APA

ISO 690-2

Harvard

Haga clic en un formato de citación

Value Relevance of net income, other comprehensive income, and comprehensive income in Brazil*

Relevancia de valor del ingreso neto, otros ingresos comprensivos y el ingreso integral en Brasil

Relevância de valor do Lucro Líquido, outros resultados abrangentes e a renda abrangente em Brasil

Cuadernos de Contabilidad, vol. 21, 2020

Pontificia Universidad Javeriana

Cassiana Bortoli a cassianabortoli@gmail.com

Universidade Federal do Paraná, Brasil

Alcido Manuel Juaniha

Universidade Rovuma, Mozambique

Jorge Eduardo Scarpin

Concordia College Moorhead MN, Estados Unidos

Nayane Thais Krespi Musial

Universidade Federal do Paraná, Brasil

Claudio Marcelo Edwards Barros

Universidade Federal do Paraná, Brasil

Received: 30 July 2019

Accepted: 25 June 2020

Published: 17 October 2020

Abstract:

This paper uses the Ohlson Model to analyze whether Net Income (NI), Other Comprehensive Income (OCI), and Comprehensive Income (CI) are value relevant for market value and the return of shares of publicy-traded Brazilian companies. To maximize the robustness of the results, we inserted the following control variables for each model: equity per Share (EqPS), Size (S), Industry (I), EBITDA per Share (EbPS), Revenue per Share (RePS), Liquidity (L), and Gross Domestic Product Growth (GDPG). The control variables S, RePS, and GDPG were significant for the three models related to the value of the company. The control variables EqPS, EbPS, RePS, and L, on the other hand, were only significant for the three models related to stock returns. Our main variables (NI, OCI, and CI) were found to be statistically significant in five of the six regression models after data analysis in a fixed effect panel using robust standard errors. However, only the variables NI and CI were considered to be relevant in the expected direction, meaning that they offered a positive contribution in explaining the value of the company. JEL Codes: M40, M41.

Keywords:Market Value, Stock Return, Net Income, Comprehensive Income, Other Comprehensive Income.

Resumen:

Este artículo utiliza el modelo de Ohlson para analizar si existe una relevancia del valor de mercado y el rendimiento de las acciones sobre la información del Ingreso Neto (NI), Otros Ingresos Comprensivos (OCI) y el Ingreso Integral (IC) de empresas brasileñas cotizadas en la BM&FBOVESPA. Para maximizar la solidez de los resultados, incluimos las siguientes variables de control para cada uno de los modelos: Patrimonio por acción, Tamaño, Industria, EBITDA por acción, Ingresos por acción y Liquidez. Estas variables de control fueron especialmente significativas para los tres modelos relacionados con la rentabilidad de las acciones, excepto la de industria y la liquidez. Obtuvimos significación estadística de nuestras variables esenciales (IN, OCI e IC) en cinco de los seis modelos de regresión con análisis de datos en panel con efectos fijos y errores estándar robustos. Sin embargo, solo las variables NI y CI fueron consideradas como relevantes en la dirección esperada. Esto permite afirmar que dichas variables ofrecen una contribución positiva en la explicación del valor de la compañía. Códigos JEL: M40, M41.

Palabras clave: Valor de relevancia, devolución de stock, ingresos netos, ingreso integral, Otros ingresos integrales.

Resumo:

Este trabalho tem como base o Modelo de Ohlson para analisar se há relevância do valor do mercado e o rendimento das ações sobre a informação do Lucro Líquido (IN), Outros Resultados Abrangentes (OCI) e Renda Abrangente (IC) de empresas brasileiras listadas na BM&FBOVESPA. Para maximizar a robustez dos resultados, inserimos as seguintes variáveis de controle para cada um dos modelos: patrimônio líquido por ação (EqPS), tamanho (S), setor (I), EBITDA por ação (EbPS), receita por ação (RePS), liquidez (L) e crescimento do produto interno bruto (GDPG). As variáveis de controle S, RePS, GDPG foram significativas para os três modelos relacionados ao valor da empresa. Já, as variáveis de controle EqPS, EbPS, RePS, e L foram significativas para os três modelos relacionados ao retorno da ação. Obtivemos significância estatística das nossas variáveis essenciais (IN, OCI e IC) em cinco dos seis modelos de regressão com análise de dados em painel com efeitos fixos e erros padrões robustos. Entretanto, somente as variáveis NI e CI foram consideradas relevantes na direção da relação esperada, contribuindo de forma positiva para a explicação do valor da empresa. Códigos JEL: M40, M41.

