APA

ISO 690-2

Harvard

Haga clic en un formato de citación

Tax Aggressiveness, Market and Idiosyncratic Risks in Brazil*

Agresividad fiscal, riesgos de mercado e idiosincrásicos en Brasil

Agressividade tributária, riscos de mercado e idiossincráticos no Brasil

Cuadernos de Contabilidad, vol. 21, 2020

Pontificia Universidad Javeriana

Antonio Lopo Martinez a antoniolopomartinez@gmail.com

University of Sao Paulo, Brasil

Welliton Botão Martins

Fucape Business School, Brasil

Received: 28 June 2019

Accepted: 31 May 2020

Published: 17 October 2020

Abstract:

This study aims to analyze the relationship between tax aggressiveness and the risks associated with the variation of returns in Brazilian companies’ stock. Particularly, the research regards the systematic and idiosyncratic risks. The sample was formed by companies that composed the IBOVESPA index in the period between 2011 to 2016. The measurements of tax aggressiveness were the effective tax rate and the temporary book-tax differences. The results showed a significant relationship between tax aggressiveness and risk, concluding that the higher the tax aggressiveness, the lower the beta, and the higher the idiosyncratic risk. This study is essential because it maps the effect of tax aggressiveness on the financial risks related to Brazilian companies’ shares, as well as being useful to investors, portfolio, and business managers. JEL Code: K34, M40.

Keywords:Tax aggressiveness, market risk, idiosyncratic risk, effective tax rate.

Resumen:

Este estudio tiene como objetivo analizar la relación entre la agresividad fiscal y los riesgos asociados con la variación de los rendimientos en las acciones de las empresas brasileñas. Particularmente, la investigación se centra en los riesgos sistemáticos e idiosincrásicos. La muestra la integran las empresas que compusieron el índice IBOVESPA en el período comprendido entre 2011 y 2016. Las mediciones de la agresividad fiscal fueron la Tasa de Impuesto efectiva y las diferencias temporales entre el beneficio contable sobre el tributario. Los resultados mostraron una relación significativa entre la agresividad fiscal y el riesgo, concluyendo que cuanto mayor sea la agresividad fiscal, menor será la beta y mayor será el riesgo idiosincrásico. Este estudio es esencial porque mapea el efecto de la agresividad fiscal en los riesgos financieros relacionados con las acciones de las empresas brasileñas, además de ser útil para los inversionistas, la cartera y los gerentes de negocios. Códigos JEL: K34, M40.

Palabras clave: Agresividad fiscal, riesgo de mercado, riesgo idiosincrásico, tasa de impuesto efectiva.

Resumo:

Este estudo tem como objetivo analisar a relação entre a agressividade tributária e os riscos associados à variação de retornos nas ações das empresas brasileiras. Particularmente, a pesquisa se centra nos riscos sistemáticos e idiossincráticos. A amostra foi formada por empresas que compuseram o índice IBOVESPA no período entre 2011 e 2016. As medidas de agressividade fiscal foram a alíquota efetiva de tributação e as diferenças fiscais temporárias entre o lucro contábil e tributário. Os resultados mostraram uma relação significativa entre agressividade e risco fiscal, concluindo que quanto maior a agressividade tributária, menor a beta e maior o risco idiossincrático. Este estudo é essencial porque mapeia o efeito da agressividade tributária sobre os riscos financeiros relacionados às ações das empresas brasileiras, além de ser útil para investidores, carteira e gerentes de negócios. Códigos JEL: K34, M40.

Palavras-chave: Agressividade tributária, risco de mercado, risco idiossincrático, taxa efetiva de imposto.

Introduction

Brazil has a complex tax system, and its different users have a hard time understanding its particularities. This complexity is a result of the system laws, either because they allow stretching interpretations and because of their loopholes. Currently, the national tax legislation has approximately sixty current taxes, governed by laws, decrees, and other norms that are repeatedly changed, giving rise to different interpretations (Pilati & Theiss, 2016).

For Rezende & Nakao (2012), the difficulty in understanding, due to the legislation or differences in the interpretation of rules, has caused conflicts in accounting choices adopted by tax legislators and accounting standards, taking into consideration the different economic interests. Thus, it is reasonable to assume that a manager has the responsibility of making choices regarding the adoption of an understanding to disclose a better economic performance. That results in significant impacts on the accounting reports, regarding both disclosure and appropriation of tax expenditures.

Therefore, managers conduct taxes to maximize investor gains, control risks with tax inspections, set standards of their remuneration, and respond to market expectations since tax expenses directly influence asset prices (Guimaraes et al., 2016).

According to Martinez & Silva (2017), tax aggressive companies are those that adopt adequate tax planning mechanisms to reduce expenses with tax charges.

Tax management is the set of intentional actions or negligent conducts performed by managers, adopted before or after an event to reduce, mitigate, transfer, or delay (following the law) tax charges (Machado & Nakao, 2012).

For Vello & Martinez (2014), organizations that are inefficient in tax planning have a higher tax burden than the competition in the sector. That undermines their competitive potential and increases their risk level in comparison to other companies. The authors suggest the existence of a significant and opposing relationship between systematic risk and the degree of efficient tax planning in organizations that adopt best practices in governance.

