APA

ISO 690-2

Harvard

Haga clic en un formato de citación

Public Sector (Un)Sustainability: a study of GRI adherence and sustainability reporting disclosure standards in Public Institutions and State-Owned Companies of the Public Agency Sector*

La In(sostenibilidad) del Sector Público: un estudio de la adherencia y de los patrones de divulgación de los informes de sostenibilidad por la GRI de las Instituciones Públicas y Estatales del Sector Agencia Pública

A In(sustentabilidade) do Setor Público: um estudo da aderência e dos padrões de divulgação dos relatórios de sustentabilidade pela GRI das Instituições Públicas e Estatais do Setor Agência Pública

Cuadernos de Contabilidad, vol. 20, no. 49, 2019

Pontificia Universidad Javeriana

Elyrouse Cavalcante de Oliveira Bellini a elyrouse@gmail.com

Universidade Federal de Alagoas, Brasil

Raimundo Nonato Rodrigues

Universidade Federal de Alagoas, Brasil

Umbelina Cravo Teixeira Lagioia

Universidade Federal de Alagoas, Brasil

Maurício Assuero Lima De Freitas

Universidade Federal de Alagoas, Brasil

Date received: 04 October 2018

Date accepted: 04 March 2019

Date published: 30 June 2019

Abstract:

This study aims to analyze the GRI adherence and disclosure standards of sustainability reports of public and state institutions in the public agency sector. The Global Reporting Initiative Database (GRI) is used for the period 2011-2017, with a sample composed by 177 public agencies. The results show that there is an evolution in the publication of GRI sustainability reports by the public agencies analyzed. However, they represent only 1.8% of the total of all organizations. In addition, a large part does not correspond to the category of integrated reports, received no external assurance, and did not formalize any input or feedback on the report provided by a panel of stakeholders or expert(s), resulting in reports with poor quality and reliability.

JEL Codes: M14, H83

Keywords: Public sector, disclosure, GRI, sustainability reports.

Resumen:

Este estudio tiene como objetivo analizar la adherencia y los patrones de divulgación de las instituciones públicas y estatales del sector agencia pública, en los informes de sostenibilidad de la Global Reporting Initiative (GRI). El estudio cubre el período de 2011 a 2017, en una muestra compuesta por 177 agencias públicas. Los resultados demuestran que hay una evolución en la publicación de informes de sostenibilidad por parte de las agencias públicas analizadas. Sin embargo, éstas sólo representan el 1,8% del total de todas las organizaciones. Además, una gran parte de las publicaciones no corresponde a la categoría de informes integrados, no hizo el servicio de aseguramiento externo, ni utilizó contribuciones formalizadas ni retroalimentación por un panel de interesados o expertos. Estas características tienden a dar como resultado la publicación de informes con baja calidad y confiabilidad.

Códigos JEL: M14, H83

Palabras clave: Sector público, divulgación, GRI, informes de sostenibilidad.

Resumo:

Este estudo tem como objetivo analisar a aderência e os padrões de divulgação dos relatórios de sustentabilidade das instituições públicas e estatais do setor agência pública nos relatórios da Global Reporting Iniciative (GRI). O estudo cobre o período de 2011 a 2017, em uma amostra composta por 177 agências públicas. Os resultados demonstram que há uma evolução na publicação de relatórios de sustentabilidade pelas agências públicas analisadas. Entretanto, elas representam apenas 1,8% do total de todas as organizações. Além disso, grande parte das publicações não corresponde à categoria de relatórios integrados, não fez o serviço de asseguração externa, nem utilizou contribuições formalizadas sobre o relatório fornecidas por um painel de interessados ou especialistas. Estas características tendem a dar como resultado a publicação de relatórios com baixa qualidade e confiabilidade.

Códigos JEL: M14, H83

Palavras-chave: Setor público, divulgação, GRI, relatórios de sustentabilidade.

Introduction

In the 1980s, sustainability evolved as a key concept in global developmental policies, making it necessary to take sustainability into consideration when defining social and economic development objectives, given that they bring about transformations in society and in the economy. In 1987, during the academic debates surrounding the UN World Commission on Environment and Development (WCED), emphasis was placed on the definition of sustainable development. Preparations for the 1992 United Nations Conference on Environment and Development, also known as the Rio de Janeiro Earth Summit, resulted in the publication of Our Common Future, also known as the Brundtland Report, which is based on the idea that human beings must utilize natural resources within their capacity for renewal in order to prevent their depletion (Brundtland, 1991).

Although the essential concept continues to be fairly clear, since 1992 several other definitions have been attributed to the term “sustainable development” (Wackermann, 2008), resulting in numerous debates and differing interpretations within the literature (Ciegis & Zeleniute, 2008). The definition provided by the Brundtland Report (1991), namely that sustainable development “meets the needs of the present without compromising the ability of future generations to meet their own needs,” is one of the most widely cited concepts and one of the most effective in disseminating the idea of sustainable development (Ciegis, Ramanauskiene & Martinkus, 2009; Riedner, Ribeiro, Brandalise & Bertolini, 2018). This definition includes core concepts such as “needs,” primarily of people living in poverty throughout the world, and “limitations” to the environment’s capacity to meet the needs of the present and the future, brought about by the effects of technology and social organization.

According to this definition, organizations are challenged to operate sustainably (considering environmental, social, and economic aspects), due to numerous situations that affect the economy and society as a whole such as climate change and the overconsumption of natural resources. Therefore, organizations must seek to understand and respond both; to how these issues will affect their longevity and long-term success, and to how they may contribute to society so that it may face these challenges (Hopwood, Unerman & Fries, 2010). Due to the existence of a wider range of accounting and accountability techniques capable of contributing to management, control, planning, and accountability towards their social and environmental impacts (Unerman, Guthrie & Striukova, 2007). The organizations are seeking to disclose information not restricted to that which is already included in financial accounting. In order to provide this information and disclose standards to stakeholders, various institutions have developed “guidelines” for sustainability reporting (SR), the preeminent reports being those produced by the Global Reporting Initiative (GRI) (Brown, Jong & Levy, 2009; Dumay, Guthrie & Farneti, 2010; KPMG International, 2013).

In the field of “public services” defined by Broadbent and Guthrie (2008) as “those activities which are enshrined within the notion of public good or service based on universality of access for the citizenry,” there is consistently increasing pressure on these organizations to be led in accordance with sustainability practices (Gray, Adams & Owen, 2014; Ball, Grubnic & Birchall, 2014), given that they are indispensable in providing sustainable development, insofar as they are responsible for the public policies that guarantee a broad range of services (Guthrie & Farneti, 2008). For example, the ability for a local government to take on a central role within the community in the search for a more sustainable future. In the event that this leadership does occur, citizens may find themselves excluded from sustainable lifestyles (Ball, Broadbent & Jarvis, 2006).