Palavras-chave: Valor de mercado, retorno das ações, lucro líquido, resultado abrangente, outros resultados abrangentes.

Introduction

In this study, we seek to verify whether the relevance of a company’s value can be explained by its net income, by its comprehensive income, and by other comprehensive income. Accounting information is relevant if it can capture the intrinsic value of a company and influence the return on stocks (Barth, Beaver & Landsman, 2000; Beisland, 2009). Net income, succinctly, refers to corporate profits. It is an accounting measure used by investors to evaluate the capacity of the company of generating returns on their investments and increase their overall value. On the other hand, the statement of comprehensive income shows changes in net equity. According to Biddle & Choi (2006), the changes are the operating net income of the company. They include items related to currency exchange (translation adjustment), pension liability to be recognized, unrealized gains and losses, and assets and liabilities to be measured by market value. Therefore, while preparing the statement of comprehensive income, it can be assumed that the resulting statement should be more closely related to the company value and stock performance shares, since it presents values closer to the reality. That is because this statement is made up of a result that derives from the sum or involve the components of the result. The reasons for publicizing the statement of comprehensive income, according to Kanagaretnam, Mathieu, & Shehata (2009), is the imposition of norms by the regulatory system which aims to increase transparency and make public the accounting information offered to the capital market. As a result, the information will be provided that is more relevant than that on net income.

The discussion on the relevance of comprehensive income statements, when compared to the relevance of income statements, is varied. There are many research approaches related to the decision of making the statements public. For example, literature presents results according to which comprehensive income is more relevant than net income to predict future cash flow (Wang, Buijink, & Eken, 2006) and stock price and returns (Kanagaretnam et al., 2009). As an alternative, other studies suggest the net income is more relevant than the comprehensive income to predict future cash flow (Goncharov & Hodgson, 2011). In addition to these approaches, we also found specific studies that include certain components of the comprehensive income, such as the relevance of currency exchange for stock value (Devalle & Magarini, 2012). Therefore, it becomes clear that these studies increasingly seek to identify which results (for example, net income, comprehensive income, or other comprehensive income) can better explain or predict cash flow, as well as stock price and expectations on stock returns. The results, however, have been quite contradictory.

It should be highlighted that these items should be measured based on the requirements of Brazilian regulatory agencies (for example, the Statement of Financial Accounting Standards 130 Comprehensive Reporting, the International Accounting Standards 1, the Committee of Accounting Statements 26, and the Financial Statements Presentation). In September 2007, the International Accounting Standards Board –IASB– publicized the International Accounting Standards 1 (IAS 1), valid for fiscal years started on December 31, 2008. This standard requires comprehensive income –CI– and its components, net income –NI– and other comprehensive income –OCI– to be made public in the financial statements of the period in which they were recognized. This was already prescribed by the SFAS 130 from the Financial Accounting Standards Board (FASB) in the United States, in June 1997 (Dhaliwal, Subramanyam & Trezevant, 1999). In Brazil, the CPC 26 is in line with the requirements from IAS 1 and requires public companies to publicize their comprehensive income statements in all their financial statements starting from 2010. Therefore, as a consequence of standardized requirements, international empiric researches were carried out to evaluate which of these declarations would be a good performance measurement from the perspective of investors.

Investors are interested in predicting the value of their investments. Depending on the context, we believe that it is possible to find the relevance of value in NI, in CI, and in OCI, which is more intense, since these make the financial and economic position of the company even more visible. As a consequence, the guiding question of our research is: How relevant are net income, comprehensive income, and other comprehensive income with regards to the market value and the stock returns of Brazilian companies listed at BM & FBOVESPA?