The results presented by a company influence investors’ risk perception. Also, the disclosure of the firm’s relevant information, such as risk level, profits, and future cash flows, may have an immediate impact on negotiated stocks, adjusting its risk index (Amorim, Lima, & Pimenta Junior, 2014).

In their study to conceptualize the risk to which firms are exposed, Silva, Fávero, & Almeida (2016) argue that the volatility of the returns on an asset’s shares represents the total risk of that organization. The risk can be separated into two components: idiosyncratic or unsystematic risk, and market or systematic risk.

Thus, we elaborated the following research problem: Do national companies with higher levels of tax aggressiveness, present higher market and idiosyncratic risks? This work aims to answer to this question, studying a sample formed by publicly traded Brazilian companies participating in the BOVESPA index, which traded shares in the B3 stock exchange, in the period between 2011 and 2016.

The results of this kind of study can collaborate with those agents who relate accounting information to business risk, stimulating research on the subject. In addition, this study adopts the following assumptions:

(a) The level of the tax burden requires examinations of the relationship between the tax system and corporations;

(b) It is not clear to what extent users of the information a firm discloses can perceive its tax aggressiveness. If the users can perceive it well, this may affect the idiosyncratic risk;

(c) Studies carried out in Brazil connecting tax aggressiveness and risks, in the components idiosyncratic and market risks, are not conclusive.

The findings of this research can also be useful for agencies regulating accounting, since they may help in the elaboration of accounting standards (Amorim, Lima, & Murcia, 2012).

The next section of this article presents a theoretical framework on the concepts and previous works addressing tax aggressiveness, risks, and the relationship between the two. Afterward, the third section shows the methodology applied in this research, including the sample selection procedures, the definition of variables, and the measurements used, as well as presenting the mathematical models adopted in the regression. The fourth section presents the results obtained from the Pearson correlation and panel regression. Finally, the fifth section is dedicated to the discussion of the results and concludes with the final considerations.

Theoretical frameworks

Tax Aggressiveness

Common law countries highly value the economic essence of the legal form, which results in a more significant difference between the amounts registered as accounting profit and the amounts considered as taxable income. In this context, the accounting system is based on principles. On the other hand, in code law countries where there is more conformity between accounting and tax systems, the form prevails over the essence. In these countries, it is possible to observe a stronger connection between accounting standards and tax regulations (Fonseca & Costa, 2017).

In the specific case of Brazil, accounting standards have a historically strong link with tax regulations. It is expected that, with the convergence to the International Financial Reporting Standards –IFRS–, this connection weakens and, existing accounting alternatives that allow for reliable representation, with the predominance of essence over form. That will cause more significant oscillation in the differences between accounting and taxable profits (Cardoso, Costa, & Avila, 2017).

According to Martinez & Silva (2017), tax aggressiveness is the set of administrative procedures adopted before the event that generates the taxation to reduce the total tax expenses. Therefore, the tax aggressiveness aims to reduce, through efficient tax planning, the income or taxable amounts. Tax reduction measures affect all corporate activities with the potential to impact fiscal responsibility. It can cover operational activities, discretionary managerial actions, and tax advantages (Ramos & Martinez, 2018).

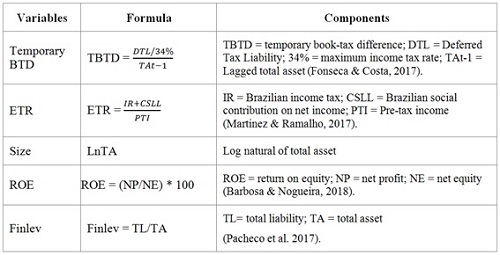

One of the most used measurements of tax aggressiveness pointed out in the current literature is the Effective Tax Rate –ETR–, obtained from the quotient between tax expenses and pre-tax income. Observing this measurement, the comparison between two companies with the same pre-tax income but different amounts of tax expenses indicate that the company with the lowest tax burden is the one with better tax planning. Another important measurement of a firm’s tax aggressiveness is the Book-Tax Difference –BTD–. This measurement is observed in the hypothesis of nonconformity between accounting profit and taxable income. This hypothesis is based on the management of accounting results for more and tax results for less (Rodrigues & Martinez, 2018).

The ETR establishes a relationship between the taxes paid and the firm’s current profit. This measurement indicates that the lower the tax burden in a company, the greater its tax aggressiveness. As for BTD, which shows the difference between the accounting profit and the taxable income, the higher the firm’s BTD, the greater its tax aggressiveness (Araújo et al., 2018).

Marques, Costa, & Silva (2016) draw attention to environments with different levels of conformity between the accounting and fiscal systems. In countries with lower levels of linkage between accounting and tax regulations, accounting information becomes more relevant to the various economic agents. In scenarios where systems are aligned, investors give more value to the tax information in detriment to the accounting figures disclosed.

When BTD is essentially based on the level of compliance between accounting standards and tax regulations, it is classified as non-discretionary differences or normal BTD. A discretionary difference or abnormal BTD is observed when there is interference from the manager, adopting alternative criteria, in light of accounting standards and tax regulations. In this case, the origin of this controversy is accounting and tax management (Mello & Salotti, 2013).

