K. M., & Graebner, M. E. (2007). Theory building from cases: Opportunities and challenges. Academy of Management Journal, 50(1), 25-32. https://doi.org/10.5465/amj.2007.24160888

Fama, E. (1980). Agency Problems and the Theory of the Firm. The Journal of Political Economy, 88(2), 288-307. https://doi.org/10.1086/260866

Fama, E., & Jensen, M. (1983). Separation of ownership and control. The Journal of Law and Economics, 26(2), 301-325. https://doi.org/10.1086/467037

Fahed-Sreih, J., & Djoundourian, S. (2006). Determinants of longevity and success in Lebanese family businesses: An exploratory study. Family Business Review, 19, 225-234. https://doi.org/10.1111/j.1741-6248.2006.00071.x

Feltham, T. S., Feltham, G., & Barnett, J. (2005). The dependence of family businesses on a single decision-maker. Journal of Small Business Management, 43, 1-15. https://doi.org/10.1111/j.1540-627X.2004.00122.x

González, M., Guzmán, A., Pombo, C., & Trujillo, M. A. (2012). Family firms and financial performance: The cost of growing. Emerging Markets Review, 13(4), 626-649. https://doi.org/10.1016/j.ememar.2012.09.003

González, M., Guzmán, A., Pombo, C., & Trujillo, M. A. (2013). Family firms and debt: Risk aversion versus risk of losing control. Journal of Business Research, 66(11), 2308-2320. https://doi.org/10.1016/j.jbusres.2012.03.014

González, M., Guzmán, A., Pombo, C., & Trujillo, M. A. (2014). Family involvement and dividend policy in closely held firms. Family Business Review, 27(4), 365-385. ttps://doi.org/10.1177/0894486514538448

Gutiérrez, P. (2003). La calificación de Colombia en prácticas de gobierno corporativo: Confecámaras promueve el gobierno corporativo en Colombia. En: CIPE (eds.), En busca de buenos directores: una guía hacia la formación del gobierno corporativo en el siglo 21, CIPE: Washington DC.

Guzmán, A., Trujillo, M. A., del Hierro, J. E., Higuera, M. P., Hoyos, F., Márquez, D., Mejía, M. P., & Téllez, J. (2020). Protocolos de familia: su relevancia como mecanismo de gobierno familiar y empresarial. Bogotá: Colegio de Estudios Superiores de Administración – CESA.

Heck, R., Hoy, F., Poutziouris, P., & Steier, L. (2008). Emerging paths of family entrepreneurship research. Journal of Small Business Management, 46(3), 317-330. https://doi.org/10.1111/j.1540-627X.2008.00246.x

Howorth, C., & Assaraf Ali, Z. (2001). Family business succession in Portugal: An examination of case studies in the furniture industry. Family Business Review, 14(3), 231-244. https://doi.org/10.1111/j.1741-6248.2001.00231.x

Jaffe, D. T., & Lane, S. H. (2004). Sustaining a family dynasty: Key issues facing complex multigenerational business- and investment-owning families. Family Business Review, 17, 81-98. https://doi.org/10.1111/j.1741-6248.2004.00006.x

Kaye, K. (1998). Happy landings: The opportunity to fly again. Family Business Review, 11, 275-280. https://doi.org/10.1111/j.1741-6248.1998.00275.x

Lambrecht, J. (2005). Multigenerational transition in family businesses: A new explanatory model. Family Business Review, 18(4), 267-282. https://doi.org/10.1111/j.1741-6248.2005.00048.x

Lane, S., Astrachan, J., Keyt, A., & McMillan, K. (2006). Guidelines for family business boards of directors. Family Business Review, 19(2), 147-167. https://doi.org/10.1111/j.1741-6248.2006.00052.x

Lawton, P., & Rigby, E. (1992). Meetings, their Law and Practice. London: Pitman.

