APA

ISO 690-2

Harvard

Haga clic en un formato de citación

Innovation financing in Colombia: An explicative proposal*

Financiación de la innovación en Colombia: una propuesta explicativa

Financiamiento da inovação na Colômbia: uma proposta explicativa

Cuadernos de Administración, vol. 34, 2021

Pontificia Universidad Javeriana

Jaime Humberto Sierra-González a jhsierra@javeriana.edu.co

Pontificia Universidad Javeriana, Colombia

David Andrés Londoño-Bedoya

Pontificia Universidad Javeriana, Colombia

Juan Manuel García-Ospina

Pontificia Universidad Javeriana, Colombia

Received: 14 September 2020

Accepted: 09 July 2021

Published: 15 October 2021

Abstract:

Data on innovation financing in Colombia present a paradox: Manufacturing companies prefer to finance their innovation projects with their own capital, with bank loans in second place, and cheaper public funding last. Extant financial theories cannot explain such a paradox (reversed pecking order), making a different approach necessary. Hence, a new perspective is presented on the basis of Sierra’s (2014, 2020) proposal. A fixed effects panel estimation is carried out that includes three new variables: A Knowledge Incorporation and Consolidation System, interaction among companies and funders, a particular type of investor (Dedicated). The results support the alternative explanation. Additionally, research possibilities, designs and applications of public and organisational policy aimed to overcome some of the problems mentioned are proposed.

JEL Codes: D81, D92, G32, O16, O31.

Keywords:Alternative funding, investment strategy, project uncertainty, risk funding, strategic decision-making, paradox.

Resumen:

Los datos sobre la financiación de la innovación en Colombia presentan una paradoja: las compañías manufactureras prefieren financiar sus proyectos de innovación con su propio capital, usando préstamos bancarios como segunda opción o, en última instancia, fondos públicos de bajo costo. Las teorías existentes no pueden explicar esta paradoja (inversión del orden jerárquico), y hacen necesario un abordaje diferente. Por tanto, se presenta una nueva perspectiva a partir de la propuesta de Sierra (2014, 2020). Se realiza una estimación de panel de efectos fijos que incluye tres nuevas variables: un Sistema de Incorporación y Consolidación de Conocimiento, la interacción entre compañías e inversionistas, y un tipo particular de inversionista (Dedicado). Los resultados apoyan la explicación alternativa. Adicionalmente, se proponen algunas posibilidades de investigación, además de diseños y aplicaciones de políticas públicas y organizacionales orientadas a solucionar algunos de los problemas mencionados.

Códigos JEL: D81, D92, G32, O16, O31.

Palabras clave: Financiamiento alternativo, estrategia de inversión, proyección de incertidumbre, financiación de riesgo, estrategia de toma de decisiones, paradoja.

Resumo:

Os dados sobre financiamiento da inovação em Colômbia apresentam um paradoxo: as companhias manufatureiras preferem financiar seus projetos de inovação com o seu próprio capital, usando empréstimos bancários como segunda opção ou, finalmente, fundos públicos de baixo custo. As teorias existentes não conseguem explicar este paradoxo (inversão da ordem hierárquica), fazendo uma abordagem diferente. Por tanto, uma nova perspectiva é apresentada a partir da proposta de Sierra (2014, 2020). Um painel de estimação de efeitos fixos foi realizado com a inclusão de três novas variáveis: um Sistema de Incorporação de Conhecimento e Consolidação, a interação entre companhias e investidores, e um tipo particular de investidor (Dedicado). Os resultados suportam a explicação alternativa. Aliás, propõem-se algumas possibilidades de pesquisa, além de desenhos e aplicações de políticas públicas e organizacionais orientadas a solucionar alguns dos problemas mencionados.

Códigos JEL: D81, D92, G32, O16, O31.

Palavras-chave: Financiamento alternativo, estratégia de investimento, projeção de incerteza, financiamento de risco, estratégia da tomada de decisões, paradoxo.

Introduction and problem approach

Colombia is the most recent member State of OECD and it barely invests 0.25% of GDP in science, technology and innovation (STI). While public spending on STI activities recently reached 30% of total funding, private actors contribute the remaining 70%; firms contribute 53% of the total spending, and higher education entities, non-governmental organisations, research centres and government entities contribute the remaining 47% jointly. Likewise, Minciencias1 –the Ministry of Science, which is the hub of the national innovation system– is the main financier of seed capital in the country; at a regional level, the departmental (Colombian states) governments contribute to such financing through oil and mining royalty funds allocated to STI activities. However, there are few companies that bet on innovation as a central component of their competitive strategy and, in addition, there are even fewer that operate in technology-intensive sectors. In fact, despite being the newest OECD member, Colombia is the new tail-light according to OECD standards in this subject (OCyT, 2018).

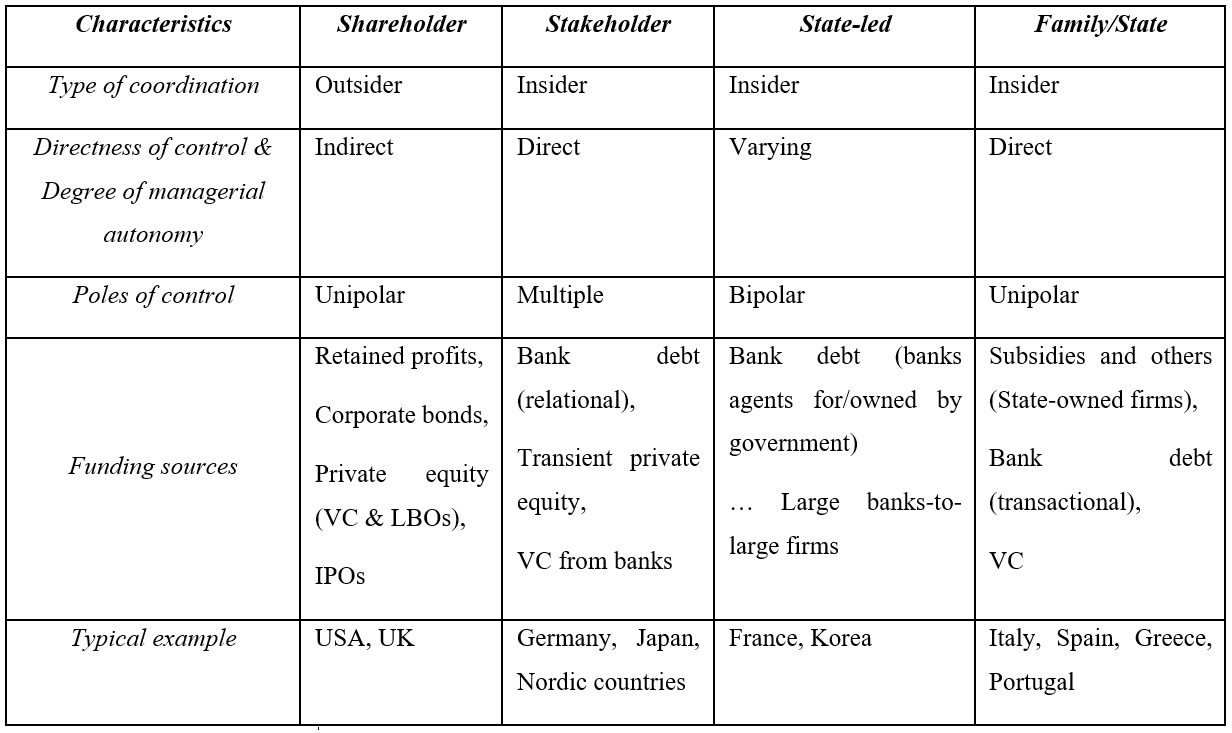

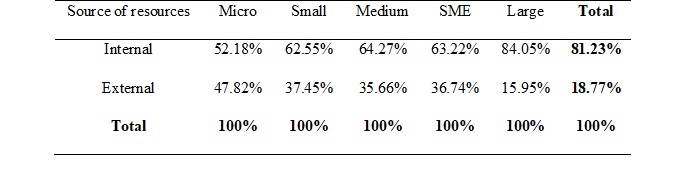

Moreover, only a few first and second tier financial institutions are interested in financing STI projects in Colombia. To complete this picture, venture capital in many cases faces serious restrictions as in almost all Latin American countries (Jiménez, 2008); also, potential applicants seem not to know or recognise this alternative2 to finance their projects. Additionally, the stock/equity market is underdeveloped and inefficient. This snapshot shows Colombia as a country relatively close to the stereotypical Tylecote and Visintin’s (2008) Family/State pattern in terms of its corporate governance and financial system characterisation, particularly in reference to coordination and control; however, it does not fit the category perfectly since transactional bank debt is the main funding source, but VC is essentially absent (Table 1).

Interestingly, according to previous research on this subject, most Colombian firms prefer to finance their innovation projects with internal liquidity (undistributed profits) in the first place. Only when these funds are non-existent or insufficient, they go to commercial banks for funding3 (loans) or, very marginally, they get financing from suppliers or clients (deferred or advanced payments) (Sierra, Malaver, & Vargas, 2009; Barona, Rivera, & Aguilera, 2015). Yet, external financing seems to be more relevant in the case of small and medium-sized firms (SMEs) (García, Barona, & Madrid, 2013), possibly due to their low degree of liquidity.