BTD is classified as permanent and temporary. Permanent BTDs –PBTD– are identified when revenue or expense is recognized by the accounting system but has no effect on the tax system. Temporary BTDs –TBTD–, however, are identified when both systems recognize revenues and expenditures equally but differ in which moment revenues and expenditures are realized. That influences the register of these accounts in the future (Fonseca & Costa, 2017).

The classification of BTD as permanent or temporary affects the predictability of future results. TBTDs carry information about the persistence of profits and the management of results. PBTDs, however, can capture financial and tax aggressiveness, higher accounting profit, and lower taxable income. Thus, the BTD classification affects the level of uncertainty of economic agents about a firm’s future returns in a different way (Marques, Costa, & Silva, 2016).

In this sense, when companies have high levels of BTD, their results are less persistent. This fact explains why BTDs are associated with the level of investors’ uncertainty regarding a company’s results (Marques, Costa, & Silva, 2016). Mello & Salotti (2013) confirm that high BTD reduces investor’s expectations since it indicates more discretionary increases and less persistence of gains. This is due to the possibility of these increases being reversed in the future.

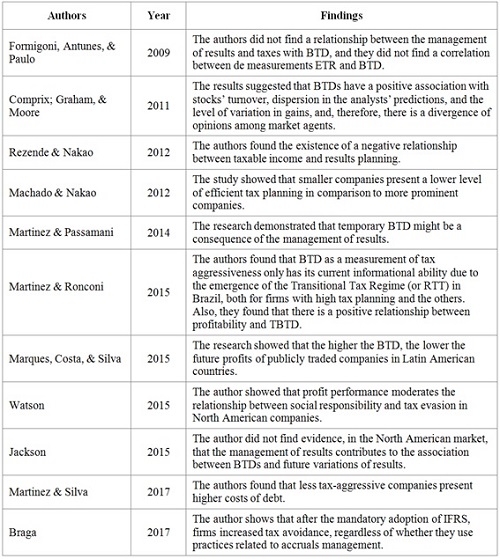

Table 1 shows a chronology of the Brazilian and international research on tax aggressiveness and its measurements.

Systematic and idiosyncratic risks

The risk factor is a component usually present in any business, potentialized in times of market turbulence, and requires companies to pay more attention to their management. In addition, the opening of capital and the expansion of markets and business environment lead management to a growing concern about the potential investors’ perception of risk (Costa, Leal, & Ponte, 2017).

Accounting reports are tools that can provide access to risk parameters, influencing investors’ decision-making. In this sense, accounting science can be understood as an essential source of information for shareholders to determine the price of a stock and its market risk (Amorin, Lima, & Murcia, 2012).

Risk is the probability that an expected event does not occur. As a result, investors charge a percentage to join a venture. This demanded rate of return will be higher as the risk involved in the business increases (Amorim, Lima, & Pimenta Junior, 2014).

Tax aggressive firms increase their risk level in the capital market, raising doubts about their ability to effectively plan their tax burden (which generates uncertainties about their future results). Previous studies have found variations in BTD levels with increased credit risk (Vello & Martinez, 2014).

It is possible to classify risk in two types. It is systematic if it affects companies in general, and there is no possibility of the risk elimination through diversification. It is non-systematic when it is specific to a single company or a single group of companies. In this case, by applying diversification, the investor manages the risk by lowering or eliminating the risk level (Souza, Massardi, & Pires, 2017).

Adopting the same trend of thought, Amorim, Lima, & Murcia (2012) point out that the total risk can be understood as the sum between systematic risk (non-diversifiable) and company risk (diversifiable). The authors also consider the possibility of investors operating in the stock market to diversify their portfolio of investments. In other words, when eliminating the effect of diversifiable risk, the core concern regarding organizational risk is the systematic risk, since it becomes the only component of total risk.

Marinho et al. (2013) argue that rational investors objectively analyze available information. These good or bad decisions made about the future are random, and do not result from tendencies that are characteristics of human feelings. They also argue that, in the process of deciding about investments, shareholders assess at least one indicator and consider profit and market specific risk (β𝑀), as determining factors for the quantification of risk in a portfolio. Thus, systematic risk can be understood as a measure of the sensitivity of an individual asset (or an investment portfolio), regarding the market variations. Beta is related to the totality of the systematic risk to which the assets are subject. It is, therefore, not diversifiable, independent of the investment being in only one asset or portfolio (Amorim, Lima, & Pimenta Junior, 2014).

As for Marinho et al. (2013), there is evidence suggesting that increasing one unit in the beta index results in a fivefold increase in the risk perceived by the investor. The authors, therefore, assume the beta index as the primary variable to measure the level of risk in which an asset portfolio is subject to when deciding to invest. Amorim, Lima, & Pimenta Júnior (2014) found a positive relationship between beta and financial and profitability indicators, as well as between beta and companies with higher profits. They also found an inverse relationship between market risk and the following business indicators: percentage of return of organizations with higher profits; market-to-book volatility; largest total assets; higher volumes of debt and degree of financial leverage –DFL–; liquidity and working capital.