In spite the fact that the majority of research and learning on social and environmental accounting focuses on for-profit business organizations (Ball, Grubnic & Birchall, 2014; Greiling, Traxler & Stötzer, 2015; Guthrie & Abeysekera, 2006; KPMG International, 2013) the public sector (which includes the national government and its ministries, regional and local governments, health care, emergency services, public enterprises, educational and research institutions, and so on) takes on greater responsibilities than private entities and thus merits greater attention. It also has great potential for progress in sustainability and accountability (Ball, Grubnic & Birchall, 2014). In agreement with the previously cited authors, Gray et al. (2014) highlights that the public sector is potentially enormous and exceptionally diverse, consequently making its social and environmental accounting and accountability too important to be ignored; especially considering that 50% of a country’s economic activity and employees go through these organizations. Moreover, this broad sector has, in varying degrees, the capacity to establish the social, legal, and physical infrastructure inside of which the rest of society operates.

In view of this, attempting to contribute to the state of the public sector’s accounting research and relevance, this study sought to answer the following question: what are the GRI adherence and sustainability reporting disclosure standards in public institutions and state-owned companies of the Public Agency Sector?

Several factors justify the choice to study sustainability reports related to the public sector. First, it is considered central to providing of sustainable development (Dumay et al., 2010), that governments depend on sustainable factors when defining their agendas for meeting the overall objectives for which they are responsible (GRI, 2005); second, the public sector has the civic responsibility of properly managing public goods, resources, and facilities with the aim of supporting sustainable development objectives and promoting public interest, and its organizations should be open and transparent in managing their actions (Tort 2010). Due to their size and influence, public agencies are expected to take the lead by publicizing their activities in order to promote sustainability. However, their sustainability reports are proceeding more slowly than those of other sectors (Greiling & Grüb, 2014, Domingues, Lozano, Ceulemans & Ramos, 2017), and there is little research related to social and environmental accounting, accountability, and sustainability in the public sector and the third sector (Adams, Muir & Hoque, 2014; Alcaraz-Quiles, Navarro-Galera & Ortiz-Rodríguez, 2014; Domingues, Lozano, Ceulemans & Ramos, 2017; Dumay et al., 2010; Greiling et al., 2015), even though numerous authors have reported on its importance (Alcaraz-Quiles et al., 2014; Ball & Bebbington, 2008; Ball, Grubnic & Birchall, 2014; Ball & Osborne, 2011; Greiling et al., 2015; Gray et al., 2014). Additionally, many of the studies in this area are related exclusively to a single country or to a specific type of organization (Papenfuß, Grüb & Frieländer, 2015).

GRI standards for analysis are used due to the fact that they create a common language for organizations’ sustainability reports, leading to a better understanding on the part of their stakeholders, which improves both global comparability and the quality of information provided, therefore generating greater transparency and accountability (Hopwood et al., 2010). Ball, Grubnic e Birchall (2014) add that they present good efforts in analyzing development internationally. They are also the most widely used sustainability reports (Adams, Muir & Hoque, 2014; Dumay et al., 2010, 2010; KPMG Internacional, 2013, Yadava & Sinha, 2016).

Literature review

According to the GRI Standards (2018) issued by the Global Sustainability Standards Board (GSSB), sustainability reports are related to the organizational act of publicly reporting economic, environmental, and/or social impacts, whether positive or negative, with the objective of promoting sustainable development. These standards create a common language for organizations and their stakeholders and in this manner, the information contained therein is easily understood, enabling stakeholders to form opinions and make decisions. Furthermore, they allow for global comparability and for improvements in the quality of information that make greater transparency and organizational responsibility possible. According to Goswami and Lodhia (2014), they highlight organizations’ performance in relation to economic, social, and environmental issues. Within the public sector, they are essential (GRI, 2005) for enabling citizens to judge the extent to which a respective level of government provides social welfare (Macintosh & Wilkinson, 2012).

According to Costa and Crisóstomo (2017), whatever an organization’s motivations for publishing SR may be, they must transmit enough information and quality to meet stakeholder demands so that the stakeholders may evaluate their actions. Goswami and Lodhia (2014) add that SR is an important means for assessing an organization's performance in relation to economic, social, and environmental issues. Within the public sector, SR are essential for enabling citizens to judge the extent to which a respective level of government provides social welfare (Macintosh & Wilkinson, 2012). &&

Among several guidelines developed for organizations to report their sustainability information, GRI is the most widely used (Adams, Muir & Hoque, 2014, Dumay et al., 2010, KPMG International, 2013, Yadava & Sinha, 2016). In the event that an organization claims that its sustainability report was prepared in accordance with GRI Standards, it is fundamental that the organization observes GRI’s Reporting Principles. These are divided into two groups: Principles for Defining Report Content, which guides choices on identifying content which should be included in the report, such as taking the organization’s activities, their impacts, and the expectations and interests of its stakeholders into account, and Principles for Defining Report Quality, which guide choices on ensuring the quality of information reported, including its presentation, which enables stakeholders to make sound and reasonable assessments of performance and to take appropriate actions. The principles in the first group are: Stakeholder Inclusiveness, Sustainability Context, Materiality, and Completeness. The second group is composed of the following six principles: Balance, Comparability, Accuracy, Timeliness, Clarity and Reliability (GRI, 2018).

Report Content is divided into Universal Standards (the 100 series, which includes three sets of standards: GRI 101 Foundation, GRI 102 General Disclosures and GRI 103 Management Approach) and Topic-Specific Standards (the 200, 300 and 400 series).

In addition to the general information requested in the Guidelines, GRI recognizes the need to develop complementary sector-specific disclosures in the form of supplements, with the purpose of enabling the preparation of robust, useful reports and to extend their applicability and comprehension by sectors worldwide. In 2005, in accordance to 2002 Guidelines, GRI developed a sector supplement denominated “GRI Sector Supplement for Public Agencies” (GRI, SSPA, 2005) specifically for general use by public agencies operating on all levels of government (ministries; federal agencies, regional governing bodies, state agencies, city councils, departments, etc.) covering public policies and implementation measures, expenditures, procurement, and administrative efficiency. This supplement allows the possibility to include three types of information: Organizational Performance, Public Policies and Implementation Measures, and Context or State of Environment. However, the focus of the supplement are the first two types.

Even though SR brings innumerable advantages to the sector, such as promoting transparency and accountability, improving internal governance, and highlighting the importance of their role as consumers and employers in various economies, there is little evidence on current SR practices in the public sector (Farneti & Guthrie, 2009). Furthermore, Cruz, Marques, and Ferreira (2009) emphasize the importance of the State in promoting the common good; given that the environment is a common good, its management and defense are state functions. Hence, its actions should be widely and transparently disclosed through reports issued by Accounting.

Because GRI is the most used guideline, most studies use it as a basis. The following section, therefore, focuses on previous studies that used the GRI as a study basis.