Leon-Guerrero, A. Y., McCann III, J. E., & Haley Jr, J. D. (1998). A study of practice utilization in family businesses. Family Business Review, 11(2), 107-120. https://doi.org/10.1111/j.1741-6248.1998.00107.x

Martin, H. (2001). Is family governance an oxymoron? Family Business Review, 14(2), 91-96. https://doi.org/10.1111/j.1741-6248.2001.00091.x

McCracken, G. (1988). The long interview (vol. 13). Thousand Oaks, CA: Sage Publications.

Miller, D., Steier, L., & Le Breton-Miller, I. (2003). Lost in time: Intergenerational succession, change, and failure in a family business. Journal of Business Venturing, 18(4), 513-531. https://doi.org/10.1016/S0883-9026(03)00058-2

Michel, A., & Kammerlander, N. (2015). Trusted advisors in a family business's succession-planning process –An agency perspective. Journal of Family Business Strategy, 6(1), 45-57. https://doi.org/10.1016/j.jfbs.2014.10.005

Mustakallio, M., Autio, E., & Zahra, S. A. (2002). Relational and contractual governance in family firms: Effects on strategic decision making. Family Business Review, 15(3), 205-222. https://doi.org/10.1111/j.1741-6248.2002.00205.x

Poza, E. J., Hanlon, S., & Kishida, R. (2004). Does the family business interaction factor represent a resource or a cost? Family Business Review, 17, 99-118. https://doi.org/10.1111/j.1741-6248.2004.00007.x

Prada, F. (2011). Colombia: del mero cumplimiento a la convicción sobre el Gobierno Corporativo. En: IGCLA y GCGF (eds.), Gobierno Corporativo en Latinoamérica 2010-2011, IGCLA y GCGF.

Reay, T., Pearson, A. W., & Gibb, W. (2013). Advising family enterprise: Examining the role of family firm advisors. Family Business Research, 26(3), 209-214. https://doi.org/10.1177/0894486513494277

Salvato, C., & Corbetta, G. (2013). Transitional leadership of advisors as a facilitator of successors’ leadership construction. Family Business Review, 26(3), 235-255. https://doi.org/10.1177/0894486513490796

Schulze, W. S., Lubatkin, M. H., Dino, R. N., & Buchholtz, A. K. (2001). Agency relationships in family firms: Theory and evidence. Organization Science, 12(2), 99-116. https://doi.org/10.1287/orsc.12.2.99.10114

Schulze, W. S., Lubatkin, M. H., & Dino, R. N. (2003). Exploring the agency consequences of ownership dispersion among the directors of private family firms. Academy of Management Journal, 46(2), 179-194. https://doi.org/10.5465/30040613

Strätling, R. (2003). General meetings: A dispensable tool for corporate governance of listed companies. Corporate Governance: An International Review, 11(1), 74-82. https://doi.org/10.1111/1467-8683.00303

Su, E., & Dou, J. (2013). How does knowledge sharing among advisors from different disciplines affect the quality of the services provided to the family business client? An investigation from the family business advisor’s perspective. Family Business Review, 26(3), 256-270. https://doi.org/10.1177/0894486513491978

Shleifer, A., & Vishny, R. W. (1997). A survey of corporate governance. Journal of Finance, 52(2), 737-783. https://doi.org/10.1111/j.1540-6261.1997.tb04820.x

Sorenson, R. (1999). Conflict management strategies used by successful family businesses. Family Business Review, 12(4), 325-339. https://doi.org/10.1111/j.1741-6248.1999.00325.x

Stake, R. E. (1995). The art of case study research. Thousand Oaks, CA: Sage Publications.