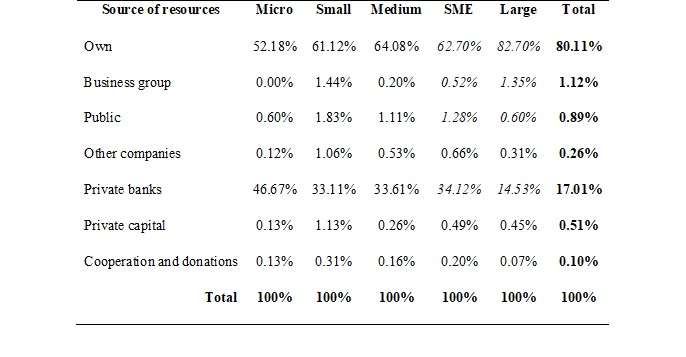

When external funds become desirable, companies prefer to go to local commercial banks rather than to available public financers (Table 2) or to international banks. On the other hand, funding through private bond placement is rare (Sierra et al., 2009; Barona et al., 2015). Thus, innovative Colombian companies, unlike what established by the standard pecking order theory (i.e., equity, debt, new private capital), do not seem to like new private capital to finance their innovation projects4.

This situation pictures a particular scenario: Colombian firms invest little in STI activities but prefer to do so based on their internal resources. Public entities offer the best options for external financing (subsidies and soft loans), although partial and limited in terms of amounts. However, firms with low liquidity indicators prefer to go to local commercial banks. Moreover, these companies rarely seek fresh private capital (perhaps because it is scarce), except for some cases where over-the-counter resources are sought (for example, some start-ups) (Table 2).

This diagnosis, based on the few existing studies (Sierra et al., 2009, García et al., 2013, Barona et al., 2015), not only presents an approximate profile of the behaviour of innovative Colombian companies, but also seems to suggest some characteristics of the projects developed by these companies. In addition, it is clear that there is a lot of research to do regarding other innovative Colombian organisations such as higher education institutions, research centres (e.g., sectoral technological development centres) and technology parks, and their way of financing STI projects and activities (OCyT, 2018).

Thus, in this paper we want to address some questions related to the paradox described above, particularly the relational dimension between the two parties: supply and demand of funds. How well do innovation project owners (e.g., firms) know the Colombian institutional and financial grid? How often do the two parties (supply and demand) get in touch? Does the Colombian financial institutional grid adequately respond to the financial needs of innovative sectors and firms? What is the role of strategy in the case of innovative companies?

Previous studies seem to indicate that Colombian innovative companies do not know the national STI system, and particularly its financial actors, well enough or they are somehow not interested in taking advantage of the sources and financing mechanisms available due to some factors such as red tape (in the past, that included finding university-based allies as necessary partners to access public funding calls), the requirement of real collateral, and the high costs that dissuade them from considering external resources.

The primary obstacles seem to refer to an inadequate context and mechanisms of interaction (matching environment/mechanisms) and, therefore, to the availability of few financing sources/mechanisms with restrictive conditions that hinder the adaptation and coupling of supply and demand of funds. Moreover, the limited record of success of both sides and knowledge asymmetries could also be factors that hamper the creation of trustworthiness in the relationship, particularly in the case of SMEs and start-ups (Sierra et al., 2009, Otálora, Hurtado, & Quimbay, 2009, García et al., 2013, Barona et al., 2015, Sierra, 2018).

Finally, although there are no detailed studies on the strategies of innovative companies in Colombia, the limited evidence available seems to indicate that the prevailing presence of short-term and cost-related criteria is an important determinant of business decisions. The limitations of such an approach are consistent with the characteristics of the institutional financial grid and the Colombian STI ecosystem. This brief characterisation highlights the embryonic development of the national STI system in relation to such a key variable as the development of adequate funding sources and mechanisms.

Therefore, the particular question that is addressed in this paper is: How can the paradox about the use of financial sources and mechanisms by innovative firms in the Colombian STI system be explained?

A relevant theoretical framework

Traditional literature on financing innovation

In simple terms, the abundant classic financial literature (Becchetti & Sierra, 2002, Hall & Lerner, 2010, Sierra, 2014) offers two approaches that explain investment in innovation projects. The selection approach assumes that project owners (company or researcher) or potential funders (external investors) choose their partnerfrom a group of possible individuals. Project owners/investors select their funders/inventors (Myers & Majluf, 1984; Amit, Brander, & Zott, 1998; Gompers & Lerner, 2001; Eckhardt, Shane, & Delmar, 2006; Ullah, Abbas, & Akbar, 2009; Knockaert, Clarysse, & Wright, 2010; Mina & Lahr, 2011; Bertoni & Tykvova, 2012).

The inducement approach assumes, instead, that project owners/investors actively seek an opportunity and when they find it, they try to convince the other party to establish an investment relationship. In other words, project owners try to persuade investors to support the project with their resources and investors try to convince project owners that their financial (and other type of) support is the most appropriate for the project (Bygrave & Timmons, 1992; Gompers & Lerner, 1998, Powell, Koput, Bowie, et al., 2002; Gulati & Higgins, 2003, Hallen, 2008, Bertoni, Colombo, & Grilli, 2011; Hallen & Eisenhardt, 2012).

These explanations have a strong bias because from two perspectives (source hierarchy or pecking order theory - POT and catalytic strategies - CST), the only criteria apparently sufficient to choose a funding source are the preferences/conveniences, the initiative, and strategies of project owners. On the contrary, from the perspective of passive search theory - PST and active search theory - AST, it is argued that investors apply objective criteria to assess the projects proposed by the owners and there is no other type of interaction between the parties or additional information is needed to make investment decisions, although active search involves some exchange of information (Table 3).

In addition, these explanations leave aside the contextual factors of financing decisions made by project owners, as well as by investors, and their dynamics (e.g., selection criteria and fixed or changing preferences, stage of project development). The characteristics of investors and project owners, their behaviour, and their impact on interactions are not considered in these explanatory models, either.

This is how imbalance and bias seem to suggest that decisions are independent and do not involve interactions between the parties. Furthermore, it is assumed that decisions are isolated from their context in terms of time and socio-geographical issues, which weakens the explanatory power of the existing approaches (Sierra, 2014).

An alternative theoretical approach

From a systemic sectoral perspective, a different explanatory model proposes to eliminate the problems of traditional approaches to financing innovation. The essential points of the proposal are: i) there is a continuous and consistent interaction between project owners and potential investors; ii) interactions are articulated around knowledge, characteristics of the parties, and features of the context; these elements, like the preferences of the parties, can mutate over time and shape the interactions; iii) knowledge and networks creation are deeply linked and play a significant role in the interactions of the parties involved; iv) decision-making processes of the parties on innovation financing and their changes over time deserve a more complete, explicit, and detailed description (Sierra, 2014; Sierra, 2018).