Guthrie and Farneti (2008) analyzed voluntary SR reporting practices in seven Australian public sector organizations that use the GRI G3 Guidelines and the GRI Sector Supplement for Public Agencies (2005). They are shown to use the guidelines in their sustainability reports, although their practices are diversified. There is also a fragmented use of the supplement, in which only a few GRI indicators are disclosed. The authors state that the annual report is only one of several media which the organizations use for sustainability disclosures.

Dumay, Guthrie, and Farneti (2010), in their article, provide a critique of the GRI Guidelines and examine their applicability to public and third sector organizations, in the period between 2001 and 2008. They conclude that the Guidelines promote a “managerialist” approach to sustainability (based on the assumption that there are no conflicts between the traditional economic criteria and those related to social and environmental aspects) rather than an approach based on ecological justice (focusing on establishing whether or not organizations act as socially and environmentally sustainable members of society) and that there is a lack of sustainability reports in the public and third sector, even though GRI is their primary reporting practice, as well as in the private sector. When analyzing whether the GRI guidelines are relevant to public and third sector organizations, based on the results of Dickinson’s (2005) and Tort’s (2010) studies, the authors observed that the GRI guidelines either did not appear to have influenced widespread public or third sector practice or were used to promote a managerial approach to elaborating SR, rather than achieving a form of ecosystem-based sustainability.

Observing that earlier studies were more concerned with what was reported and not the motivation for reporting, Farneti and Guthrie (2009) attempted to analyze the motives that led a group of Australian public sector agencies, considered to be followers of “better sustainability report practice”, to report on issues related to environmental and social aspects. Within this group, those who followed GRI Guidelines were invited to participate, resulting in the same sample as Guthrie and Farneti (2008). To reach their objective, they conducted semi-structured interviews with key preparers of the reports, concluding that they used the GRI Guidelines from the Sector Supplement for Public Agencies published in 2005. The report was prepared by a key individual in the organization using the most widely utilized media for disclosure. The main motivation for the disclosure of sustainability information was to provide information to stakeholders.

Lodhia, Jacobs, and Park (2012) evaluated environmental reporting practices within public sector entities. They observed the type and the extent of environmental disclosures in 19 Australian Commonwealth Departments, based on the legitimacy approach and on GRI. They found little evidence of widespread adoption of GRI Guidelines and argued that the influences of legislation and government regulation better explain the environmental reporting publications than legitimacy does. Even though the authors support the argument in favor of legitimacy, they make the point that the most significant initiatives in environmental reporting came from departments that could be seen as having potential legitimacy motivation and benefits, thus making it necessary to conduct more sophisticated research.

Adams, Muir, and Hoque (2014) analyzed the practice of measuring performance in the Australian public sector. This practice emphasized on measurement of sustainability performance and aimed to support improvements in organizational performance. The authors used a survey approach, mailing a questionnaire with a Likert scale from 1 (to little or no extent) to 5 (to a great extent) to 109 departments on the state/territory and federal tiers in August of 2005. 51 questionnaires were filled out of a total of 109. Statistical analysis (χ2, Kruskal-Wallis, and Mann-Whitney U test) was used to test for significant associations between profile characteristics and responses at a significance level of 5%. The most used performance measures were in the areas of production (quantity), cost efficiency, and quality, whereas those less utilized were learning and growth. Socio-environmental performance measures were the least used. Within this category, the most used were related to employee diversity and economic impact and the least used were problems related to ecological and social well-being.

Farneti and Siboni (2011) sought to analyze social reporting guidelines in local Italian governments. The sample was made up of 17 best practice reports, 11 being “annual,” referring to the year 2006 and, when it was not available, to the year 2005. Five reports were “five-year period” reports, referring to the 1999-2003 term, and one was a “ten-year” report, referring to the period comprising two terms, from 1995 to 2004. They first compared two Italian governmental guidelines for developing social reports in public sector organizations with Global Reporting Initiative (GRI) Guidelines to identify differences and similarities between them. Then they examined a group of social reports to explore the incidence, frequency, and quality of the information, in comparison with GRI Guidelines. In order to do this, they used content analysis, and to analyze the reports they used a coding instrument proposed by Guthrie and Farneti (2008), which was amplified to include the Italian governmental guidelines. Based on their findings, the authors were able to observe the following: only a few categories of the Italian governmental guidelines are similar to GRI Guidelines, most notably those which are related to general aspects; the disclosure of categories and elements in the social reports was fragmentary compared to the coding instrument; and Italian governmental guidelines are more largely related to labor.

Goswami and Lodhia (2014) carried out a case study to identify sustainability disclosure standards in four local councils in South Australia, in the absence of any mandatory sustainability reporting guidelines. To evaluate the extent of sustainability information disclosed, they used the 2005 GRI Sector Supplement for Public Agencies. Their results suggest that, even though they are not in use, elements of these guidelines are reported as sustainability issues in annual reports in a manner that enables state councils to consider financial sustainability more important than environmental and social sustainability.

Greiling, Traxler, and Stötzer (2015) investigated the extent to which public sector entities in Austria, Germany, and Switzerland applied sustainability reporting guidelines in accordance with the GRI and what types of data were reported. In order to do this, they conducted documentary analysis of external reports by public sector organizations included in the database of the GRI for the years 2012-2014. The article concluded that the entities analyzed were largely in compliance with the guidelines to a relatively great extent, but with considerable variations on social, environmental, and economic information.

Joseph (2013) investigated Malaysian local authorities’ understanding of sustainable development and sustainability reporting concepts by interviewing 23 people from 16 local councils. The results were analyzed by interpretive textual analysis, which identified that the concept of sustainable development was quite broad among respondents, being understood only by staff directly involved in the sustainable development activity. Most respondents agreed concerning the GRI definition of sustainable development.

Yadava and Sinha (2016) compared the sustainability reports of leading Indian public and private sector companies, based on the 2011 GRI Guidelines. Their analysis made use of 84 performance indicators from the 2011 GRI Guidelines. The performance indicators were divided into economic (9), environmental (30), and social (45) dimensions, and a numerical score from 0 to 3 was assigned to each. Analysis showed that reports in the economic dimension were much better than those in the social and environmental dimensions, there being no significant differences in their reporting practices on economic performance, whereas many differences were present in reporting practices on environmental and social dimensions. The authors considered the company Tata Steel an example to be followed.

Among the ten most cited articles an important number deal with aspects related to sustainability reports in only one country (Guthrie & Farneti, 2008; Farneti & Guthrie, 2009; Lodhia et al., 2012; Farneti & Siboni, 2011; Goswami & Lodhia, 2014; Yadava & Sinha, 2016); whereas only Greiling et al. (2015) refer to three countries.