The idiosyncratic risk, in turn, is the firm’s specific risk and, according to Harry Markowitz’s Portfolio Theory, investors with balanced market portfolios would theoretically eliminate it. However, not all investors diversify their investments, which results in some degree of this type of risk, or the specific risk in its entirety. These investors demand additional returns to compensate for the higher risk in their portfolios or investments (Mendonça et al., 2012). Companies with lower risk levels benefit from better pricing of their shares, providing a favorable environment for new capital openings and new share issuance. Thus, the stock market is strengthened, creating more economically attractive alternatives to fund companies (Besarria & Silva, 2017).

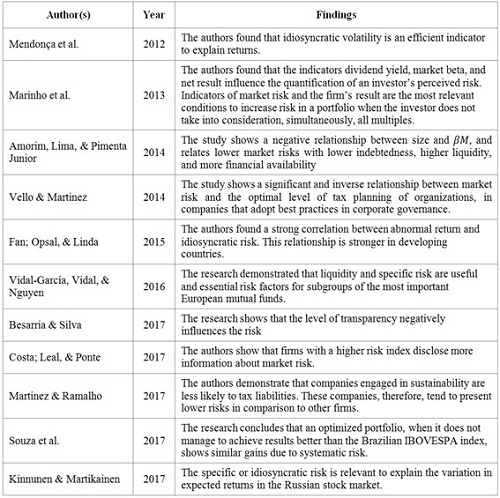

Table 2 shows a chronology of the recent research, both Brazilian and international, about market and idiosyncratic risks.

Hypothesis on the relationship between tax aggressiveness and risks

As mentioned before, Vello & Martinez (2014) stress the importance of tax planning to increase competitiveness. They suggest that companies that adopt best practices in corporate governance show a significant and opposing relationship between systematic risk and the degree of efficient tax planning.

Companies encourage their managers to use risky strategies, seeking to maximize their returns, and accepting a higher level of risk. There is a direct relationship between CEO incentives and tax aggressiveness (Guenther, Matsunaga, & Williams, 2017).

Also, as mentioned in the introduction of this article, tax aggressive companies increase their risk level in the capital market, putting in check their ability to conduct effective tax planning and generating uncertainties about their future results. Studies observed variations in BTD levels with increased credit risk (Vello & Martinez, 2014).

Guenther, Matsunaga, & Williams (2017) argue that corporate operations that seek to minimize the payment of tax expenditures increase organizational risk since future uncertainties about tax expenditures accompany tax aggressiveness. However, the same authors did not find a significant relationship between the aggressiveness and the total risk of the company.

In this study, we want to test the relationship between tax aggressiveness with idiosyncratic risks and systematic risks. Based on the international literature, the existence of a significative statistical relationship is inferred. It is believed that the greater the tax aggressiveness, the higher the idiosyncratic risk of the returns. Thus, a positive relationship is expected at this point. In turn, concerning the systematic risk, the relationship can be direct (like the one that is anticipated to idiosyncratic risk), or even inverse (which is fundamentally dependent on the sensitivity of the return of a company the oscillations of the Brazilian market). Depending on how the market sees tax risks it will define the beta of a company in a future period.

Methodology

The sample was obtained from Economática® database and the CVM’s platform. It is composed of Brazilian publicly traded companies listed in the B3 stock exchange and included in the BOVESPA index for the period from 2011 to 2017. After data treatment, institutions with differential tax treatment, such as financial institutions and insurance companies, were excluded from the sample. Companies with negative ETRs were also excluded, allowing for a better understanding of the obtained results.

The independent variables of the study are temporary BTD and ETR. Two proxies were used to test a possible convergence between the measurements, increasing the reliability of the results. The TBTD variable was based on Fonseca & Costa (2017) who associate TBTD with the reduction of tax payments, allowing a better association with tax aggressiveness. As for the dependent variables, the study considered two. The first analysis refers to the variable that represents a market or systemic risk and the second analysis observes the company’s idiosyncratic or specific risk.

Besarria & Silva (2017) argue that portfolios with companies showing a higher level of governance present a lower risk compared to other companies. Fonseca & Costa (2017) defend an inverse relationship between BTD, firm size, and financial leverage. Amorim, Lima, and Pimenta Junior (2014) suggest that the larger the asset, the lower the risk. Consul & Saito (2014) found in their studies a direct relationship between performance and return on equity, suggesting the use of this indicator as a criterion for investors to select assets.

Based on the literature, therefore, the following indicators were used as control variables: the market segment of B3 Brazilian stock exchange called ‘Novo Mercado’ (new market); firm’s size, ROE, and financial leverage, the size was expressed in the log natural of total asset.

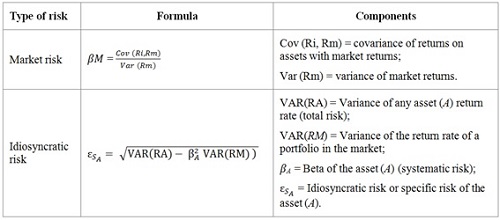

In order to determine the market beta (𝛽𝑀), we used the covariance between the results achieved by an asset and the returns from the market itself, divided by the variance of the market returns (Silva, Fávero, & Almeida, 2016).