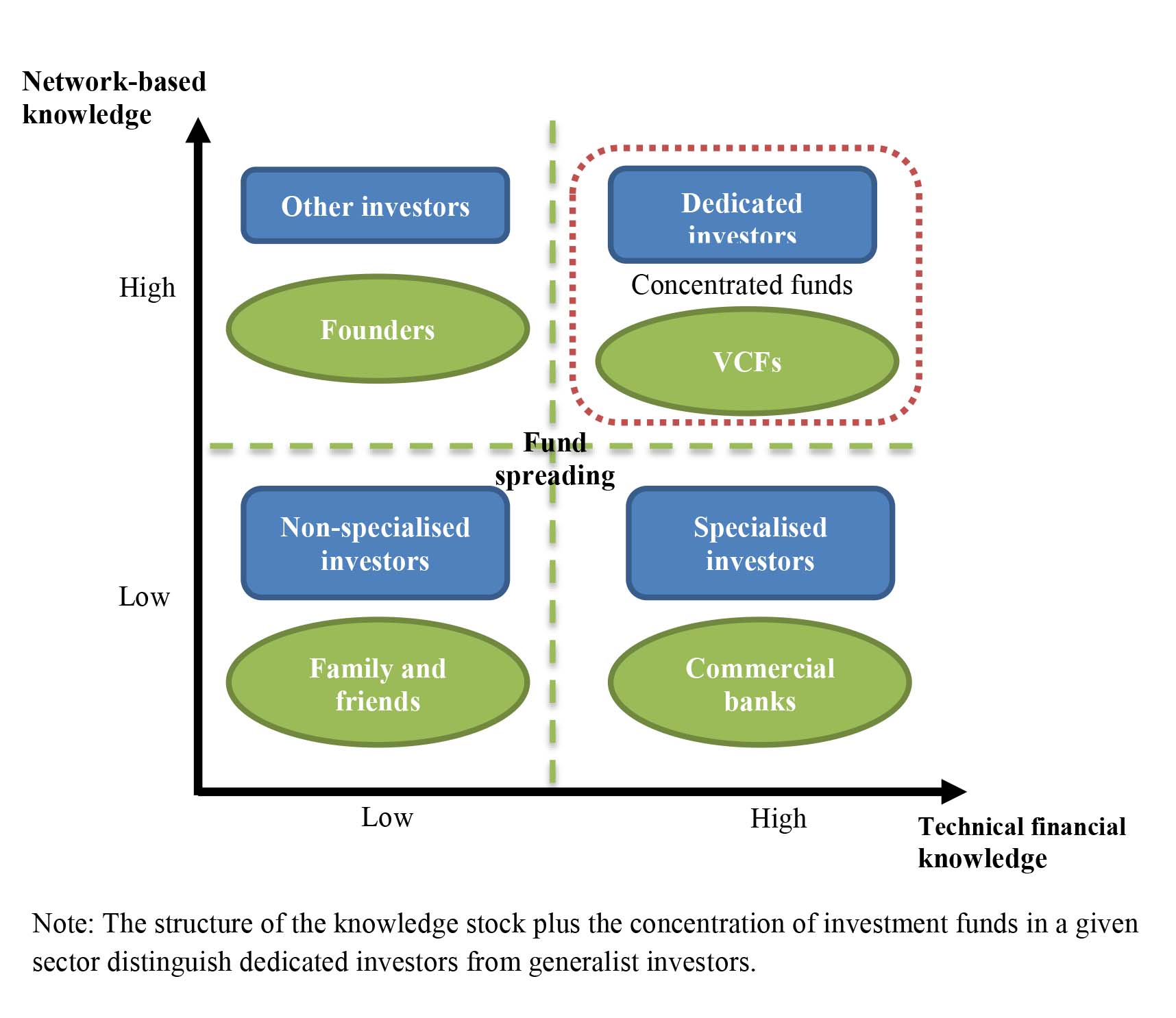

Under this perspective, it is proposed that both project owners and investors build and possess a Knowledge Incorporation and Consolidation System (KICS) that changes over time and that, in the first case, includes the necessary knowledge to innovate, to search, and to negotiate the financing for projects and, in the second case, includes technical and financial knowledge about innovation in a given sector and, also, knowledge underlying the ability to create networks. In this abstraction Knowledge has two forms, stock (i.e., knowledge accumulated through learning, experience, etc.) and flow (i.e., new knowledge mobilised by different channels, including networks) (Figure 1). The KICS underlies the interactions of the parties involved (Sierra, 2014).

Additionally, it is necessary to bear in mind that despite the regulatory proposals on the creation of a large and well-established Institutionalised Financial System (IFS), the same sources and financing mechanisms are not available in all contexts and not all existing sources, including over-the-counter financiers who are more active than ever (Sierra, 2020), have the same willingness to finance innovation projects. Each potential external funder also has different characteristics and preferences concerning the investor base (and its impact on the amount of funds and the size of the team), the time horizon of interest and the timing of the decision, the structure of the preferred investment (co-investor vs lone investor), the preferred investment stage, and the preferred exit mode (Sierra, 2014).

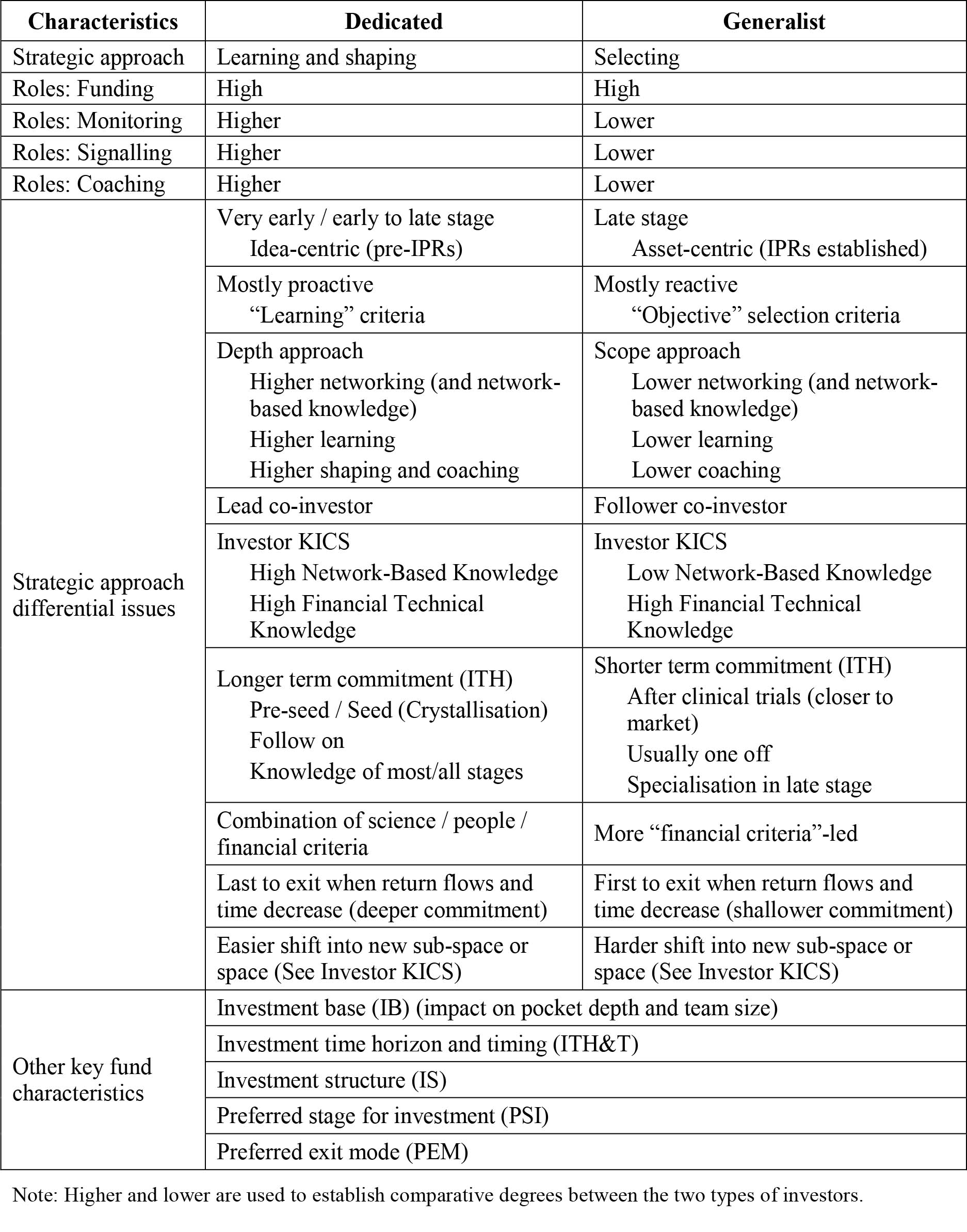

Because of the role that the KICS plays in formulating and deploying the strategy to seek investment opportunities by potential funders, four categories of external funders of innovation projects emerge: Specialised, non-specialised, dedicated, others (Figure 1). Particularly, two types of radically different external investors come forth (dedicated and generalist) which differ in their roles and strategic approach (Table 4), even though they can eventually mutate from one investor category to another (Sierra, 2014).

Likewise, this explanatory approach proposes that, in a sector-specific STI ecosystem, the financing decisions of innovation projects by potential external investors cannot be explained without taking into account how much knowledge the two parties have on the STI ecosystem and, especially how well project owners know the relevant Institutionalised Financial System (IFS). Moreover, financing decisions cannot be explained without considering the characteristics and preferences of the counterparts (supply and demand of investment) and their interaction strategies, especially when the whole theoretically possible range of sources and financing mechanisms is not available and may not be interested in innovation projects. Therefore, it is not strategically equivalent to seek and interact with dedicated investors or with generalists (Sierra, 2014, 2020).

Financing innovation in Colombia

After analysing the classic financial literature and the alternative theoretical approach to financing innovation, it will be contrasted for Colombia through an econometric data panel model explained below.

Data and sources

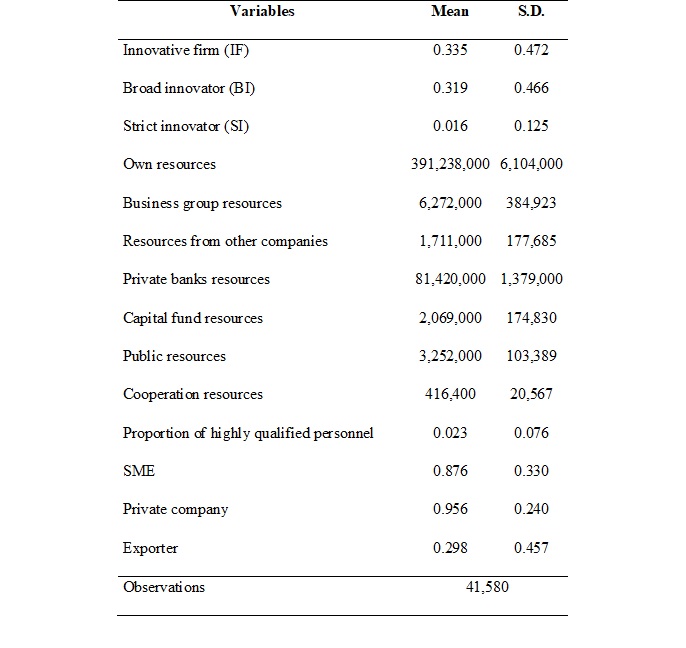

The data on which this analysis is based comes from two sources: The Development and Technological Innovation Survey (EDIT, in Spanish) and the Annual Manufacturing Survey (EAM, in Spanish), both applied to Colombian companies by the National Administrative Department of Statistics (DANE, in Spanish). The sample includes a time horizon of ten years, covering from 2007 to 2016. The panel database has 41,580 observations, which allows tracking the evolution of 4,158 companies during the ten years included in the study. The survey includes manufacturing companies with more than 10 employees or with a production value of more than 130,000 US dollars for 20165. The sample includes companies from 22 sectors of economic activity identified with the International Standard Industrial Classification (ISIC) at two digits.