Alcaraz-Quiles, Navarro-Galera, and Ortiz-Rodríguez (2014, 2017) analyzed sustainability disclosure practices in local government websites in Spain, establishing a comparative analysis for transparency. Domingues, Lozano, Ceulemans, and Ramos (2017) explored the relationship between reporting process and management of organizational changes for sustainability within public sector organizations that, by 2014, had published a sustainability report based on GRI Guidelines at least once; Farneti and Dumay (2014) critically analyzed changes to GRI G4, making recommendations on sustainability topics for public agencies and presenting a normative argument based on Gray’s (2006) ecological and eco-justice (EEJ) approach to produce public value in sustainability.

Other public organizations have also been studied. Cantele, Tsalis, and Nikolaou (2018) presented a new structure for evaluating the reporting disclosures of water utilities. Chamorro, Perea, and Balsells (2016) explored the extent to which public water supply and sanitation entities in Spain prepared their sustainability reports in accordance with the GRI, as well as their principle characteristics. Jiménez, Martínez, and López (2016) presented a proposal for producing a list of performance indicators adapted to the reality of Spanish universities based on GRI G4.

Therefore, according to the literature review, there was a significant lack of research regarding studies on the publication of public sector accountability reports at the international level, since most of the studies refer to a single country or specific type of organization, as previously mentioned by Papenfuß, Grüb and Frieländer (2015).

Methodology

The authors present studies on sustainability accounting and accountability as a research gap (Adams et al., 2014; Ball, Grubnic & Birchall, 2014, Gray et al., 2014). In this sense, this study aims to analyze the adherence and the standards of disclosure of GRI sustainability reports by public and state institutions from the public agency sector. The study can be described as documentary analysis, with a quantitative, descriptive approach.

The study initially searched in the Scopus database for publications on the use of public sector reports applying the GRI. We initially found 33 articles after using the terms “GRI” and “Public Sector” or “Global Reporting Initiative” and “Public Sector”. In the analysis of the entire period, it was observed that the first was from 2004. This study included 26 articles in total. Ten articles were excluded because, upon reading, it became clear that they did not deal directly with the use of GRI in the public sector. A description of the ten most cited articles were reported, in descending order.

As a sample, the analysis used Public Institutions and State-Owned Companies from the Public Agencies sector that had published sustainability reports in the Global Reporting Initiative (GRI) Database, whose data refer to the period between 1999 (the first year of disclosure) and the 4th July 2018. However, this survey covers a seven-year time lapse, focusing on the period between 2011 (the year in which GRI began to disclose reports by organization type) and 2017, since 2018 has yet to come to a conclusion. From the 177 public agencies included in the study, 138 were public institutions and 39 were state-owned companies, and had published 363 and 132 reports, respectively. Only 27 public institutions and 11 state-owned companies published more than five reports. Only the following seven agencies disclosed seven reports over the seven-year period: Empresa Municipal de Transportes (EMT), Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ), Hungarian Public Prosecutor’s Office, Société de transport de Montréal (STM), Trasporti Pubblici Parma (TEP), Belgische Technische Cooperatie (BTC), and Canada Post.

The data analyzed were obtained from the GRI Database, received upon request sent via email to ReportRegistration@GlobalReporting.org. The data allow users to filter and classify reports and organizations according to several criteria, revealing trends and standards in reporting practices, such as: Organization Type, Sector, Country/Territory, Region, Publication year, Integrated Report, Report type, Adherence level, GRI Service, Status, Stakeholder panel/Expert opinion, External assurance, Type of assurance provider/Assurance provider, Assurance scope, Level of assurance and Assurance Standard.

Inside the organization type, only public institutions and state-owned companies were considered. Public institutions are defined by the GRI (2013) as “an administrative unit of government, including the municipal authority of a city” and state-owned companies are defined as “a legal entity created by a government in order to undertake commercial activities on behalf of the owner government.” In both cases, analysis was limited to the public agency sector.

Integrated Reports are self-reported by the reporting organization. The label integrated means that the organization included basic non-financial, financial, and economic disclosures in a single report.

The Report Type field indicates the version of the GRI Guidelines applied in the report: GRI G1 (published in 2000), GRI G2 (published in 2002), GRI G3 (published in 2006), GRI G3.1 (published in 2011), GRI G4 (published in 2013 and valid until June 30, 2018), GRI Standards (published in 2016 and currently valid), Citing GRI (integrated sustainability reports that make explicit reference to being based on the GRI Guidelines but for which there is no GRI Content Index), and Non-GRI (when the integrated reports released by the organization disclose information on economic, environmental, social and/or governance performance, but there is no reference to being based on the GRI Guidelines or GRI Standards).

The Adherence Level reflects the extent to which the GRI Sustainability Reporting Framework and GRI Standards have been applied to a report. Reports are classified according to the GRI standard applied. GRI G1 and GRI G2 reports may be: In Accordance or Content Index Only. GRI G3 and GRI G3.1 may be A, B, or C and, in the event that an organization opts to have its report externally assured, a ‘+’ is added, resulting in A+, B+, or C+. GRI G4 reports may be classified as In Accordance – Core, In Accordance – Comprehensive, or Undeclared. GRI Standards may be In Accordance – Core, In Accordance – Comprehensive, or GRI-Referenced. When a report is considered “In Accordance,” this indicates that it is declared to be in conformity with the Guidelines, either Core or Comprehensive (required to present Disclosures G4-2, G4-35 to G4-55, and G4-57 to G4-58). “GRI-Referenced” (known as “Content Index Only” until 2017) indicates that a report uses individual GRI standards or parts of its content for sustainability reporting and may not to claim, in consequence, that the report was prepared in accordance with GRI Standards. Finally, Undeclared refers to the fact that there is no application level explicitly declared.

GRI Service indicates whether the report has gone through one of the following GRI Services: Materiality Disclosures Service, Content Index Service, SDG Mapping Service, GRI-Referenced Service, or Application Level Service.

Status applies specifically to GRI G3 (2006) and GRI G3.1 (2011) and refers to the status of the Application Level declaration for the GRI report. It may be Self-declared (the Application Level declaration was not confirmed by GRI or another third-party), GRI-checked (the report went through a GRI Application Level Check before December 2014), or Third-party-checked (the Application Level was confirmed by a third-party, separately from external assurance).

Stakeholder Panel/Expert Opinion indicates whether there was formalized input to or feedback on the report provided by a panel of stakeholders or expert(s). As of 2012, the GRI Database informs whether or not the report received external assurance, the type of assurance provider (accountant, engineering firm, small consultancy or boutique firm), and the name of the assurance provider. The Assurance Scope may refer to the Entire Sustainability Report, Specific sections, GHG (greenhouse gases) only, or not specified. The Level of Assurance may be limited/moderate, reasonable/high, combination (in different parts), or not specified.