[Equation 1]

[Equation 1]Where:

Covar = covariance function

SD = standard deviation function

For the idiosyncratic risk, we used the model based on the Capital Asset Pricing Model (CAPM): VAR(R

A

) =  VAR(R

M

) +

VAR(R

M

) +  . When reordering the terms, the model to calculate IDIOS is obtained (Silveira, Barros, & Famá, 2008).

. When reordering the terms, the model to calculate IDIOS is obtained (Silveira, Barros, & Famá, 2008).

[Equation 2]

[Equation 2]

In order to identify the existence of a relationship between levels of tax aggressiveness and the components of systemic and idiosyncratic risks, we used the linear regression models for fixed effects data according to the following equations:

[Equation 3]

[Equation 3]

[Equation 4]

[Equation 4]These models verify the possible significance between the level of systemic risk of the next period to the measurement of TBTD –equation (3) and ETR– equation (4), as a proxy of tax aggressiveness. Beta(t+1) is the company’s next period Beta market; TBTD is the measurement of the temporary book-tax difference; the ETR is the effective tax rate; NM represents the B3 stock exchange segment called ‘Novo Mercado’; SIZE is the firm’s size; FINLEV is the financial leverage, and ROE is the return on equity; α0 is the intercept and Ԑ is the error associated with the model.

[Equation 5]

[Equation 5]

[Equation 6]

[Equation 6]The models test the correlation at a confidence level of 5%, between the idiosyncratic risk of the next period to the proxies of tax aggressiveness, TBTD – equation (5), and ETR – equation (6). It was used different periods to see the effect of a level of tax aggressiveness in the next period levels of risk.

Results

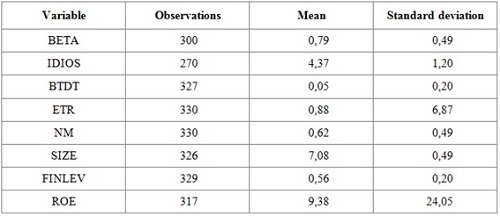

This research adopted Pearson’s correlation of statistical tools and fixed effects panel regression. The econometric analysis was carried out using the statistical program Stata. Table 5 shows the result of the descriptive statistics. The independent variables are lagged concerning the dependent variables to identify influences (in t+1) from the variation of the data of the independent components in the risks examined. Size is expressed in log function.

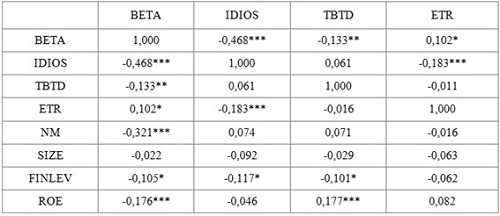

Table 6 shows the result of the correlation between the analyzed variables. The TBTD measurement presented an inverse relationship with the market risk variable, with a significance level of 5%. There was no significance for TBTD in a direct relationship with the idiosyncratic risk. For ETR, this ratio is reversed: there is a direct relationship with systematic risk, with the significance of 10%, and the opposite with idiosyncratic risk, with the significance of 1%. These results presented for TBTD and ETR, according to Araújo et al. (2018) are convergent. It is possible to infer, therefore, that the higher the firm’s tax aggressiveness, the lower its market risk and the higher its specific or idiosyncratic risk.

Regarding the control variables, the data presented an inverse and significant relationship between the components of the Novo Mercado segment, financial leverage, return on equity, and the systematic risk, with a significance of 1%, 10%, and 1%, respectively. In this way, it is possible to say that the higher the levels of NM, FINLEV, and ROE of a company, the lower its market risk. Financial leverage was inversely correlated with idiosyncratic risk (significance of 10%), which could mean that companies that are more financially leveraged have a lower specific risk. The data also point to an inverse relationship between the variable FINLEV and TBTD, with a significance of 10%, and a direct relationship between the return on equity and TBTD. Therefore, the more leveraged companies tend to present a lower level of tax aggressiveness and those with a higher return on equity, show a higher level of tax aggressiveness. No other significant relationships were found. The findings for the variable NM are in line with the studies carried out by Besarria & Silva (2017) and Vello & Martinez (2017). The results for the relationship with the variables size and market risk do not confirm the findings of Amorim, Lima, & Pimenta Júnior (2014).

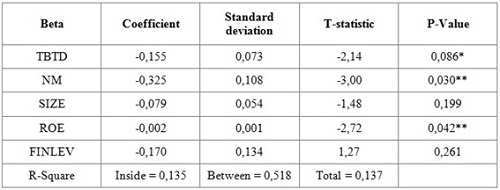

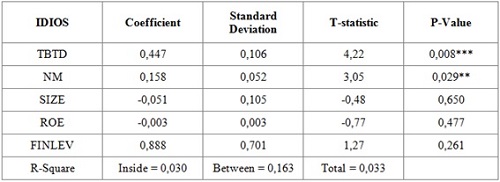

When using the TBTD as a proxy that captures the firm’s tax aggressiveness in relation to systematic risk (table 7), the coefficient found in the regression is negative, with the significance of 10%. The literature on the subject indicates that the greater the value of BTD, the higher the firm’s tax aggressiveness. This assumption suggests, in the light of the findings, that the higher the level of tax aggressiveness of an organization, the smaller its Beta.