This investigation uses, as the base of its development, the Ohlson’s model (1995), aiming to verify the relevance of the NI, the CI, and the OCI in the stock returns of public Brazilian companies. The justification of this study is related to the important changes in Brazilian accounting legislation, which led it to become convergent to international accounting standards, reflecting on the financial statements that started to be presented in 2010. These statements start to consider the economic substance. Therefore, starting from the aforementioned change in Brazilian legislation, results/profit are considered to be “cleaner” (since fiscal adjustments must be done in specific statements to the treasury, and not in accounting records), motivating the market to find value relevance in this information. These changes had been expected by the investors, but, mostly, started to be implemented in accounting in 2010. This created the expectation of the possibility of obtaining more quality information, in addition to further relevant information.

Theoretical-empirical framework and research hypotheses

Historically, agents have more information than the principals, which can be understood through information asymmetry. As a result, financial reports aim to correct these problems. Investors and creditors are seen as the most demanding among the interested parties with regards to the accounting information found in the reports, since they use this information, combined with intuition, to predict outcomes (Barth et al., 2000; Beisland, 2009; Kousenidis, Ladas & Negakis, 2009). Studies suggest that, after the adoption of international accounting standards, there was a significant increase in the relevance of the value of accounting information in Europe (Clarkson et al., 2011) and emerging markets (Alali & Foote, 2012; Elshandidy, 2014). Studies have also indicated that corporate profit is likely to contain information on future advantages that may result from it (Franzen & Radhakrishnan, 2009). As a result, this study uses the theory of value relevance, as operationalized by Ohlson’s model, to investigate whether the information about NI, CI, or OCI has predictive value with regards to the return on stocks.

Net Income

The main objective of publicizing net income is to provide interested parties with useful information for decision making, thus diminishing information asymmetry (Hendriksen & Van Breda, 1999). According to these authors, publicizing the NI in financial reports may lead to different specific objectives from the interested parties, such as NI as a measure of the efficiency of a company's administration; historic data on NI as an instrument to predict the future trajectory of the company or the future payment of dividends; and NI as a measure of performance and guidance for future managerial decisions. The net income, according to the Generally Accepted Accounting Principles –GAAP–, includes deductions, such as unrealized gains and losses in for sale securities, translation adjustments for foreign currencies, pension liability adjustments, and changes in the values of certain futures qualified as market hedges, violating the idea of a “clean profit” (Skinner, 1999; Biddle & Choi, 2006). Therefore, starting from the adoption of the International Financial Reporting Standards –IFRS–, the Statements of Outcome in Brazil will express only the value that makes up the results of the period and their variations.

After the adoption of the IFRS, NI would present fair values resulting from the variation of the elements that make it up. Tsalavoutas, André & Evans (2012) carried out a study in Greece to verify the predictive value of net equity and net income before and after the mandatory transition into IFRS, also verifying possible variations. They believed that, after the transition from the local GAAP to the IFRS, the information presented in financial statements could offer more transparency and increased predictive value. However, the results of their research contradicted their beliefs, showing that there was no significant change in the relevance of the value of NI between the periods. Mironiuc, Carp, & Chersan (2015) also investigated the relevance of the value of CI over NI in companies in Romania. Their results showed that investors from the financial market gave more relevance to the accounting information after the International Accounting Standards were adopted.

Considering the above, the following research hypotheses were elaborated:

Hypothesis 1: The Net Profit has a relevant value for the Market Value of the companies listed in BMG & BOVESPA.

Hypothesis 2: Net Profit has a relevant value for the return on stocks of the companies listed in BMG & BOVESPA.