The Assurance Standards indicate the application as disclosed in the external assurance statement. They may be AA1000AS, from Accountability; ISAE3000, from the International Standard on Assurance Engagements; Assurance Standard: national standard (general), with general accounting principles developed at the national level, for instance, or by an organization within the specific national context; or Assurance Standard: national standard (sustainability), which indicates the application of a sustainability (non-financial) specific national assurance.

There are some limitations related to the GRI Database. GRI created the GRI Standards Report Registration System and, as of March 1st 2018, reports must be submitted and verified by the reporting organizations through GRI. This enables them to notify GRI about the use of GRI Standards. Submitted reports are published in the List of GRI Standards Reports and in the GRI Sustainability Disclosure Database. Reports submitted prior to this period were added to the Database directly, having been temporarily removed and then returned to the Database upon reporter confirmation through the GRI Standards Report Registration System. Another issue is that, as a continuous database, analysis may end up including reports that refer to previous periods. The year considered is that of publication and not the year to which the report refers. Additionally, some documents may be omitted, such as those in non-Latin scripts or those not published online (GRI, 2018).

Results analysis

The following results are derived from analysis of sustainability reports published by organizations in the GRI Database. It was observed that, during the 2000-2015 period, there was a significant increase in the number of institutions that started to publish sustainability reports through the GRI. In 2017, there was a decline for all types of organizations. GRI (2018) stated that there are two reasons for this decline: first, as the register is an ongoing process, it is still collecting reports published in 2017, and, second, due to the implementation of the new standard registration system, the report must be approved by the reporter in order to appear in the GRI Database.

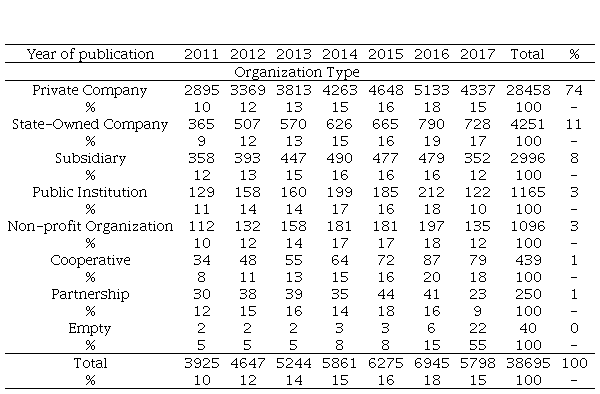

One may also observe that, in spite of the increase in the number of reports published by public and state institutions, the majority of reports (74%) are still published by private companies, in corroboration with previous authors’ findings (Ball, Grubnic & Birchall, 2014, Greiling et al., 2015, Guthrie & Abeysekera, 2006, KPMG International, 2013).

By corroborating with previous authors’ findings (Ball, Grubnic & Birchall, 2014, Greiling et al., 2015, Guthrie & Abeysekera, 2006, KPMG International, 2013), one may also observe that, in spite of the increase in the number of reports published by public and state institutions, the majority of reports (74%) are still published by private companies.

Public institutions and state-owned companies represent only 14% of the total, and, when public institutions are considered alone, they account for only 3% (see Table 1). Few entities omitted to publish the sector to which they belonged, as well as other data. These data are worrying, as sustainability commitments have a major impact on Public Sector Organizations, seeing that many are responsible for redefining policy and law objectives, with sustainability as a goal; they are also service providers, who play an important role in delivering sustainability policy results (Ball, Grubnic & Birchall, 2014).

Out of the 38,685 reports published, only 1,165 of them were published by public institutions in 53 countries. The United States of America (13%), Spain (11%), Australia (8%), Switzerland (6%), and Canada (5%) were the countries with the highest number of reports, accounting for almost 50% of all reports published. Brazil is in 10th place (3%) and Colombia in the 22nd (1%), due to ties between some countries.

State-owned companies from 79 countries published a total of 4,251 reports, with China (35%), Sweden (7%), the United Kingdom (7%), Finland (3%), and Australia (3%) standing out. Brazil and Colombia (2%) were in 10th place. We noted that there are differences in behavior among countries regarding reports from public institutions and state-owned companies.

Public institutions from 32 sectors published sustainability reports, most notably public agencies (31%), followed by universities, financial services, other sectors, and water utilities. These five sectors represent 72% of the total reports. While there has been an evolution over the years in the number of reports from state-owned companies (PA), the number of reports from public institutions (PA) has declined since 2015.

Five of the 36 sectors that published sustainability reports stood out among state-owned companies. They were, in descending order: financial services, other sectors, energy, energy utilities and logistics, accounting for nearly half of the reports. State public agencies occupied the twelfth position in this ranking.

Since the purpose of this study is to present the results of the public agency sector considering state-owned organizations and public companies, all references made to these organizations, henceforth concern only those in the public agencies sector. Europe (41%), North America (24%) and Asia (15%) were the regions with the highest number of sustainability reports published by public institutions. The most notable regions regarding state-owned companies were Europe (35%), Asia (29%), and Oceania (23%). These results demonstrate that Europe and Asia are the regions that stand out with disclosures on sustainability in the public agency sector, validating therefore the results of GRI's research (2010), which highlight an increase in publications in North America.

Excepting 2017, there is a greater adherence of public institutions over the years analyzed, showing a total of 363 reports published by 31 countries. The following countries stand out: United States (14%), Canada (10%), Republic of Korea (9%), and Australia and Spain (both with 8%). Brazil and Colombia (1%) share the 10th place with other countries.

State-owned companies’ sustainability reports have evolved, with the publication of 132 reports in 17 countries during the period analyzed. The countries with the highest number of disclosures were Australia (23%), the Republic of Korea (14%), the United Arab Emirates (11%), Portugal (6%), and Belgium. Brazil, Canada and Spain have the same number of published reports (5%). No reports were published in Colombia.

Although there has been an evolution in the number of sustainability reports published through GRI by public agencies, they still represent very little (1.28%) compared to the total reporting in the period from 2011 to 2017. Up to 2009, the public agencies represented 1.7% (GRI, 2010).

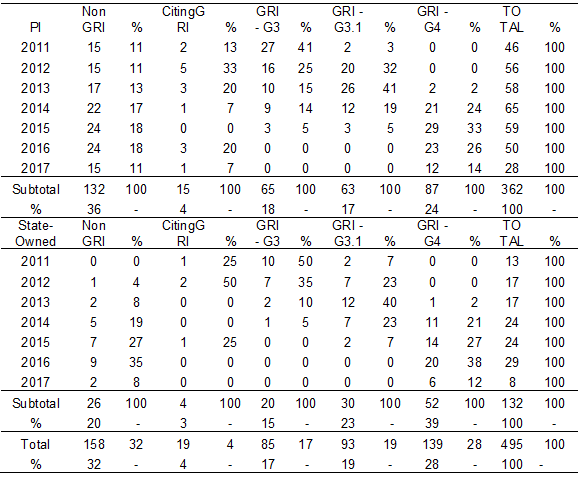

Although public organizations are expected to lead sustainability practices (Gray, Adams & Owen, 2014; Greiling & Grüb, 2014), they account for a very insignificant share (1%) of total reports published by companies in general. This result is corroborated by a 2010 GRI study (Reporting in Government Agencies) which showed that during the period 2001-2009 only 69 reports were published by 57 different public agencies, including state-owned companies. From 2011 to 2017, it was observed that 495 reports were disclosed by public and state-owned institutions, most of them (73%) by PI.