The Novo Mercado and return on equity variables, both with the significance of 5%, presented negative coefficients, indicating an inverse relationship between these variables and the systematic risk. These results indicate that the higher the degree of corporate governance and the results achieved regarding the company net worth, the lower is its market risk.

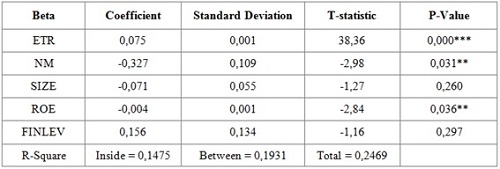

When the data refer to the ETR measurements of tax aggressiveness, due to the Beta (table 8), the coefficient found is positive, with a significance of 1%. When considering that, according to the literature on the subject, the lower the ETR value of an organization, the higher the tax aggressiveness. The findings converge with the data for BTD, reinforcing that the higher the firm’s tax aggressiveness; its Beta will be less expressive.

The data presented for the control variables reinforce the findings when the TBTD is the measurement of tax aggressiveness. The data suggest, once again, that companies with a higher level of governance and higher ROE may present lower market risks.

The data obtained when the dependent variable is the idiosyncratic risk, and the independent variable is the measurement TBTD (table 9), shows a positive coefficient, establishing a direct proportionality, with the significance of 1%. In the literature, this result may mean that the organization’s idiosyncratic risk is proportional to its tax aggressiveness. Therefore, the higher the tax aggressiveness, the higher the idiosyncratic risk. The only control variable that presented significance was the variable ‘Novo Mercado’. For this variable, the result was a negative coefficient, which may mean that organizations that have a higher level of governance present a more significant idiosyncratic risk.

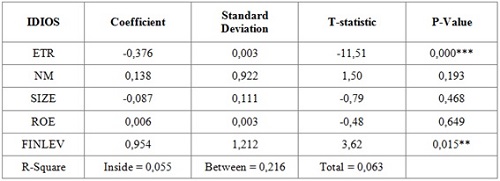

When the ETR is the measurement adopted to explain tax-aggressiveness in relation to the firm’s idiosyncratic risk (table 10), the coefficient found is negative, with a significance of 1%. It is possible to infer, in this case, that the findings converge with the data for TBTD, i.e., the more tax aggressive the company is, the more expressive its idiosyncratic risk is. Only the financial leverage variable presented significance (5%). The coefficient found was positive, indicating that the more leveraged a company, the higher its idiosyncratic risk.

It should be added that even though they are not documented in the tables, additional tests were performed to assure the robustness of the statistics. Among these should be highlighted: (i) the Jarque-Bera (JB) normality test, indicating that the residuals have a normal distribution; (ii) The Factor Inflation Variance (FIV) test presented high values close to 4,000, which however were below the limits that would be characterized as serious problems of multicollinearity, and (iii) The Breusch-Godfrey (BG) test, which found that there is no autocorrelation among the residuals.

Discussion of results

This research aimed to verify the influence of tax aggressiveness on the market and idiosyncratic risks in Brazilian companies. The dependent components of the adopted models were the market and idiosyncratic risks in the next period and, as independent variables, we adopted the measurements ETR and BTD, which capture the intensity of the tax aggressiveness. The following components were used as control variables for this study: a dummy for the market segment ‘Novo Mercado’, a firm’s size, ROE, and financial leverage.

Compare to previous studies, the work of Araújo et al. (2018) points out the direct relationship between the levels of tax aggressiveness and the measurement book-tax differences, and the inverse relationship between tax aggressiveness and the effective tax rate. Thus, it is possible to infer that more tax aggressive forms present higher values for BTD and lower for ETR.

Other studies indicate that tax aggressiveness increases organizational risk. Vello & Martinez (2014) and Guenther, Matsunaga, & Williams (2017) agree with this thought, although the latter did not find any significant relationship between a company’s total risk and its tax aggressiveness.

In this study, the total risk was divided into market risk and idiosyncratic risk, aiming to verify if there is risk enhancement in different environments. The results on this research showed a significant relationship between a firm’s degree of tax aggressiveness and the components of the risks studied (market and idiosyncratic). It is possible to infer that the higher the tax aggressiveness of an organization, the less expressive its beta, and the higher its idiosyncratic risk. The result obtained from the direct relationship between tax aggressiveness and idiosyncratic risk corroborates the literature (see tables 9 and 10). For Guenther, Matsunaga, & Williams (2017) this result may be reflecting the dispersion of probable returns due to the high future unpredictability. This is due to tax deferral practices and associated tax risks, from notices of infractions, tax fines, and damages to corporate reputation.

The inverse relationship between market risk (Beta) and tax aggressiveness may be reflecting a greater attractiveness of these assets in investment portfolios that seek a better balance and lower risk (see tables 7 and 8). In this case, assets of more tax aggressive companies would have their idiosyncratic risk diversified. Due to these companies’ beta, they could work as a kind of hedge in a diversified portfolio, considering they are less sensitive to market variations.