Comprehensive Income

In Brazil, the NI, before the acceptance of international accounting standards, involved balances that, after the IFRS was adopted, were highlighted in the Statements of Comprehensive Income, in such a way that the Statements of Income show the “clean” profit, and the Statements of Comprehensive Income show the income discount of the adjustment of previous fiscal periods. Therefore, a CI aims to show an economic profit that is closer to reality and becomes an important tool for management analysis. However, according to Skinner (1999), CI recognizes the same information previously divulged in the statement of income, and it is difficult to understand why CI would be more closely related to the returns on the net equity than to NI. According to the author, this can be seen in the concept of CI of the SFAS 230, which includes all changes in the assets of the company, except the investments of the owners and the distribution to the owners. The SFAS 130, which involves the dissemination of CI, was published in June 1997 (Skinner, 1999), but Johnson, Reither, & Swieringa (1995) discussed which results represented the financial outcomes of the company before this date. The question of where it is most appropriate to publicize these values was already confusing for researchers at that time when companies could decide where the information was made public. In this sense, one could imagine how difficult it was, especially for small investors, to identify and interpret these differences.

Although standardization agencies from IASB and CPC consider it adequate to publicize two results, considering the historic adjustment of cost and fair value, many authors discuss the existence of a comprehensive statement of the outcomes. Dhaliwal et al. (1999) showed that the SFAS 130 would be the culmination of a debate that has been held for long in accounting. This debate involves the “full inclusion” (comprehensive income) and the concept of “current operational performance”. They investigated which, CI or NI, was the best option to summarize the performance of a company as reflected by the return on the stocks. They analyze also which components of the SFAS 130 improve the production capacity to summarize the performance of the company. However, they did not find clear empirical evidence showing that CI would be more strongly associated to returns than NI, with regards to its explanatory power. The results of this comparison between NI and CI were highly unstable, depending on the country from where the sample for each investigation was obtained. This result could be related to the importance attributed to user’s perception of the quality of accounting statements. That because users could be trying to assess the reputation of the company and the regulations in force in each country to safeguard a fair and subjective value method, ever since the start of their measurements.

Considering the above, the following research hypotheses were elaborated:

Hypothesis 3: The Comprehensive Income has a relevant value for the Market Value of companies listed in BMG & BOVESPA.

Hypothesis 4: The Comprehensive Value has a relevant value for the Return on Stocks of the companies listed in BMG & BOVESPA.

Other Comprehensive Income

An investigation by Serrat, Gutierrez & Perez (2011) showed that the CI values the relevance of both market value and predictions of future profitability. However, a number contained in the statement of CI called the attention of researchers, as was the case for OCI. Kanagaretnam et al. (2009) researched the predictive value of the information contained in CI, OCI, and NI, separately. They found that one of the most important evidences in their study relates to changes in the fair value of the investments available for sale (other comprehensive income), which were positively tied to the price of stocks. Dhaliwal et al. (1999) could not prove, statistically, that CI would have a higher predictive value for the returns than NI. However, they were able to identify that the component of SFAS 130 that improves the association between result and returns is the adjustment of negotiable securities from the sectorial bank. Biddle & Choi (2006) found evidence that the components of CI may bring useful information into the market. The studies mentioned here report the relevance of the components of CI as considered separately. As a result, some researchers, such as Schaberl & Victoravich (2015) have questioned whether the means of publication of this information may be influencing the use or lack thereof of these values as a predictive tool.

Schaberl & Victoravich (2015) investigated whether finding OCI, such as statements of CI or net equity, could lead to variations in the relevance of value. They found that, ever since the IFRS was adopted, the relevance of OCI had been diminishing, verifying that this is determined by the historical location where the company publicizes the value. From that, we gathered that the interested parties use this information, but it does not receive attention enough. Considering the changes in the measurement methods implemented with the decision to follow the IFRS, the users of the accounting information should be more cautious, by using the information that was measured according to its historical cost. Considering that SFAS 130 allowed companies to choose to report components of the CI in their statements of net equity or their statements of performance, the FASB issued the Accounting Standards Update –ASU– 2011-05, to improve the comparability, consistency, and transparency of financial information (Schaberl & Victoravich, 2015). This document eliminated the option of reporting the components of the CI in the statements of net equity. It allows performance statements to be issued in two different formats: (1) in a single statement of CI, with its components immediately below the net income; or (2) in the form of two statements, one of which includes the full CI balance, while the other presents its components.