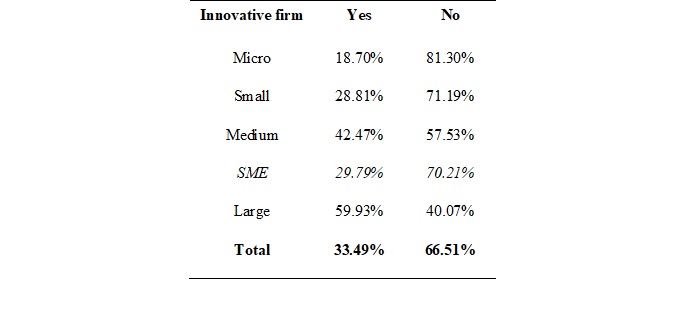

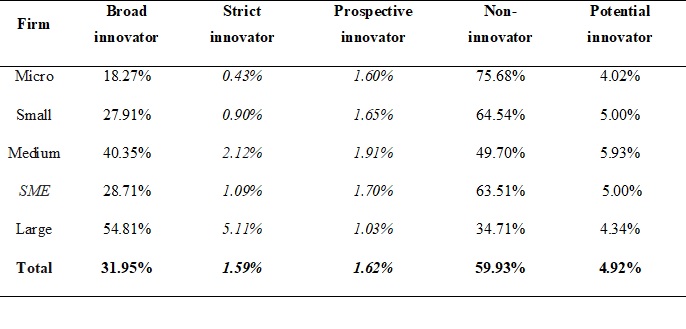

The manufacturing companies included in the sample are mostly SMEs6, private (firms where the State owns 49% or less of the assets), non-exporting, and employ few highly qualified personnel (personnel with a master’s or PhD degree). On the side of innovation, the picture is not encouraging; innovative manufacturing firms (IF)7 are a minority and even fewer are those that make innovations with greater geographic scope (SI). Likewise, there are also few companies that cooperate to innovate with another ecosystem actor (Table 5).

In terms of innovation investment, the scenario is similar. On average, Colombian manufacturing firms invest 391 million pesos (US$ 120,000) of their own resources annually, obtain commercial bank loans for 81 million pesos (US$ 25,000), access 3 million pesos (US$ 1,000) of public resources and 2 million pesos (US$ 616) from capital funds, and only 0.4 million pesos (US$ 125) via cooperation resources (Table 5). The results are consistent; few manufacturing firms innovate, usually the largest ones, and these show great advantage over all others (Tables 6 and 7).

In this context of little innovation, another problem is evident: The limited growth of international competitiveness guided by innovation (only 1.59% firms achieve innovation-based improvements aimed at the international market and 1.62% state having the intention to innovate - column 2, Table 7).

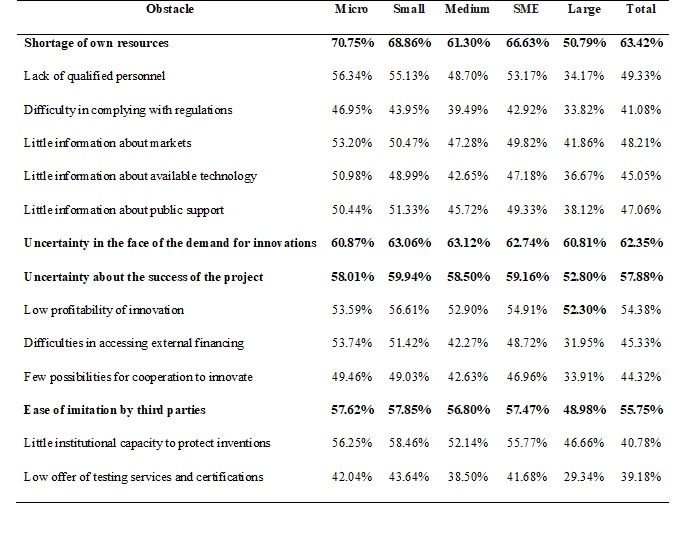

This scenario reveals that firms do not have a lot of incentives to innovate and, on the contrary, innovation is perceived as unprofitable (54.4%) due to alleged uncertainty regarding the demand for innovations on the market (62.4%) and the uncertainty regarding the success of projects (57.9%) (Table 8).

Other factors include the lack of own investment resources (63.4%), and the apparent ease of imitation by third parties (55.8%), which suggest that most companies have a low capacity to protect their innovations (Table 8). This is not new. The last report on the subject (SIC et al., 2017) indicates that the country is lagging behind in Latin America. Although there is a growing trend in the number of patent applications submitted, as well as in brands, the ownership of such applications is mostly in the hands of foreign residents (e.g., parent company where application originates).

Finally, when examining the obstacles to innovation by firm size, it is found that they are not equal for all. In large firms, uncertainty and low profitability of innovation are the protagonists, while among small and medium-sized firms the scarcity of own resources and uncertainty are more important. Subsequently, the weak protection of innovation affects all firms and, interestingly, the difficulty of accessing external financing appears in a secondary position among the obstacles examined (Table 8).

A typical traditional analysis

In order to deepen the issue of financing innovation in Colombian manufacturing firms, we carried out an approach similar to Sierra et al. (2009) and Barona et al.’s (2015). The analysis confirms the existence of a particular pecking order in which financing with internal resources predominates and is more pronounced in large companies due, presumably, to their greater liquidity (Table 9).

This is consistent with the great importance (second place in preferences) of external resources, mostly private bank loans, to finance innovation in SMEs despite their higher relative cost. Indeed, it reveals a paradoxical fact that configures a curious preference system (reversed pecking order) since the resources of public financing, which are less expensive than private, appear only in a third place of the classification and below private bank loans (Table 10).

This is quite curious among Micro and SMEs, since microenterprises go to private bank loans more than small and medium enterprises and use public funds much less than the others (Table 10). This is especially striking given the fact that commercial bank loans should usually be guaranteed by real collateral that these companies do not usually have.

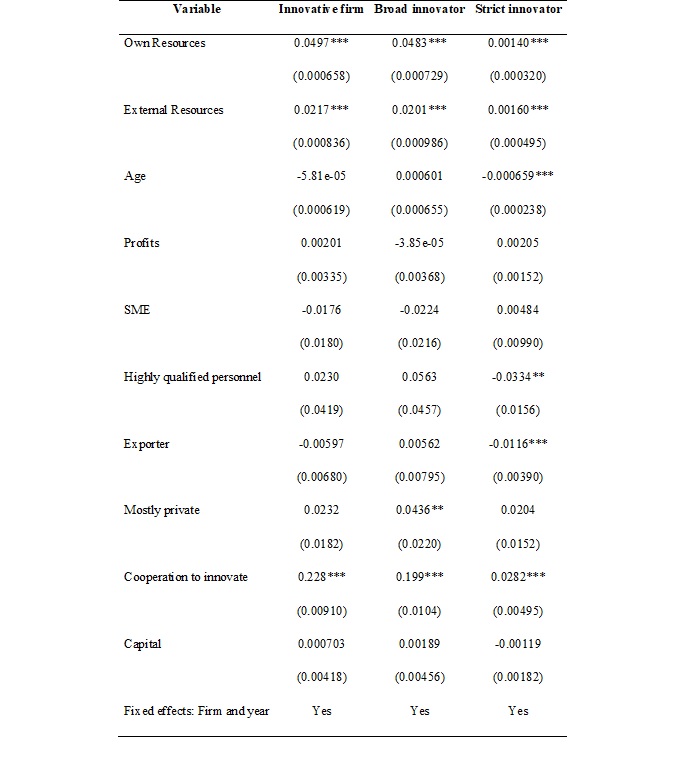

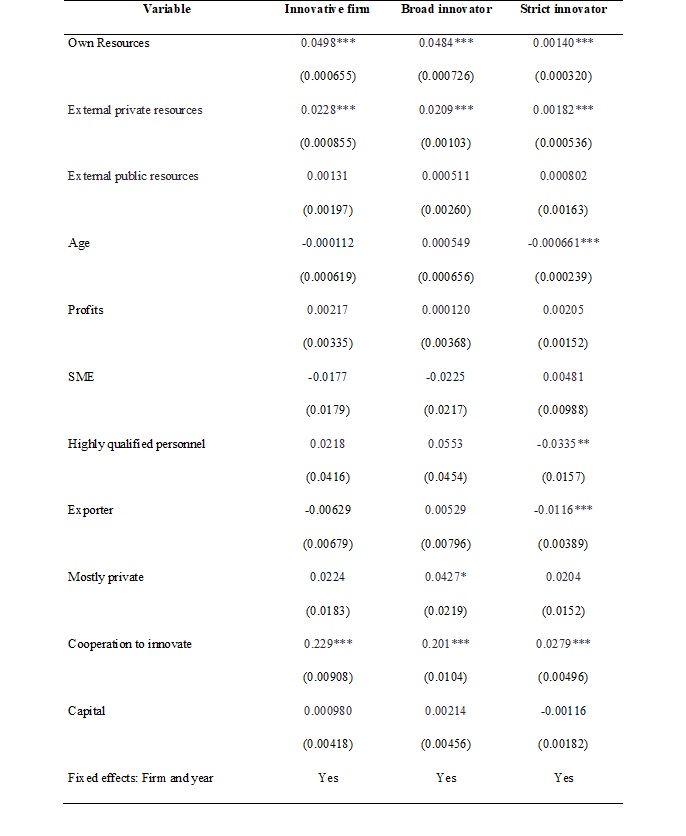

To confirm these descriptive findings, the following econometric analysis is carried out: A fixed effects panel estimation, which allows the mitigation of possible biases of unobservable variables that can be controlled as long as these factors are time invariant. The fixed effects model is shown in equation (1) and includes variables regarding the characteristics of each firm and each period of observation time8:

Equation (1)

Equation (1)Where  corresponds to either innovative firms (IF), strict innovators (SI) and broad innovators (BI). A

corresponds to either innovative firms (IF), strict innovators (SI) and broad innovators (BI). A  vector of control variables is also included, which is described later.

vector of control variables is also included, which is described later.  and

and correspond to the firm and time fix effects dummies, along with their correspondent coefficients,

correspond to the firm and time fix effects dummies, along with their correspondent coefficients,  and

and  .