Using the results documented in this research, an investment manager can structure a portfolio of investments in actions to manage risks and optimize the returns. The less aggressive tax companies have a lower idiosyncratic risk. However, they tend to have higher systematic risk, which makes them more sensitive to market variations. In turn, those companies that are more tax aggressive have a higher idiosyncratic risk, but in an investment portfolio, they reduce the risk of the portfolio by reducing the total risk.

Business managers can also use the results documented in this research as guides to understand how their decisions regarding their tax planning will impact their systematic and idiosyncratic risk in the future period. Strategic business managers should reconcile their tax planning practices with the risk management of their stocks, to decide in the best interest of their shareholders in the capital market, generating value for them.

Conclusions

In this study, it was identified that the level of tax aggressiveness of a company influences its systematic and idiomatic risk in the subsequent period. Whether they are investment managers or business managers, if they are interested in creating value, they cannot ignore the role played by the tax practices on stock risks in Brazil.

More tax aggressive companies tend to present in the subsequent period higher idiosyncratic risk and lower systematic risk. In turn, in the opposite direction, companies less tax aggressive tend to have lower idiosyncratic risk and higher systematic risk.

In general terms, in the analysis of an individual asset, the tax aggressiveness leads to an increase in the company's own risk, probably due to the perception of higher tax risk. However, from the perspective of a portfolio, a more tax aggressive would reduce the systematic risk (beta), make this asset more interesting to compose a portfolio, and, through diversification, reduce the total risk.

In the analysis, it was used, as tax aggressiveness metrics, the effective tax rate –ETR–, and temporary book-tax differences –TBTD–. The focus was to concentrate on the effect of taxes on earnings, focal points for market risk analysis. Indirect taxes, although relevant in the Brazilian reality, have the characteristic of being transferred to clients. Companies that pay more indirect taxes are not necessarily less tax aggressive. They are only transferring to third parties the tax burden, which would compromise the analysis that was developed, focused on the result for the shareholder. Given the focus on this study for direct taxes, only the corporate tax contingent on net income was analyzed.

A better understanding of the effects of tax aggressiveness taxation on a financial market such as the Brazilian market was a gap in international literature. International Investors who allocate their portfolio in a global setting, would appreciate knowing what the effects of tax aggressiveness in an emerging market are. The findings in this sense are useful also for the portfolio investor and business managers from an international perspective.

The limitation of this study’s capacity of generalization lies in its focus on the period post-full adoption of the IFRS in Brazil, and the small number of companies that belong to the Bovespa index. Notwithstanding, these limitations do not reduce the relevance of the research for investors, managers, and the financial market in general.

In future discussions on the topic, we suggest an expansion of the sample, going beyond the companies that belong to the theoretical portfolio of the BOVESPA Index. Also, future studies should explore a relativization of the results with the instability levels of the national and international economy. Another potential expansion of the scope of the recordings would be to verify how this relationship is manifested between risk and aggressiveness in different economic contexts, i.e., scenarios of economic growth or stagnation.

References

Amorim, A. L. G. C., Lima, I. S., & Murcia, F. D. (2012). Análise da relação entre as informações contábeis e o risco sistemático no mercado brasileiro. Revista Contabilidade & Finanças - USP, 23(60), 199-211. http://dx.doi.org/10.1590/S1519-70772012000300005

Amorim, A. L. G. C., Lima, I. S., & Pimenta Júnior, T. (2014). Informação contábil e beta de mercado. Revista Universo Contábil, 10(4), 128-143. http://dx.doi.org/10.4270/ruc.2014433

Araújo, R. A. M., Leite Filho P. A. M., Santos, L. M. S., & Câmara R. P. B. (2018). Agressividade fiscal: uma comparação entre empresas listadas na NYSE e BM&FBOVESPA. Enfoque: Reflexão Contábil, 37(1), 39-54. http://dx.doi.org/10.4025/enfoque.v37i1.32926

Besarria, C. N. & Silva, H. S. (2017). A efetividade da governança corporativa sobre o risco dos ativos da BM&FBOVESPA. RACE: Revista de Administração, Contabilidade e Economia , 16(3), 933-956. https://doi.org/10.18593/race.v16i3.13318

Cardoso, T. A. O., Costa, P. S., & Ávila, L. A. C. (2017). A persistência da Book-Tax Differences nas companhias abertas brasileiras após a adoção do International Financial Reporting Standards (IFRS). Revista Alcance, 24(4), 462-475. https://doi.org/10.14210/alcance.v24n4(Out/Dez).p462-475

Consul, C. C. & Saito, A. T. (2014). Desempenho de carteiras selecionadas pelo uso do ROE entre 2008 e 2013. Caderno Profissional de Administração da UNIMEP, .(1), 92-102. http://www.cadtecmpa.com.br/ojs/index.php/httpwwwcadtecmpacombrojsindexphp/article/view/54

Costa, B. M. N., Leal, P. H., & Ponte, V. M. R. (2017). Determinantes da divulgação de informações de risco de mercado por empresas não financeiras. RACE: Revista de Administração, Contabilidade e Economia, 16(2), 729-756. https://doi.org/10.18593/race.v16i2.12204

Fonseca, K. B. C., & Costa, P. S. (2017). Fatores determinantes das Book-Tax Differences. Revista de Contabilidade e Organizações, 11(29), 17-29. https://doi.org/10.11606/rco.v11i29.122331