Considering the above, the following research hypotheses were elaborated:

Hypothesis 5: The Other Comprehensive Income has a relevant value for the Market Value of companies listed in BMG & BOVESPA.

Hypothesis 6: The Other Comprehensive Value has a relevant value for the Return on Stocks of the companies listed in BMG & BOVESPA.

Methods

This research was carried out to verify whether the value of the company (its market value and its return on stocks) can be explained by net profit, OCI, and CI (to be provided by the statistical significance of the relations) of publicly traded companies listed in the Brazilian stock exchange. In the Brazilian context, the convergence to international accounting standards is recent and impacts accounting statements. In this sense, this study also aims to evaluate whether including accounting information that is considered to be more relevant (respecting the economic substance) would receive attention from investors. That means, reflecting in the market value of companies and on their returns on stocks from one tax period to the other. Answering the hypotheses proposed by this research is important for the Brazilian scientific community, as well as for that of other countries that recently adhered to international accounting standards. Additionally, the results will indicate whether this accounting information is relevant to the investors, who are considered to be rational and, as a result, interested in receiving information for decision making, including accounting information. For the research to be clearer, we will present the methodological procedures adopted in two specific sections: research context and data collection.

The context of the research in the Brazilian accounting environment

The first document which specifies rules for Equity Companies in Brazil was issued in 1940 by decree-law No. 2.627 (Rodrigues, Schmidt & Dos Santos, 2012). Rodrigues et al. (2012) report that most commercial and industrial companies were limited liability ones, and that strong European influence, such as from the Italian school of thought, led Brazil to develop in such a manner. Decree-law No. 2.627/40 gave recommendations with regards to factors such as asset evaluation, profit retention, and dividend and reserves distribution. A new process of standardizing financial reports in Brazil started with the issuing of decree-law No. 2627. However, Salotti et al. (2015) state that the standards from the decree-law were inferior to the model that was to follow, which was only issued in 1976, through Law. 6404.

The Brazilian accounting model was widely modified in 1976, with the issuing the Law of Equity Companies, No. 6.404. Brazil adhered to the best international accounting practices when the Law of Equity Companies 6.404/76 was in effect since its parameter was the North American accounting standards, seen as an international reference. As years went by, the Law of Equity Companies became increasingly obsolete with regards to internationally adopted practices, due to the need of being in sync with the evolution of financial instruments and business practices (Salotti et al., 2015). For an important period, many institutions started issuing recommendations about accounting practices which would slowly push accounting away from its research subject: asset control. As a result, Law 11.638/07 led to profound changes in Brazilian legislation, which converged with international accounting norms. Adapting statements for publicly traded companies became mandatory in 2010.

Ever since, many researchers have been making efforts to contribute with the market, with new findings with regards to the configuration of accounting, especially in the national environment (Filipin et al., 2012; Acuña et al., 2013; De Farias et al., 2014; Da Costa & Freitas, 2015). Internationally, there are still few documents about the development of Brazilian accounting (Rodrigues et al., 2012), and the market has been using accounting information from this new setting (Black, Carvalho, & Sampaio, 2014; Sampaio et al., 2014). It stands out that Brazil has the fifth larger landmass in the world and abundant natural resources (Pamplona & Cacciamali, 2017), being, as such, one of the developing countries that grow the most in the world and a member of both BRICS and the G20 (Rodrigues et al., 2012). Still, the Brazilian stock exchange remains relatively small, which can be due to the lack of standardization of Brazilian accounting, in addition to the cultural and economic environment of the country. Therefore, other countries need to get to know the existing Brazilian accounting standards, being able to use the information generated by these standards to evaluate the possibility of participating in the Brazilian stock exchange, be it searching for financing or investment opportunities.