Regarding the adhesion of public agencies to integrated reports, 77% of public institutions and 76% of state companies self-declared that they did not adhere. In addition, as of 2015, GRI indicated whether a report is a “featured report” or not. None of these reports were considered featured reports.

The table 2 indicates the version of the GRI Guidelines applied to sustainability reports. Most of the reports published by PIs (59%) and state-owned companies (77%) were submitted under some type of GRI (GRI G3, GRI G3.1, or GRI G4). Only one report was submitted under GRI Standards, however, it only came into force in 2018.

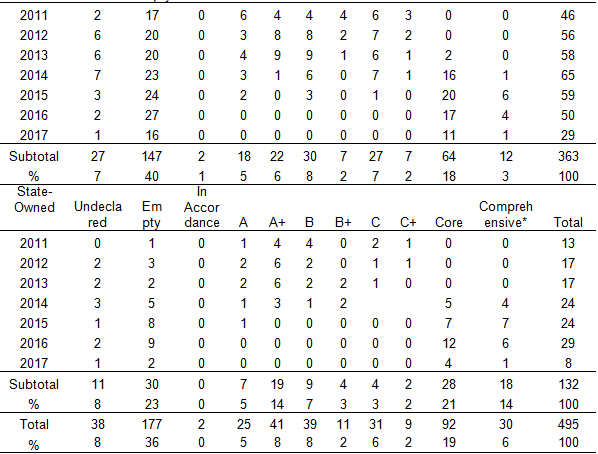

According to Table 3, most PIs (71%) did not declare or did not report the level of adherence of their reports to the GRI structure. Thirty percent reported that they applied the guidelines for GRI G3 or GRI G3.1 models and 21% for GRI G4 and GRI Standards, the latter having published only one report on the “in accordance” level, which was essential in 2017. It is possible to observe an effort to publish reports in compliance with GRI standards. However, the percentage of undeclared or unreported disclosures is still very high, decreasing to 31% among state-owned companies. Most of these (69%) met some GRI standard (GRI G3, GRI G3.1, and GRI G4). Costa and Crisóstomo (2017) point out that it is pertinent to propose that good adherence to quality standards, such as the GRI guidelines and the external audit of reports, strongly contribute to the quality and comprehensiveness of the information disclosed.

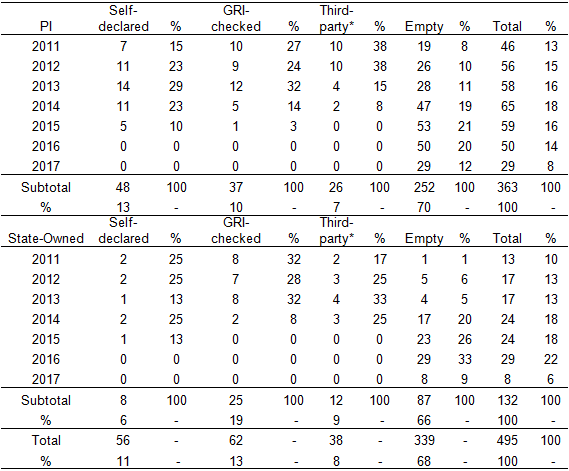

In reference to assurance aspects, it is possible to observe through the data analyzed whether Reports had engaged external assurance or not. It was observed that only 8% of the reports issued by public agencies were submitted to external verification, which represents a very small percentage. In addition, since 2015 there has been no submission of reports for external assurance. Most of them (68%) did not report this information, and this represents a very large gap in this analysis (see Table 4).

In addition to the previous information on assurance, as of 2012, it is possible to identify other aspects in the GRI Database. It can be inferred from the information provided regarding public institutions, that most of them (84%) did not use any external assurance service. In those cases where this service was provided, it was done through an accountancy firm, an engineering company, or a small consultancy or boutique firm. Most did not use formalized contributions or feedback on the report provided by a stakeholder panel or expert. Furthermore, a large number (84%) reported neither the scope nor the assurance level, in addition to declaring that no guarantee standard was used (AA1000 A + A35S, ISAE3000, National General and National Sustainability) in the external assurance statement.

According to the information provided in relation to public institutions, it was possible to identify that the majority (84%) did not use any external assurance service. In those cases where this service was provided, it was done through an accountancy firm, an engineering company, or a small consultancy or boutique firm. Most PI did not use formalized contributions or feedback on the report provided by a stakeholder panel or expert. Furthermore, a large number (84%) reported neither the scope nor the assurance level, in addition to declaring that no guarantee standard was used (AA1000 A + A35S, ISAE3000, National General and National Sustainability) in external assurance statement.

State-owned companies present a similar result to public institutions. Most of them did not engage any external assurance service (86%). The accountancy firm KPMG was selected by most of the companies who did engage the external assurance service, representing 10% of the total. Also, most of the companies did not use formalized contributions or feedback provided by an interested panel or expert (87%) on the report, did not report scope (72%), assurance level (72%) and stated that no standard was used (AA1000 A + A35S, ISAE3000, National General and National Sustainability) in achieving the external assurance statement.

As of 2013, reports indicate whether GRI materiality was verified. In 2014, only 17 reports submitted this information. As of 2015, this disclosure was related to the contracting of other services with the GRI, with a total of 46 requests for services from 45 entities: Content Indexing Service (28), Materiality Disclosure Service (14), Application Level Service (3), SDG Mapping Service (1) and GRI-Referenced Service (0).

Since 2009, it is also possible to identify the use of Sector Supplements in reporting. Only four reports from public institutions have reported that they have used the Supplement for Public Agencies in a complementary way. Since 2015, none of the organizations analyzed have used it. These results show that use of the supplement has worsened. From 2005 to 2009, 21 reports were published by 12 different public agencies (GRI, 2010). Some factors contribute to the non-use of the supplement, such as its generic nature, private sector triple-bottom-line approach, lack of applicability across the range of public agencies (Guthrie & Farneti, 2008), and the tendency to elaborate narrative/descriptive reports on policies rather than disseminating quantified data over time (GRI, 2010).

Conclusion

This work sought to analyze the GRI adherence and disclosure standards of sustainability reports of public and state institutions in the public agency sector.

An evolution was observed in the disclosure of sustainability reports in the GRI Database over the years, except for 2017, when there was a decline in all items analyzed, which was justified by GRI. However, despite this evolution, also perceived among public and state institutions, it was possible to identify that there are still very few sustainability reports in this area, given that they represent only 1.8% of the total.