Guenther, D. A., Matsunaga, S. R., & Williams, B. M. (2017). Is tax avoidance related to firm risk? The Accounting Review, 92(1), 115-136. https://doi.org/10.2308/accr-51408

Guimarães, G. O. M., Curvello, R. S., Marques, J. A. V. C., & Macedo, M. A. S. (2016) Gerenciamento tributário: evidências empíricas no mercado segurador brasileiro. Revista Contemporânea de Contabilidade, 13(30), 134-159. http://dx.doi.org/10.5007/2175-8069.2016v13n30p134

Machado, M. C., & Nakao, S. H. (2012). Diferenças entre o lucro tributável e o lucro contábil das empresas brasileiras de capital aberto. Revista Universo Contábil, 8(3), 100-112. http://dx.doi.org/10.4270/ruc.2012324

Marinho, K. B. A., Menezes, T. A., Lagioia, U. C. T., Carlos Filho, F. A., & Lemos, L. V. (2013). Indicadores financeiros e contábeis que influenciam a tomada de decisão do investidor na elaboração de uma carteira de ações e na determinação do nível de risco. Revista Evidenciação Contábil & Finanças, 1(2), 52-68. http://dx.doi.org/10.18405/recfin20130204

Marques, A. V. C., Costa, P. S., & Silva, P. R. (2016). Relevância do conteúdo informacional das Book-Tax Differences para previsão de resultados futuros: evidências de países-membros da América Latina. Revista Contabilidade & Finanças - USP, 27(70), 29-42. https://doi.org/10.1590/1808-057x201501570

Martinez, A. L., & Silva, R. F. (2017). Agressividade fiscal e o custo de capital de terceiros no Brasil. Revista de Gestão, Finanças e Contabilidade, .(1), 240-251. https://doi.org/10.18028/2238-5320/rgfc.v7n1p240-251

Mello, H. R., & Salotti, B. M. (2013). Efeitos do regime tributário de transição na carga tributária das companhias brasileiras. Revista de Contabilidade e Organizações, 7(19), 3-15. https://doi.org/10.11606/rco.v7i19.55517

Mendonça, M. J., & Sachsida, A.. (2012). Existe bolha no mercado imobiliário brasileiro? Texto para Discussão, Instituto de Pesquisa Econômica Aplicada (IPEA), https://www.ipea.gov.br/portal/index.php?option=com_content&id=15348

Pilati, R. H., & Theiss, V. (2016). Identificação de situações de elisão e evasão fiscal: Um estudo com contadores no estado de Santa Catarina. Revista Catarinense da Ciência Contábil, 15(46), 61-73. http://dx.doi.org/10.16930/2237-7662/rccc.v15n46p61-73

Ramos, M. C., & Martinez, A. L. (2018). Agressividade tributária e o refazimento das demonstrações financeiras nas empresas brasileiras listadas na B3. Pensar Contábil, 20(72), 4-15. http://www.atena.org.br/revista/ojs-2.2.3-06/index.php/pensarcontabil/article/view/3366

Rezende, G. P., & Nakao, S. H. (2012). Gerenciamento de resultados e a relação com o lucro tributável das empresas brasileiras de capital aberto. Revista Universo Contábil, 8(1), 6-21. http://dx.doi.org/10.4270/ruc.2012101

Rodrigues, M. A., & Martinez, A. L. (2018). Demora na publicação das demonstrações contábeis e a agressividade fiscal. Pensar Contábil, 20(71), 14-23. http://www.atena.org.br/revista/ojs-2.2.3-06/index.php/pensarcontabil/article/view/3317

Silva, C. L., Fávero, L. P. L., & Almeida, J. E. F. (2016). Lucro abrangente e medidas de risco total e sistemático de companhias brasileiras de capital aberto. Revista de Finanças Aplicadas, .(3), 1-37. http://www.financasaplicadas.net/index.php/financasaplicadas/article/view/321

Silveira, A. M., Barros, L. A. B. C., & Famá, R. (2008). Atributos corporativos e concentração acionária no Brasil. Revista de Administração de Empresas, 48(2), 51-66. https://doi.org/10.1590/S0034-75902008000200005

Souza, L. C., Massardi, W. O., & Pires, V. A. V. (2017). Otimização de carteira de investimentos: Um estudo com ativos do Ibovespa. Revista de Gestão, Finanças e Contabilidade, .(3), 201-213. https://doi.org/10.18028/2238-5320/rgfc.v7n3p201-213

Vello, A. P. C., & Martinez, A. L. (2014). Planejamento tributário eficiente: uma análise de sua relação com o risco de mercado. Revista Contemporânea de Contabilidade , 11(23), 117-140. http://dx.doi.org/10.5007/2175-8069.2014v11n23p117

Notes

*

Research paper.

Author notes

a Corresponding author. E-mail: antoniolopomartinez@gmail.com

Additional information

Cited as: Lopo Martinez, A., & Botão Martins, W. B. (2020). Tax aggressiveness, market and idiosyncratic risks in Brazil. Cuadernos de Contabilidad, 21. https://doi.org/10.11144/Javeriana.cc21.amir