.

In the case of the independent variables  , we used the different financing sources described in the innovation survey –internal resources and external resources were used, which were divided as follows: Internal resources include own resources and resources of the business group; external resources include public resources, resources from other companies, resources from private banks, private capital, and cooperation and donation resources.

, we used the different financing sources described in the innovation survey –internal resources and external resources were used, which were divided as follows: Internal resources include own resources and resources of the business group; external resources include public resources, resources from other companies, resources from private banks, private capital, and cooperation and donation resources.

In addition, the control variables  used were: Firm age, logarithm of the value of the firm's annual profit, SME dummy, the percentage of highly qualified personnel employed, exporter dummy, privately owned dummy, cooperation for innovation dummy, and logarithm of value of firm’s annual capital (property, plant and equipment).

used were: Firm age, logarithm of the value of the firm's annual profit, SME dummy, the percentage of highly qualified personnel employed, exporter dummy, privately owned dummy, cooperation for innovation dummy, and logarithm of value of firm’s annual capital (property, plant and equipment).

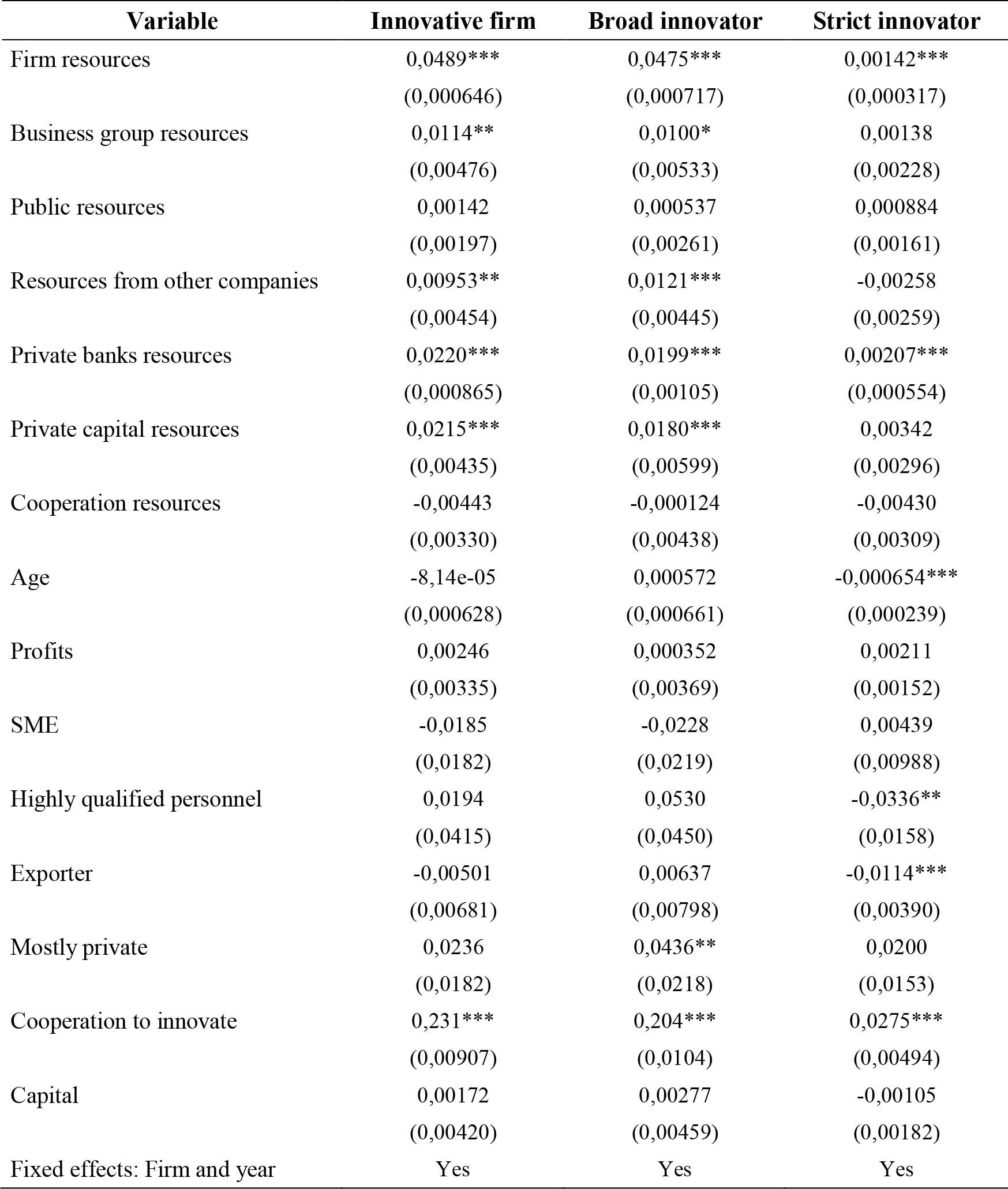

The econometric analysis (signs and magnitudes of the coefficients and levels of significance) confirms the paradox described by the reversed pecking order both under the general concept of innovative firms, and in its disaggregation by levels of innovation where even public resources are not significant as explanatory variable (Tables 11a and 11b).

Another variant of the model indicates that the established preference structure is more pronounced in less innovative firms, which may be explained by lower levels of uncertainty and risk related to innovation processes/products (Table 11C).

An alternative explanatory approach

Although the previous exercise reveals some interesting specificities about the Colombian case, it also evidences the limitations of the traditional theoretical approach because there is no satisfactory explanation about the mentioned particularities.

Therefore, an alternative approach and explanatory model are proposed here. In particular, three concepts are operationalised through the construction of the corresponding explanatory variables that are incorporated into the econometric models: Knowledge Incorporation and Consolidation System (KICS)9, interaction among actors (including those of the IFS)10, and Dedicated Investors (with specific characteristics)11. Their contribution is explained below.

The construction of proxy variables that measure the KICS, the interaction between actors, and dedicated investors, was carried out exclusively with the information from the Colombian Innovation Survey. For the construction of the interaction among actors proxy, the variable included dedicated investors plus all the relationships that the firm has with the rest of the actors of the National System of Competitiveness, Science and Technology (SNCCTI, in Spanish) and also, with the financing of STI activities. On the other hand, the construction of the KICS proxy includes the two previous variables plus the fact that the firm is innovative (a detailed explanation of the construction of each variable is in Appendix A).

As indicated, this construction imposes the need to estimate three different models: One for the KICS, another for the interaction between actors, and a last one for the dedicated investors, since including all three variables in a single model results in collinearity problems among these variables. This becomes a limitation (obstacle) on the use of EDIT surveys to study the phenomenon of financing innovation in Colombia because there are no other sources of information to measure the degree of interaction among SNCCTI actors and to identify whether an investor is generalist or dedicated, independently of the construction of the KICS variable.

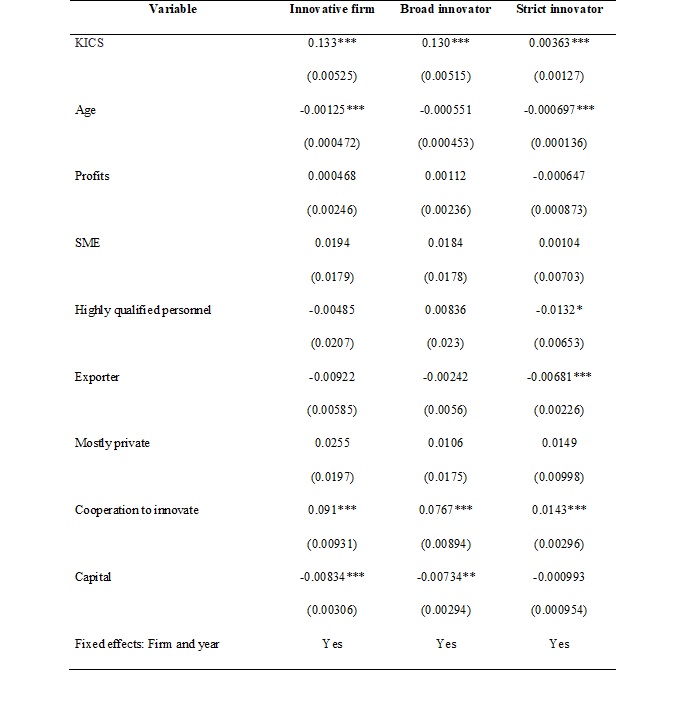

The econometric analysis shows that having a KICS turns out to be important and significant for the innovative firm, although its effect seems more accentuated in BI and more tenuous in SI. This result supports the importance of different types of knowledge that can be gathered from the construction of networks with other actors linked to innovation issues in order to search for financial resources (Table 12a).