Data Collection and Processing

The information to carry out the study was found using the Thomson Reuters and Economática databases, in addition to the statements of companies available from the Brazilian stock exchange (BM&FBOVESPA) and the Brazilian Commission of Transferable Securities. To achieve a reliable outcome, we adopted some precautions related to data, coverage period, and sample. We also used the Softwares Stata and EViews to extract results from the statistical tests and graphs.

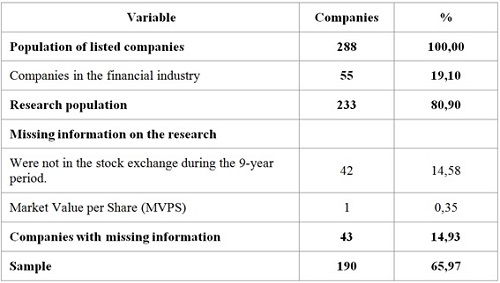

The Statement of Comprehensive Income is mandatory for publicly traded companies in Brazil since 2010. However, we found it necessary to exclude the year 2010 from our sample, since it would significantly restrict the number of companies in the sample due to a lack of data. Consequently, the period analyzed was from 2011 to 2019. The research population was made up of all companies listed at BM & BOVESPA, the Brazilian stock exchange. That means that the 288 companies listed there were included in May 2019. That is the date when data collection and the test of the research were made. However, 98 companies had to be excluded due to a lack of data. The final sample included 190 companies for nine years, totaling 1710 cases.

The details of the composition of the sample can be found in table 1.

As table 1 show, 55 companies from the financial sector were excluded after the inclusion of control variables to the model. The control variable EBITDA is only pertinent for non-financial companies since the structure of its statements is different. The inclusion of control variables allows for greater consistency in the possible significance of independent interest variables. That means they are used to control whether the effects of independent variables (net equity, NI, OCI, and CI) on depending variables (market value and return on stocks) remain the same when there are other interferences. Therefore, control variables contributed to testing the efficiency of the model, since the significance of independent variables remains, and the model is understood as being more robust. Therefore, based on previous studies and the logic of the expected behaviors of the variables, this study uses the control following variables: Size, Industry, EBITDA, Revenues, Liquidity, and Gross Domestic Product Growth –GDP–.

Size: Larger companies make more information public due to being under closer supervision by competent institutions and interested parties, in addition to the needs of the market to predict future value to analyze the viability of potential investments. Also, the content of information is a target for the interest of many participants in the market, and pressures companies to divulge more and more quality accounting information, not to mention that larger companies tend to undergo more in-depth audits. That leads us to believe that precision and reliability in the publication of data is more closely related to the value of these companies and their returns on stocks than in the case of smaller ones (Biddle & Choi, 2006; Anandarajan & Hasan, 2010; Lischewski & Voronkova, 2012). We assume that size can provide different levels of value relevance between companies, and as a result, expect a positive relation to existing between the size of the company and its market value and returns on stocks. That shows that the information content is considered in the analysis of investors when companies are large-sized. We calculated this variable using the natural logarithm of the total actives of each company. This procedure makes it possible to size the companies while avoiding discrepancies that could lead to the elimination of companies due to the possibility of their being presented as outliers.

Industry: The relevance of accounting information can vary according to the classification of the industry for the companies (Dhaliwal et al., 1999; Elshandidy, 2014). Exogenous questions that reflect on the economy of each industry can be observed, and we believe that, for specific industries, the accounting results indicated as independent variables become necessary to predict Market Value and Returns (Alali & Foote, 2012). Therefore, we believe that each sector will react differently to market value and returns. This variable is equivalent to the industry classification available in the BM & BOVESPA website, and the Economática database. Industry classification had to be done through dummies. A score of 1 was attributed to the companies from a specific industry, and a score of 0 for other industries that did not fit.