Strike, V. (2012). Advising the family firm: Review the past to build the future. Family Business Review, 25, 156-177. https://doi.org/10.1177/0894486511431257

Strike, V. (2013). The most trusted advisor and the subtle advice process in family firms. Family Business Review, 26, 293-313. https://doi.org/10.1177/0894486513492547

Swartz, S. (1989). The challenges of multidisciplinary consulting to family-owned businesses. Family Business Review, 2(4), 329-331. https://doi.org/10.1111/j.1741-6248.1989.tb00002.x

Thomas, J. (2002). Freeing the shackles of family business ownership. Family Business Review, 15, 321-336. https://doi.org/10.1111/j.1741-6248.2002.00321.x

Tirole, J. (2001). Corporate governance. Econometrica, 69(1), 1-35. https://doi.org/10.1111/1468-0262.00177

Tracy, S. J. (2019). Qualitative research methods: Collecting evidence, crafting analysis, communicating impact, 2nd ed. John Wiley & Sons.

Voordeckers, W., Van Gils, A., & Van den Heuvel, J. (2007). Board Composition in Small and Medium‐Sized Family Firms. Journal of Small Business Management, 45(1), 137-156. https://doi.org/10.1111/j.1540-627X.2007.00204.x

Villalonga, B., Amit, R., Trujillo, M. A., & Guzmán, A. (2015). Governance of family firms. Annual Review of Financial Economics, 7, 635-654. https://doi.org/10.1146/annurev-financial-110613-034357

Villalonga, B., Trujillo, M. A., Guzmán, A., & Cáceres, N. (2019). What are boards for? Evidence from closely held firms in Colombia. Financial Management, 48(2), 537-573. https://doi.org/10.1111/fima.12224

Yin, R. (2003). Case study research design and methods. Thousand Oaks, CA: Sage Publications.

Appendix

Corporate Governance: Latin America and Colombia between the 1900s and 2010s

Colombia’s economic openness during the 1990s allowed investors such as the International Finance Corporation –IFC– to invest in the country. IFC made a series of commitments to Colombian firms –private and state-owned, regarding good governance– with technical assistance provided by consultants who knew the globally accepted principles of good governance.

In 1999 the OECD (Organization for Economic Cooperation and Development) promulgated a set of corporate governance principles as a reference for regulators, entrepreneurs, investors, academics, and others interested in this subject worldwide. In a revised version of these principles, the OECD, in2004, makes explicit the relationship between regulated corporate governance and the transparency and efficiency of capital markets; it also highlights the importance of governmental agencies for supervision, regulation, and imposition of penalties when needed.

Looking to adopt these corporate governance principles for Latin America, the Latin American Corporate Governance Roundtable met for the first time in April 2000, organized in collaboration with the OECD, the World Bank, IFC, and both public and private regional partners. The work of the roundtable, published in 2003, takes the particularities of Latin America into account with special emphasis on the need to improve compliance and enforcement of standards in the region and to encourage cooperation between the constituent countries.

Another multilateral organization contributing to the development of good corporate governance in Latin American countries is the Development Bank of Latin America, formerly known as the Andean Development Corporation (CAF, Spanish acronym). Of particular interest to regulators, investors, companies, and other capital market players are CAF’s ‘Guidelines for an Andean Code of Corporate Governance,’ published in 2005. For each measure of corporate governance, the guidelines consider whether it should be taken into account by large companies, listed companies, or closely-held businesses. This is especially important as it begins to contextualize corporate governance for closely-held medium-sized and small firms not listed on the stock exchange.

Along with these international efforts, direct intervention in Colombia by such organizations as the Center for International Private Enterprise (CIPE), Confecámaras, and governmental supervisory agencies has increased the awareness of entrepreneurs, shareholders, and regulators regarding the need for good governance practices in listed and closely-held firms. According to Prada (2011), corporate governance came to Colombia through a program developed by CIPE and Confecámaras in 1999 to emphasize the importance of good corporate governance, especially for firms listed on the stock exchange.

The joint project comprised of different aspects of action: the diagnosis of corporate governance practices in Colombian firms, the search for establishing codes of good governance in the country, training advisors, issuers, investors, and audit firms in corporate governance, the disclosure of the importance of corporate governance through a media strategy and publication of various documents with academic and practitioner approaches, and supporting legislative initiatives to increase the implementation of good corporate governance practices (Gutiérrez, 2003).