The public agency sector is the one that most publicizes in organizations that are public institutions, however, in the state-owned, it occupies only the 12th place. Europe was observed to be the region with the highest number of public (PI and state-owned) agencies with GRI sustainability disclosures. The countries with the highest number of disclosures are the United States of America, with respect to public institutions, and Australia, with respect to state-owned companies.

Crisóstomo, Forte, and Prudêncio (2017) consider that the quality of reports depends on the issuing of integrated reports, the adherence to the GRI guidelines, the level of application of the report, and the external audit carried out in the sustainability reports. In this sense, if the quality and reliability of the reports are related to the characteristics listed above, one may argue that public and state institutions have disclosed their reports with low quality and reliability.

Although most published PI and state reports have adhered to some type of GRI (GRI G3, GRI G3.1, GRI G4, or GRI Standards) and there has been an effort to disclose reports with application levels in compliance with the type of GRI declared, especially those on the Accord - Essential level, there were a significant number of reports without this information, mainly of the PI (PA). Additionally, most of the reports were not integrated reports, received no external assurance, and had no formalized input or feedback on the report provided by a panel of stakeholders or expert(s). Furthermore, there was no use of any assurance standard (AA1000 A + A35S, ISAE3000, National General and National Sustainability) in achieving the external assurance statement.

Considering these findings, the publication of reports by the public agencies analyzed may increase. However, this increase is still very insignificant. Furthermore, the low quality of published reports, confirms Adams, Muir, and Hoque’s (2014) claim that the comprehensive implementation of public sector sustainability reporting will only be possible if it is mandatory and if there are competitive advantages to adopting these measures.

Taking this into account, this study aimed to contribute to a better comprehension of the scenario of research on accountability related to public sector sustainability, going further previous studies by analyzing the report publication though the GRI database and observing all data inside it, in all countries. The lack of research in this area mentioned by previously cited authors was verified herein as well. These findings also provide a better understanding to public agencies for the publication of their reports, aiming to enabling them to improve their quality.

The limitation to this study is the fact that it uses data provided by the organizations in question to the GRI database. It is recommended to conduct future empirical research directly on organizations' reports to conduct qualitative analysis of the data in the reports, including other databanks or report models, so that these analyses may contribute to other accountability instruments for public sector sustainability.

References

Adams, C., Muir, S. & Hoque, Z. (2014). ‘Measurement of Sustainability Performance in the Public Sector’, Sustainability Accounting. Management and Policy Journal, 5(1), 46-67. DOI: https://doi.org/10.1108/SAMPJ-04-2012-0018 .

Alcaraz-Quiles, F., Navarro-Galera, A. & Ortiz-Rodríguez, D. (2014). Comparative analysis of transparency in sustainability reporting by local and regional governments. Lex Localis, 12(1), 55-78. DOI: https://doi.org/10.4335/12.1.55-78(2014)

Alcaraz-Quiles, F., Navarro-Galera, A. & Ortiz-Rodríguez, D. (2017). Transparency about sustainability in regional governments: The case of Spain [Article@La transparencia sobre sostenibilidad en gobiernos regionales: El caso de España]. Convergencia-Revista de Ciencias Sociales, 24(73), 113-140.

Altenburger, O. & Schaffhauser-Linzatti, M. (2014). Integrated reporting for universities? Austrian public universities as an example. In Knowledge and Management Models for Sustainable Growth, e-book of Proceedings of IFKAD (pp. 2705-2712).

Ball, A., Broadbent, J. & Jarvis, T. (2006). Waste management, the challenges of the PFI and sustainability reporting. Business Strategy and the Environment, 15(4), 258-274.DOI: https://doi.org/10.1002/bse.532.

Ball, A., Grubnic, S. & Birchall, J. (2014). Sustainability Accounting and Accountability in the Public Sector. In J. Unerman et al. (eds.) Sustainability Accounting and Accountability. Oxon & New York: Routledge.

Borglund, T., Frostenson, M. & Windell, K. (2010). Increasing responsibility through transparency. A study of the consequences of new guidelines for sustainability reporting by Swedish state-owned companies. Stockholm.

Broadbent, J. & Guthrie, J. (2008). Public sector to public services: 20 years of “contextual” accounting research. Accounting, Auditing & Accountability Journal, 21(2), 129-169. DOI: https://doi.org/10.1108/09513570810854383 .

Brown, H., de Jong, M. & Levy, D. (2009). Building institutions based on information disclosure: Lessons from GRI’s sustainability reporting. Journal of Cleaner Production, 17(6), 571-580. https://doi.org/10.1016/j.jclepro.2008.12.009.

Brundtland, G. (1991). Nosso Futuro Comum/Comissão Mundial Sobre Meio Ambiente e Desenvolvimento, 2 ed., Rio de Janeiro: FGV.

Cantele, S., Tsalis, T. & Nikolaou, I. (2018). A new framework for assessing the sustainability reporting disclosure of water utilities. Sustainability (Switzerland), 10(2). DOI: https://doi.org/10.3390/su10020433.

Ciegis, R. & Zeleniute, R. (2008). Ekonomikos plėtra darnaus vystymosi aspektu. Taikomoji ekonomika: sisteminiai tyrimai, t. 2, (1), 37-54.

Ciegis, R., Ramanauskiene, J. & Martinkus, B. (2009). The concept of sustainable development and its use for sustainability scenarios. Engineering Economics, 62(2).

Costa, B. & Lima Crisóstomo, V. (2017). Comprehensiveness of Corporate Social Responsibility Reports of Brazilian Companies: An analysis of its evolution and determinants. Cuadernos de Contabilidad, 18(45), 125-151. http://dx.doi.org/10.11144/javeriana.cc18-45.ccsr.

Crisóstomo, V., Forte, H. & Prudência, P. (2017). Uma análise da adesão de instituições brasileiras à gri como método de divulgação de informações de responsabilidade social. V Conferência Sulamericana de Contabilidade Ambiental Valores Humanos e Consumo Sustentável. Brasília, DF.

Cruz, C., Marques, A. & Ferreira, A. (2009). Informações ambientais na contabilidade pública: reconhecimento de sua importância para a sustentabilidade. Sociedade, contabilidade e gestão, 4(2).

Domingues, A., Lozano, R., Ceulemans, K. & Ramos, T. (2017). Sustainability reporting in public sector organisations: Exploring the relation between the reporting process and organisational change management for sustainability. Journal of environmental management, 192, 292-301. DOI: https://doi.org/10.1016/j.jenvman.2017.01.074.

Dumay, J., Bernardi, C., Guthrie, J. & Demartini, P. (2016). Integrated reporting: A structured literature review. Accounting Forum, 40(3), 166-185. https://doi.org/10.1016/j.accfor.2016.06.001.