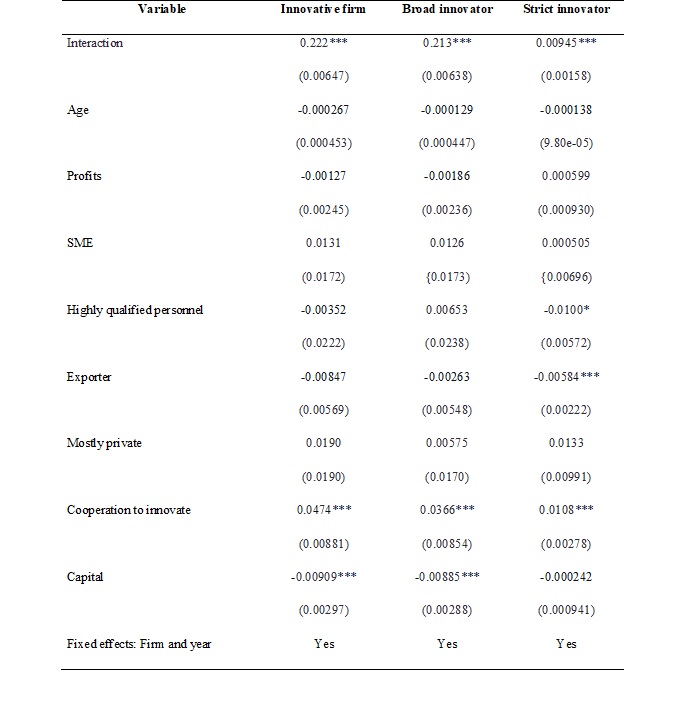

Moreover, the variable Interaction (with potential investors) is incorporated into the analysis and, as expected, the results are also significant and positive for all categories of innovative companies. However, the effect of the variable is greater for the BI than for the SI, again (Table 12b).

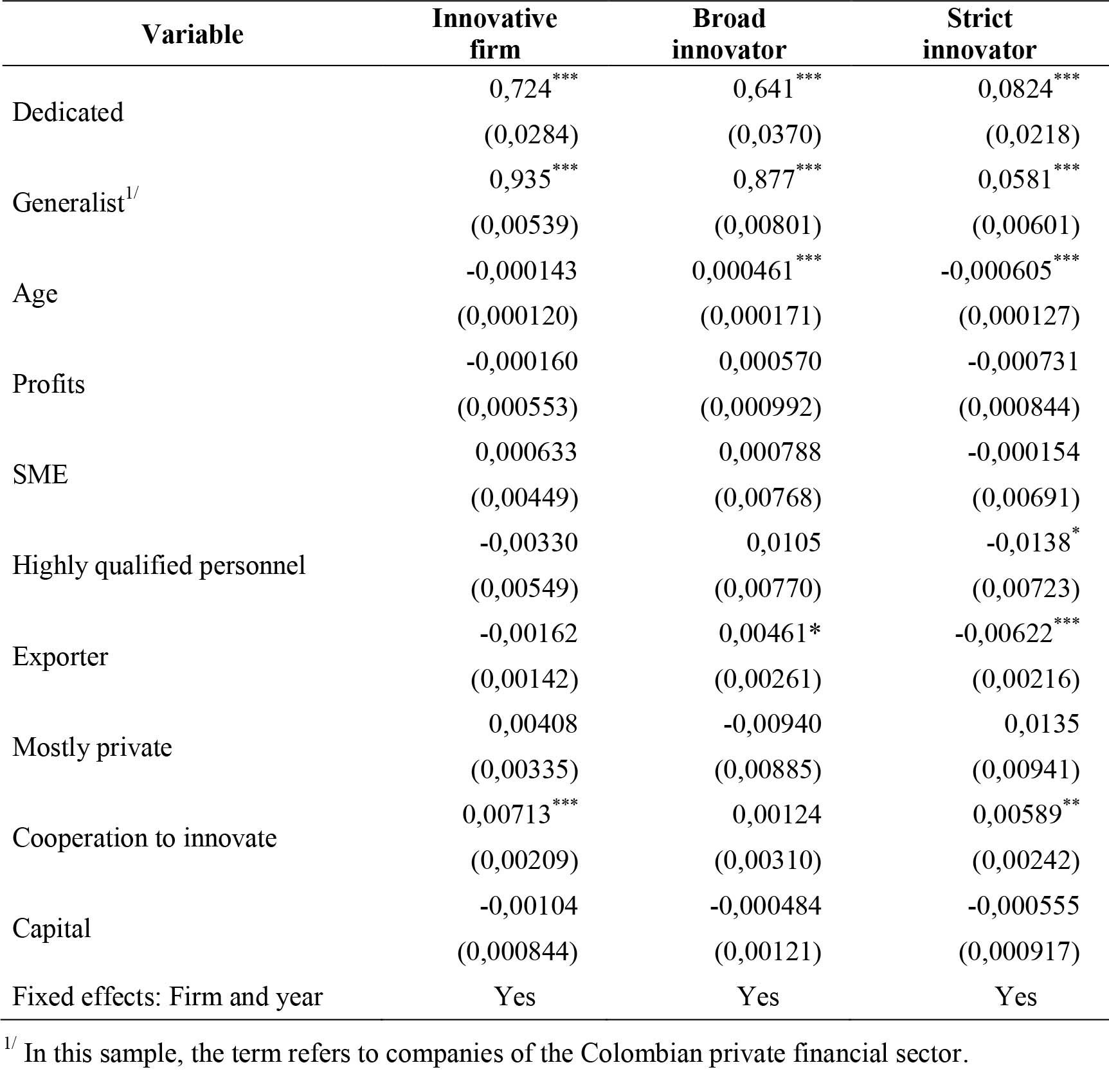

Finally, a variable is incorporated to differentiate generalist investors (those who use the typical diversification strategy of a portfolio of projects financed in many sectors / sub-sectors) from dedicated investors (those who concentrate their investments and knowledge in few sectors / subsectors) (see Figure 1). At first, the importance of the availability of generalist investors is greater than that of those dedicated to both the general (IF) and the BI categories. For the most innovative companies (BI), on the other hand, the availability of dedicated investors is more important (Table 12c).

Results and discussion

These results confirm two facts described in previous research: 1) the existence of an atypical pecking order in the financing preferences of innovative firms; 2) the paradox involved in the order of such preferences: Although firms argue a shortage of own resources, innovative firms prefer to leverage their projects on such resources and, when those resources are not sufficient, they prefer to obtain loans from commercial banks rather than using the most convenient (cheaper) public resources (subsidies and loans). This might be attributable to either lack of trust in public funders, red tape or sheer ignorance about such funding.

These stylised facts are not satisfactorily explained by traditional theories (see above). Neither the financial explanations (POT, PST, AST), nor those with a sociological basis (CST) (Table 3), nor the normative variants of POT (Sau, 2007) can account for the two results mentioned above for the Colombian case. Therefore, it is proposed that the alternative approach (Sierra, 2014; Sierra, 2020) can offer a better understanding of the phenomena described.

How is the Colombian situation explained?

Colombian innovative firms and potential investors do not know the national/regional/sectoral STI system well enough, including its Institutionalised Financial System. This implies that firms do not know precisely which and how many sources and viable financing mechanisms exist in their environment, and that investors also do not know which firms propose innovation projects. Such ignorance hinders, at least, the interaction and deployment of the necessary strategies to build and secure the necessary ‘financing relationships’ to guarantee the development of innovation projects. This situation creates a ‘compartmentalisation’ of the spheres of action and decision of firms that own the projects and of potential external investors, which gives rise to the phenomenon described.

This ignorance (incompleteness of the KICS of both actors) is partially explained by some contextual problems and interaction mechanisms (e.g., non-existent or inaccessible information, lack of contact between actors, inadequate public policy, lack of experience in negotiations). This problem is enhanced by the non-existence or insufficiency of financing sources/mechanisms in the national/regional/sectoral environment (e.g., shortage of venture capital dedicated to high technology sectors in Colombia) and the knowledge gap between project owners and potential investors (related, among other things, to the scarce contact between companies and funders).

In this context, at least three of the four premises enunciated above are not fully met and do not explain, at least in part, the problems described in the Colombian case. In short, if the individual actors do not know the rest of the STI system, the players and their dynamics; if there are no contextual mechanisms that favour the relationship among the actors; if they lack experience and do not implement mechanisms for facilitating interaction; if the different types of knowledge involved in the KICS are not updated; if the two parties (project and/or fund supply) do not act proactively; if interaction does not involve the strategic keys of both parties; if dedicated investors do not emerge, it will be very difficult to promote effective financing of innovation even if there is, somewhere, availability of sufficient funds.

The resolution of the Colombian paradox and the scarcity of financing for innovation in the country involves understanding the aforementioned problems and generating adequate conditions for their solution.

How can adequate solution conditions be generated?

Although the problems of financing innovation are usually assumed under the traditional financial logic of availability and cost, there are more comprehensive perspectives that involve factors ignored by the existing literature. Some of the deficiencies mentioned for the Colombian case give rise to specific proposals to improve the explanatory models and the existing mechanisms in the daily reality of innovation ecosystems. In this sense, some specific actions are suggested here:

To study the reasons guiding the decisions of both firms and investors. This includes strengthening and complementing the Innovation Surveys, since the existing information is clearly insufficient to understand the phenomenon of financing innovation in Colombia. Sectoral 360 degrees (involving all actors), mixed and in-depth studies are a relevant alternative.

To promote/build contextual factors and mechanisms (e.g., networks, support organisations, SFI) that facilitate mutual knowledge of the actors within the innovation system framework and favour their relationship and interaction with specific purposes.

Actors must become aware of the need to build and update their KICS. Concurrently, they must determine their level of proactivity or reactivity in relation to their needs, particularly those of financing, according to the strategic framework of their projects.

Actors of all levels should favour the emergence (incorporation, transformation) of dedicated investors that complement the presence and activity of generalist funders (specialised or not) in the National Innovation and Competitiveness System.