The first step taken by Confecámaras and CIPE involved studies in determining the state of corporate governance in Colombia, which generated disturbing results. Among the main weaknesses highlighted between 2000 and 2002 were the lack of mandatory or voluntary adoption of corporate governance codes, the limited independence of board members, low application of investors’ existing rights, the need for additional rights for investors in accordance with international standards, and the lack of a clear policy on disclosure of information. These weaknesses could be partially due to the lack of knowledge of family managers of the benefits provided by a sound corporate governance system. Reay et al. (2013) argue that advisors are ‘effective translators’ of research knowledge to implementable practice in the specific context of each firm.

This analysis, coupled with the activism of Confecámaras and CIPE and the work of government agencies, explains in part the changes in regulation that have emerged in Colombia in the last decade. The regulations established in this period require that major institutional investors, such as those associated with pension funds, consider compliance with minimum standards of good governance when choosing their investments. Regulations also established specific requirements relating to disclosure, insider trading, minority shareholder protection, and the structure and independence of the board, among other issues.

In 2007, a committee comprising of different stakeholders in Colombian corporate governance defined minimum standards to be adopted by companies that act as issuers of securities on the Stock Exchange of Colombia. These standards were published as the Best Practices Code of Colombia, better known as Código País (Country Code). However, progress does not only involve issuers of securities. As previously noted, one of the most important aspects of CAF’s 2005 ‘Guidelines for an Andean Corporate Governance Code’ was the intent to bring corporate governance to closely-held, medium-sized and small companies.

A multilateral agency such as CAF is aware of the prevalence of closely-held and family firms in Latin American countries, and Colombia is a clear example of this reality. Fewer than 100 firms have issued stocks on the Colombia Stock Exchange to date, and only 24 can be considered highly tradable. Therefore, CAF published its ‘Corporate Governance Manual for Privately Held Firms’ in 2006 as a valuable tool for small, medium-sized, and large firms that have restrictions on the free transfer of shares or ownership participation. In Latin America, such companies generate the most significant contribution to GDP and the majority of jobs.

Building on efforts at the regional level, the Superintendence for Commercial Societies (SSOC) began implementing good governance in privately held firms. In 2009 the SSOC, Confecámaras and the Bogotá Chamber of Commerce developed the ‘Guide to Colombian Corporate Governance for Closely-Held and Family Firms.’ Subsequently, Confecámaras and the Chamber of Commerce of Bogotá implemented these measures in the applicable firms. Among the measures undertaken in this regard was a Corporate Governance Training Program that began in 2010. The program selected a team of advisors through a rigorous process to implement good governance practices in closely-held and family firms.

With international support from organizations such as CIPE and SECO, Confecámaras sought to strengthen the management and performance of closely-held and family-owned firms to increase their perdurability and reduce their rate of bankruptcy while easing their access to different funding sources and encouraging a culture of good corporate governance (Prada, 2011). In fulfilling these objectives, Confecámaras implemented the measures suggested in the ‘Guide to Colombian Corporate Governance for Family and Closely-Held Firms’ in the target organizations. A pilot test involving different firms and advisors trained in corporate governance sought to achieve a demonstrable effect to encourage other companies to follow this path. The cases we analyzed in this paper are part of the mentioned pilot.

Notes

*

Research paper.

1

SSOC is the government body overseeing the real sector firms, especially those corporations that are not subject to the supervision of another governmental body, such as the Superintendence of Utilities. By 2012, more than 22,000 companies with revenues or assets greater than or equal to $10,000 are under SSOC supervision.

Author notes

a Corresponding author. E-mail address: maria.trujillo@cesa.edu.co

Additional information

Cited as: Trujillo, M. A., González, M., & Guzmán, A. (2021). Advisors in Corporate Governance of Family Firms. Cuadernos de Administración, 34. https://doi.org/10.11144/Javeriana.cao34.acgff