Dumay, J., Guthrie, J. & Farneti, F. (2010). GRI sustainability reporting guidelines for public and third sector organizations: A critical review. Public Management Review, 12(4), 531-548. DOI: https://doi.org/10.1080/14719037.2010.496266.

Farneti, F. & Dumay, J. (2014). Sustainable public value inscriptions: A critical approach. Studies in Public and Non-Profit Governance, 3, 375-389. DOI: https://doi.org/10.1108/S2051-663020140000003016.

Farneti, F. & Guthrie, J. (2009, junho). Relatórios de sustentabilidade das organizações do setor público australiano: por que eles relatam. Contabilidade fórum, 33(2), 89-98. DOI: https://doi.org/10.1016/j.accfor.2009.04.002

Farneti, F. & Siboni, B. (2011). An analysis of the Italian governmental guidelines and of the local governments' practices for social reports. Sustainability Accounting. Management and Policy Journal, 2(1), 101-125. DOI: https://doi.org/10.1108/20408021111162146.

Flower, J. (2015). The International Integrated Reporting Council: A story of failure. Critical Perspectives on Accounting, 27, 1-17. https://doi.org/10.1016/j.cpa.2014.07.002.

Global Reporting Initiative (GRI). (2005) Sector Supplement for Public Sector Agencies: Pilot Version 1.0, Amsterdam: Global Reporting Initiative.

Global Reporting Initiative (GRI). (2012). Pontos de Partida Relatórios de Sustentabilidade da GRI: Quanto vale essa jornada? Amsterdam: Global Reporting Initiative.

Global Reporting Initiative (GRI). (2013). Sustainability Reporting Guidelines. Data Legend. Amsterdam: Global Reporting Initiative.

Global Reporting Initiative (GRI). (2018). Sustainability Disclosure Database. Data Legend. Amsterdam: Global Reporting Initiative.

Global Reporting Initiative GRI. (2010). Reporting in Government Agencies. Amsterdam: Global Reporting Initiative.

Goswami, K. & Lodhia, S. (2014). Sustainability disclosure patterns of South Australian local councils: A case study. Public Money & Management, 34(4), 273-280. DOI: https://doi.org/10.1080/09540962.2014.920200.

Gray, R., Adams, C. & Owen, D. (2014). Accountability, Social Responsibility and Sustainability: Accounting for society and the environment. United Kingdom: Pearson.

Greiling, D. & Grüb, B. (2014), Sustainability reporting in Austrian and German local public enterprises. Journal of Economic Policy Reform, 17(3), 209-223. https://doi.org/10.1080/17487870.2014.909315.

Greiling, D., Traxler, A. & Stötzer, S. (2015). Sustainability reporting in the Austrian, German and Swiss public sector. International Journal of Public Sector Management, 28(4/5), 404-428. DOI: https://doi.org/10.1108/IJPSM-04-2015-0064.

Guthrie, J. & Abeysekera, I. (2006) Content Analysis of Social, Environmental Reporting: What Is New? Journal of Human Resource Costing & Accounting, 10(2), 114-126. https://doi.org/10.1108/14013380610703120.

Guthrie, J. & Farneti, F. (2008). GRI sustainability reporting by Australian public sector organizations. Public Money and management, 28(6), 361-366. DOI: https://doi.org/10.1111/j.1467-9302.2008.00670.x.

Hopwood, A., Unerman, J. & Fries, J. (2010). Accounting for Sustainability: Practical Insights. London: Earthscan.

Jacobs, M. (1995). Sustainable development–from broad rhetoric to local reality. In Conference Proceedings from Agenda, Vol. 21.

Jornal Oficial da União Europeia. (2014). Diretiva 2014/95/UE do Parlamento Europeu e do Conselho de 22 de Outubro de 2014. https://eur-lex.europa.eu/legal-content/PT/TXT/PDF/?uri=CELEX:32014L0095&from=EN.

KPMG Global Sustainability Services. (2008). Pesquisa internacional de responsabilidade corporativa relatando 2008. Amstelveen.

KPMG International. (2013). The KPMG survey of corporate responsibility reporting 2013. https://assets.kpmg.com/content/dam/kpmg/pdf/2015/08/kpmg-survey-of-corporate-responsibility-reporting-2013.pdf.

Lodhia, S., Jacobs, K. & Park, Y. (2012). Driving public sector environmental reporting: The disclosure practices of Australian commonwealth departments. Public Management Review, 14(5), 631-647. DOI: https://doi.org/10.1080/14719037.2011.642565.

Macintosh, A. & Wilkinson, D. (2012). Are we progressing? Comprehensive monitoring and reporting in Australia. The Australian Collaboration.

Nascimento, E. & Costa, H. (2010). Sustainability as a new political Field. Cahiers do IIRPC, 51-8 (especial).

Papenfuß, U., Grüb, B. & Frieländer, B. (2015). Nachhaltigkeitsberichterstattung öffentlicher Unternehmen – Entwicklung eines Qualitätsmodells und empirische Befunde für Stadtwerke im internationalen Vergleich. Journal for Public and Nonprofit Services, 38(S45), 170-187.

Riedner, L., Ribeiro, I., Brandalise, L. & Bertolini, G. (2018). Dimensão social da sustentabilidade: Uma análise a partir de propriedades produtoras de mandioca. Revista Brasileira de Gestão e Desenvolvimento Regional, 14(3), 396-425.

Rolland, D. & O'Keefe Bazzoni, J. (2009). Greening corporate identity: CSR online corporate identity reporting. Corporate Communications: An International Journal, 14(3), 249-263. https://doi.org/10.1108/13563280910980041.

Tort, L. (2010). GRI Reporting in Government Agencies. Amsterdam: Global Reporting Initiative (GRI).

Unerman, J., Guthrie, J. & Striukova, L. (2007) UK Reporting of Intellectual Capital, University of London: ICAEW.

Wackermann, G. (2008). Le développment durable. Paris: elipses.

Yadava, R. & Sinha, B. (2016). Scoring sustainability reports using GRI 2011 guidelines for assessing environmental, economic, and social dimensions of leading public and private indian companies. Journal of Business Ethics, 138(3), 549-558. DOI: https://doi.org/10.1007/s10551-015-2597-1.

Notes:

*

Scientific and technological research article.

Author notes:

a

Corresponding

author. E-mail address: elyrouse@gmail.com

Additional information:

How to cite: Bellini,

E. C. de O., Rodrigues, R. N., Lagioia,

U. C. T., & Lima De Freitas, M. A. (2019). Public Sector (Un)Sustainability: a study of GRI adherence and

sustainability reporting disclosure standards in Public Institutions and

State-Owned Companies of the Public Agency Sector. Cuadernos de Contabilidad, 20(49). DOI: https://doi.org/10.11144/Javeriana.cc20-49.psss