The financing of innovation must be actively and deeply incorporated into the National Innovation System governance agenda if we want to have a holistic view of the problem.

Conclusions and implications

The financing of innovation in Colombian firms falls into the atypical set of cases of hierarchical preferences (reversed pecking order) described in the literature, but with the aggravating circumstance that its structure implies a paradox that no traditional theory can explain.

The explored alternative theoretical approach offers insights into the factors and dynamics that underlie the Colombian phenomenon and allows us to suggest exit routes and potential solutions appropriate to the relevant context. In general, there is a need to deepen the study of the financing of innovative business projects in Colombia and to articulate it with the study of National Innovation System governance at different levels, and from a sectoral perspective, to facilitate a better understanding of the reasons of the problems and to formulate different approaches aiming at pertinent solution conditions.

Among other things, it is evident that the information obtained through the Innovation Survey is not enough, so it is urgent to raise new quantitative and qualitative information through broad and deep sectoral approaches that involve all the actors of the innovation system and subsystems. This means that the academy and the other actors of the System must assume a more active and inquisitive role in terms of the nature and functioning of the system.

Ethical considerations

No particular ethical considerations have been highlighted or addressed at any point concerning this research.

Authors' contributions statement

The authors declare they have contributed to the final version of this manuscript (data analysis and interpretation, article drafting, review and editing). J. Sierra-Gonzalez directed the research project of which this paper is an outcome.

Interest conflicts

The authors have no conflicts of interest to declare.

Financing

This research outcome has been funded by Pontificia Universidad Javeriana through a Research Vice-President’s Office grant.

References

Amit, R., Brander, J., & Zott, C. (1998). Why do venture capital firms exist? Theory and Canadian evidence. Journal of Business Venturing, 13, 441-466. https://doi.org/10.1016/S0883-9026(97)00061-X

ANIF Centro de Estudios Económicos (2017). La Gran Encuesta Pyme – Lectura Nacional. Informe de resultados 2do. Semestre 2017.

Barona, B., Rivera, J. A., Aguilera, C. (2015). Análisis de la relación de la innovación empresarial con la financiación en Colombia. Cuadernos de Administración, 28(50), 11-37. https://doi.org/10.11144/Javeriana.cao28-50.arie

Becchetti, L., & Sierra, J. (2002). Financing innovation: Trodden and unexplored paths. Cuadernos de Administracion, 15(24), 7-40. https://www.redalyc.org/articulo.oa?id=20515242

Bertoni, F., Colombo, M., & Grilli, L. (2011). Venture capital financing and the growth of high-tech start-ups: disentangling treatment from selection effects. Research Policy, 40(7), 1028-1043. https://doi.org/10.1016/j.respol.2011.03.008

Bertoni, F., & Tykvova,T. (2012). Which form of venture capital is most supportive of innovation? Discussion Paper 12-018, ZEW.

Bygrave, W., & Timmons, J. (1992). Venture capital at the crossroads. Boston, MA: Harvard Business School Press.

Eckhardt, J. T., Shane, S., & Delmar, F. (2006). Multistage selection and the financing of new ventures. Management Science, 52, 220-232. https://doi.org/10.1287/mnsc.1050.0478

García, D., Barona, B., & Madrid, A. (2013). Financiación de la innovación en las Mipyme iberoamericanas. Estudios Gerenciales, 29, 12-16. https://doi.org/10.1016/S0123-5923(13)70015-9

Gompers, P., & Lerner, J. (1998). Venture Capital Distributions: Short and Long run Reactions. Journal of Finance, 53, 2161-2183. https://doi.org/10.1111/0022-1082.00086

Gompers, P., & Learner, J. (2001). The venture capital revolution. Journal of Economic Perspectives, 15(2), 145-168. https://doi.org/10.1257/jep.15.2.145

Gulati, R., & Higgins, M. (2003). Which ties matter when? The contingent effects of interorganizational relationships on IPO success. Strategic Management Journal, 24, 127-144. https://doi.org/10.1002/smj.287

Hall, B. H., & Lerner, J. (2010). The financing of R&D and innovation. In: B. Hall & N. Rosenberg (eds.), The Handbook of the Economics of Innovation (pp. 610-639). Oxford: Elsevier.

Hallen, B. (2008). The causes and consequences of the initial network positions of new organizations: From whom do entrepreneurs receive investments. Administrative Science Quarterly, 53, 685-718. https://doi.org/10.2189/asqu.53.4.685

Hallen, B., & Eisendhardt, K. (2012). Catalyzing strategies and efficient tie formation: How entrepreneurial firms obtain investment ties. Academy of Management Journal, 55(1), 35-70. https://doi.org/10.5465/amj.2009.0620

Jiménez, L. F. (2008). Capital de riesgo e innovación en América Latina. Revista de la CEPAL, 96, 173-187. http://hdl.handle.net/11362/11287

Knockaert, M., Clarysse, B., & Wright, M. (2010). The extent and nature of heterogeneity of venture capital selection behaviour in new technology-based firms. R&D Management, 40(4), 357-371. https://doi.org/10.1111/j.1467-9310.2010.00607.x

Mina, A., & Lahr, H. (2011). Venture capital in Europe: Recovery, downsizing or breakdown? FINNOV Discussion Paper, Document FP7-SSH-2007-1.2.3-217466-FINNOV-D3.2.

Myers, S., & Majluf, N. (1984). Corporate financing decisions when firms have investment information that investment do not. Journal of Financial Economics, 13, 187-221. https://doi.org/10.1016/0304-405X(84)90023-0

OCyT - Pardo, C. I. & Cotte, A. (eds.) (2018) Science and Technology Indicators 2017, Observatorio Colombiano de Ciencia y Tecnología, Bogotá.

Otálora, D., Hurtado, R., & Quimbay, C. (2009). Interés de las empresas por la financiación de sus actividades de I+D+i: un análisis en el marco de las redes complejas para el sector industrial manufacturero colombiano. En: J. Robledo, F. Malaver & M. Vargas (eds.), Encuestas, datos y descubrimiento de conocimiento sobre la innovación en Colombia, Bogotá: Colciencias.

Powell, W., Koput, K., Bowie, J., & Smith-Doerr, L. (2002). The spatial clustering of science and capital: Accounting for biotech firm-venture capital relationships. Regional Studies, 36(3), 291-305. https://doi.org/10.1080/00343400220122089

Sau, L. (2007). New pecking order financing for innovative firms: an overview. Working Paper N. 02, Department of Economics, University of Turin, Italia.

Sierra, J. (2014). Financing innovation in bio-pharma: a sectoral systems approach. PhD Thesis, Manchester Business School, University of Manchester.

Sierra, J. (2018). La cuarta hélice y la financiación de la innovación. Journal of Economics, Finance and Administrative Science, 23(45), 128-137. https://doi.org/10.1108/JEFAS-01-2018-0014

Sierra, J. (2020). How financial systems and firm strategy impact the choice of innovation funding. European Journal of Innovation Management, 23(2), 251-272. https://doi.org/10.1108/EJIM-07-2018-0147

Sierra, J., Malaver, F., & Vargas, M. (2009) “La financiación de la innovación: un análisis a partir de la encuesta de innovación de Bogotá y Cundinamarca”, en J. Robledo, F. Malaver y M. Vargas (Eds.), Encuestas, datos y descubrimiento de conocimiento sobre la innovación en Colombia. Bogotá: Colciencias.

Superintendencia Financiera de Colombia (2017). Reporte de Inclusión Financiera 2016. Bogotá.

Superintendencia de Industria y Comercio - SIC, WorldIntellectual Property Organization, Departamento Nacional de Planeación, Instituto Colombiano Agropecuario, Dirección Nacional de Derechos de Autor, Ministerio de Relaciones Exteriores - Cancillería (2017). Reporte sobre la información en materia de Propiedad Intelectual en Colombia. Septiembre, Bogotá.

Tylecote, A., & Visintin, F. (2008). Corporate governance, finance and the technological advantage of nations. Routledge, Oxon (UK).

Ullah, F., Abbas, Q., & Akbar, S. (2009). The relevance of pecking order hypothesis for the financing of computer software and biotechnology small firms: Some UK evidence. International Entrepreneurship and Management Journal, 6(3), 301-315. https://doi.org/10.1007/s11365-008-0105-0

APPENDIX A

Knowledge Incorporation and Consolidation System (KICS). Firms’ system that involve existing and new knowledge necessary to innovate in a given sector, to find and negotiate financing for projects, the technical financial knowledge, and the knowledge that underlies the capacity to create networks. This variable was built based on questions in Chapter I - Innovation and its impact on the company - numeral I.1

Indicate if your company introduced any of the following innovations: New goods or services only for your company (They already existed in the national market and / or in the international). New goods or services in the national market (They already existed in the international market). New goods or services in the international market. Goods or services significantly improved for your company (They already existed in the national and / or international market). Goods or services significantly improved in the national market (They already existed in the international market). Significantly improved goods or services in the international market. Introduced new or significantly improved methods of production, distribution, delivery, or logistics systems in your company. Introduced new organisational methods implemented in the internal workings of the company, in the knowledge management system, in the organisation of the workplace, or in the management of the external relations of the company. Introduced new marketing techniques in your company (Channels for promotion and sale or significant changes in packaging or product design), implemented in the company with the aim of expanding or maintaining its market (Changes that affect the functionalities of the product are excluded since this would correspond to a significantly improved good or service).