EBITDA per Share: EBITDA measures the performance of the company by sizing its financial capabilities of compensating its shareholders. Therefore, return and market value may depend on the performance of this index (Veloso & Malik, 2010; Isaksson & Woodside, 2016). However, this measure assumes that all credit provided was within the year and does not consider the need for reinvesting. Despite its highlights we believe that the profitability, measured by the EBITDA, may positively and significantly explain the capacity of returns on shares. That is, the higher the EBITDA, the higher tend to be investor expectations and, consequently, their evaluation must consider higher values for the value of the company and return on shares. We used the EBITDA per Share because the dependent variables underwent the same type of work. The division of the EBITDA variable according to the number of stocks allows us to avoid discrepancies that could lead us to eliminate companies that could be considered outliers. Therefore, we consider that the volatility that remains in the results is typical of accounting variables and expressive of the real situation of the company in the market, since it was relativized.

Revenue per Share: Revenues per Share are used by many researchers as a proxy for the growth of a company (Yeh & Hsu, 2014). The Efficient Market Hypothesis is based on the premise that the value of shares contains all available market information, be it qualitative, quantitative, endogenous, or exogenous. Ohlson (1995) also shows that the accounting data is relevant to predict the value of a company. We can infer that accounting data is used by market analysts and investors to predict future returns, which is done through an analysis of the growth of the company through the years, contributing to fulfill the expectations of future return and to escalate the value of the company. We believe that companies that grow through the years can bring higher returns than companies that grow less (Yeh & Hsu, 2014; Isaksson & Woodside, 2016). As a result, we expect to find a positive relation between the income of a company and its value and returns, since a greater income tends to generate greater expectations and better evaluation of dependent variables. We used the revenue weighted by the number of shares of a company to relativize the variable, as was done for other variables.

Liquidity: Liquidity is one of the determinant factors of returns on stocks (Demir & Ersan, 2017; Lischewski & Voronkova, 2012) and company value. However, it is not directly observable and is difficult to measure. Roggi & Giannozzi (2015) describe that the volume of negotiations weighted by the available shares for negotiation was used as a proxy for this variable and considered to be a precise form of liquidity, since it is given by market behavior. According to a survey of literature on liquidity by these authors, this proxy can capture the information desired, and negotiation decline for low liquidity companies in periods of crisis (Amihud, 2002; Lischewski & Voronkova, 2012; Roggi & Giannozzi, 2015). We believe that there is a tendency for a negative relation between the liquidity of the company in the stock exchange and the market value, and its corresponding returns on negotiated shares. That is because, if we measure the liquidity according to the volume of negotiations and find a lower number of negotiations, a plausible reason must be given to the investors for them to keep it in their portfolio, such as incentives related to market value and returns. Observing the availability of the information necessary to measure this variable, we used the volume of negotiations weighted by the total number of negotiable shares for the liquidity variable, which means that the variable was also relativized.

Gross Domestic Product Growth: The political and economic uncertainties with regards to the Brazilian corporate environment reflect on the growth of the company as a whole (Demir & Ersan, 2017). As a result, it is necessary to include a macro-economic variable. For this context, the most adequate one is the Gross Domestic Product Growth. The GDP is the sum of all goods and services produced within the country in one year. If we consider the variation of this number from one year to the next, we will find information on the economic growth or decline of a country. As a result, we can expect that there will be a positive relation between the GDP Growth and market value, and the returns of companies. After all, when the economy presents a positive environment, companies tend to have better conditions, present good performance, and achieve good returns, as well as proper market value. However, when the Brazilian economy is in decline, the same is expected for the returns and the market value of the companies listed in the stock exchange of the country.