Chapter III of EDIT, numerals III.1 - Sources of the resources used to finance investments in innovation - private banking, private capital, cooperation or donations; numeral III.2 Origin of the amount of public resources used to innovate; numeral III.3 - Did the company intend to request public resources to finance its innovations?; numeral III.4 - Importance of the following obstacles to access public resources to innovate: ignorance of the existing public financing lines, lack of information on requirements and procedures, difficulty in complying with the requirements or completing the formalities, timeline excessive processing, financing conditions and / or co-financing unattractive, delay in intermediation between commercial banks or public credit lines. Chapter V. numeral V.1 - Indicate whether or not the following sources of information and knowledge were important for innovation: Internal R&D department, Production department, Sales and marketing department, Other department of the company, Specific interdisciplinary groups for innovation, Company executives, Other related company (if it is part of a conglomerate), Foreign parent company, R&D Department of another company in the sector, Competitors or other companies in the sector (except R&D department), Clients, Suppliers, Companies from another sector, Associations / sectoral associations, Chambers of Commerce, Technological Development Centres, Autonomous research centres, Incubators of Technology-Based Enterprises, Technology Parks, Regional Productivity Centres, Universities, Training centres / techno parks, Consultants, experts or researchers, Fairs and exhibitions, Seminars and conferences, Books, magazines or catalogues, Industrial property information systems (patent bank), Copyright information system , Internet, Scientific and technological databases, Standards and technical regulations, Public institutions (ministries, decentralised entities, secretariats); numeral V.2 - Relationship of the company with SNCTI stakeholders as support for the realisation of innovations -: Administrative Department of Science, Technology and Innovation (COLCIENCIAS), SENA, ICONTEC, Superintendence of Industry and Commerce (SIC), National Directorate of Authors’ Rights, Ministries, Universities, Technological Development Centres, Autonomous Research Centres, Incubators of Technology-Based Companies, Technology Parks, Regional Productivity Centres, Departmental Councils of Science and Technology, Regional Commissions of Competitiveness, Sectoral Associations and Chambers of Commerce, Consultants in Innovation and Technological Development, PROEXPORT - PROCOLOMBIA, BANCOLDEX, Technical and technological training entities (other than SENA); numeral V.3 - The company cooperated with one of the following partners for innovation-: Other companies of the same group (conglomerate), Suppliers, Customers, Competitors, Consultants, experts or researchers, Universities, Technological development centres, Autonomous research centres, Technological parks, Regional productivity centres, Non-governmental organisations, Government.

Interaction between actors. This variable refers to firms that interact among themselves and with financiers and have innovation networks in place. It was built on the basis of questions in Chapter III of Edit, numerals III.1 - Sources of resources used to finance investments in innovation - private banking, private capital, cooperation or donations; numeral III.2 Origin of public resources used to innovate; numeral III.3 - Did the company intend to request public resources to finance its innovations? - numeral III.4 - Importance of the following obstacles to access public resources to innovate -: ignorance of existing public financing lines, lack of information on requirements and procedures, difficulty in complying with requirements or completing formalities, timeline excessive processing, unattractive financing / co-financing conditions, delay in intermediation between commercial banks or public credit lines.

Chapter V.2 - Relationship of company with SNCTI stakeholders as support for innovation -: Administrative Department of Science, Technology and Innovation (COLCIENCIAS), SENA, ICONTEC, Superintendence of Industry and Commerce (SIC), National Directorate of Authors’ Rights, Ministries, Universities, Technological Development Centres, Autonomous Research Centres, Incubators of Technology-Based Companies, Technology Parks, Regional Productivity Centres, Departmental Councils of Science and Technology, Regional Commissions of Competitiveness, Sectoral Associations and Chambers of Commerce, Consultants in Innovation and Technological Development, PROEXPORT - PROCOLOMBIA, BANCOLDEX, Technical and technological training entities (other than SENA); numeral V.3 - The company cooperated with one of the following partners for innovation -: Other companies of the same group (conglomerate), Suppliers, Customers, Competitors, Consultants, experts or researchers, Universities, Technological development centres, Autonomous research centres, Technological parks, Regional productivity centres, Non-governmental organisations, Government.

Dedicated Investors. Here defined as specialised public entities (e.g., Colciencias, managers of royalty funds for CTI) that finance innovation.

APPENDIX B

Notes

*

Research paper.

1

Formerly known as the Administrative Department of Science and Technology –Colciencias–, it is the entity in charge of promoting public policies to foster science, technology and innovation in Colombia.

2

In addition, a survey inquired about access to resources through private equity funds or entrepreneurial support (VC: Venture Capital). However, only 6% of the three macro sectors answered affirmatively, while the remaining 94% answered that they had not accessed to resources through these means. (ANIF, 2017).

3

In 2016, however, only 30% of Colombian companies had a banking product, savings and checking accounts mostly. No more than 15% of the companies had any type of bank loans (Superintendencia Financiera de Colombia, 2017).

4

In particular, “The resources requested by SMEs from the three macro-sectors to the financial system were mainly used for working capital during the first half of 2017 (59% in industry, 65% in commerce and 39% in services). In second place, these resources were used for the consolidation of liabilities (35% in industry, 34% in commerce and 39% in services). The third destination of the resources for the industrial sector (14%) and commerce sector (12%) were renovations or adjustments, while in the service sector it was the purchase or lease of machinery (14%).

Regarding alternative sources of financing, 42% respondents in industry, 44% in commerce, and 41% in services did not access any source of financing other than bank loans in the first half of 2017. The suppliers were the most important source of alternative financing for SMEs in industry (27%) and commerce (29%), while financing with own resources was for service firms (28%). The use of other alternative sources continues to be uncommon, as in the case of leasing (4% in industry, 2% in commerce and 5% in services) and factoring (between 3% and 4% of SMEs). On the other hand, the non-banking market was the option least used by SMEs (less than 1% for the three macro sectors).By size, it is observed that the percentage of small firms that do not access other sources of financing is the same as in medium size firms of the industry sector (42%); it is higher in the case of the commerce sector (46% in small vs. 37% in medium) and lower in the case of the service sector (40% in small vs. 44% in medium). In turn, the medium-sized companies of the three macro-sectors use the leasing tool more (7% -8% of respondents) compared to their small peers (1% -4%).” (ANIF, 2017 – Our translation and underlining).

5

This value changes every year according to the Producer Price Index.

6

The size is given by the book assets of the firm: Micro: up to 500 minimum wages, Small: between 500 and 5,000 minimum wages, Medium: between 5,000 and 30,000 minimum wages, Large: more than 30,000 minimum wages, according to Law 905 of August 2 of 2004. (Ministry of Industry, Commerce and Tourism)

7

Types of innovative firms (IF): Broad innovators (BI): It implies obtaining a new or improved good or service for the national market or for the company, and / or the implementation of a new productive or improved process for the main or complementary production line. Strict innovators (SI): Companies that obtain new or significantly improved goods or services for the international market in the exercise of innovation activities. Prospective (PI) innovators: Those companies that intend to innovate, but do not have any innovation project. Non-innovators (NI): Companies that did not obtain innovations, nor reported having in process, or having abandoned, any project to obtain innovations. Potential innovators (PtI): they report having or having abandoned an innovation process to obtain either a new or a significantly improved product for the national, international or company market. (Taken from EDIT).

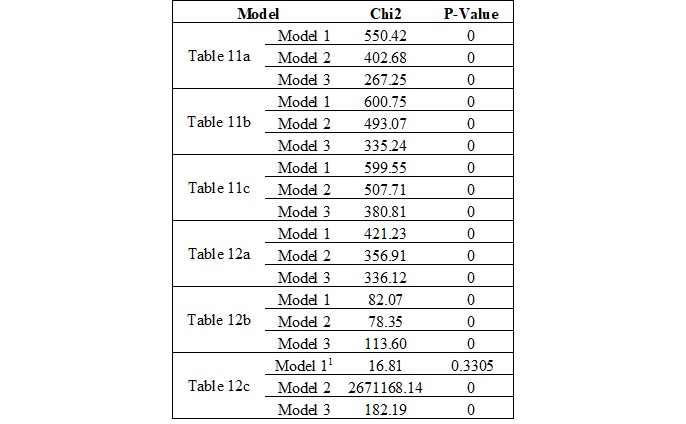

8

Additionally, a Hausman test was carried showing that the model that best adapts is fixed effects one. The result of this test for all regressions is shown in Appendix B.

9

Knowledge/capacities that firms have (additional to those necessary to innovate) and underlie their ability to create networks in order to seek and obtain financing for their projects (Sierra, 2014). This proxy was built on the basis of questions in EDIT V-VII, Chapter I - Innovative company in any sense (Question 1.1); Chapter III - Financing of STI activities (Questions 3.1, 3.2, 3.3 and 3.4); Chapter V - Relations with SNCCTI Actors (Questions 5.1, 5.2 and 5.3).

10

Knowledge about potential funders built by companies through their networks. The interaction proxy was built on the basis of EDIT V-VII, Chapter III - Financing of STI activities (Questions 3.1, 3.2, 3.3 and 3.4) and Chapter V - Relations with SNCCTI Actors (Questions 5.2 and 5.3).

11

Specialised public entities (e.g., Colciencias (now Minciencias), managers of royalty funds for STI) that finance innovation in Colombia.

Author notes

a Corresponding author. E-mail address: jhsierra@javeriana.edu.co

Additional information

Cited as: Sierra-González, J. H., Londoño-Bedoya, D. A., & García-Ospina, J. M. (2021). Innovation financing in Colombia: An explicative proposal. Cuadernos de Administración, 34. https://doi.org/10.11144/Javeriana.cao34.ifce