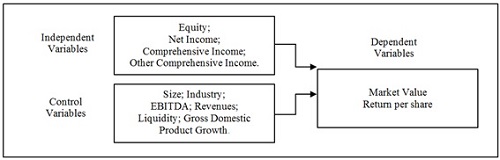

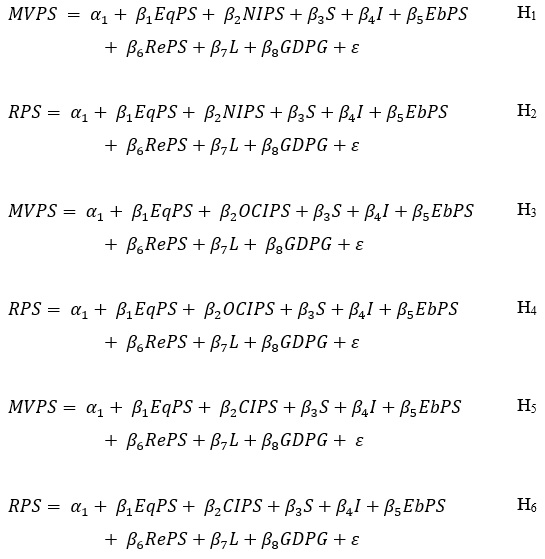

After controlling the variables Size, Industry, EBITDA, Revenues, Liquidity, and GDP growth, which we believe can also partially explain the market value and return on shares, we explain the model used to solve the problem in figure 1.

We also present the regression models used to answer each research hypothesis. Each model exposed corresponds to one hypothesis in the same order of presentation:

Where,

α1 – Intercept

β1; β2; β3; β4; β5; β6; β7 – Regression coefficients

MVPS – Market Value per Share;

RPS – Return per Share;

EqPS – Equity per Share;

NIPS – Net Income per Share;

OCIPS – Other Comprehensive Income per Share;

CIPS – Comprehensive Income per Share;

S – Size;

I – Industry;

EbPS – EBITDA per Share;

RePS – Revenue per Share;

L – Liquidity;

GDPG – Gross Domestic Product Growth;

ε – Error term.

Multivariate linear regressions were elaborated and based on Ohlson’s model (1995), since we aim to detect, on accounting data, information capable of identifying the evaluation of the company (Kanagaretnam et al., 2009; Alali & Foote, 2012). Since it is necessary to work with the data in two dimensions, space and time, we opted to use the data from the panel. This statistical technique allows us to analyze more than one company (cross-sectional analysis) throughout a period (temporal series). The analysis of data in a panel is the method used by many researchers in articles that seek to find the relevance in the value of different dependent variables (Dhaliwal et al., 1999; Biddle & Choi, 2006; Kousenidis et al., 2009). To assure the strength of our results, we were careful to carry out multivariate statistical tests of the assumptions: Durbin-Watson – residual autocorrelation; White — heteroscedasticity; Normality of Residuals — error distribution; VIF – multicollinearity; and F Test – adjust of the model. Additionally, after the assumptions were proved, we used the diagnostic and panel tests: Residual Variance, Breusch-Pagan, & Hausman. These tests help the researcher to define the model that adjusts best to the data found, allowing for an unbiased analysis. Additionally, when there are residual autocorrelation and heteroscedasticity problems, considered to be serious violations of assumptions, the Robust Standard Errors was applied in the panel regression.

Result analysis and discussion

This section is divided into two topics: Result analysis and result discussion. This distinction is necessary so that the statistical procedures adopted can be exposed and the answer to the research question be communicated. That makes it possible to investigate the reflections of the findings of this research in national and international contexts.

Result Analysis

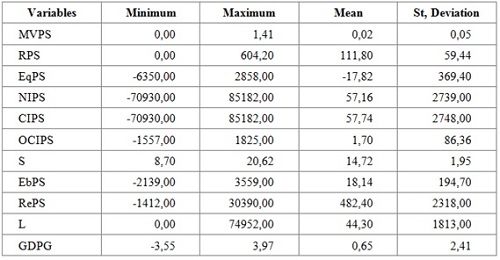

Table 2 presents the descriptive statistics of the continuous variables used in this study.

As table 2 shows, the accounting variables EqPS, NIPS, CIPS, OCIPS, EbPS, and RePS presented great variability, as shown by their high standard deviation values. Due to this high standard deviation, we emphasize for this study that, outliers were admitted. We believe that eliminating them is inadequate when the sample of companies is different in Industry and Size, which reflects the variability of results. To minimize the high variability between the companies, we were careful to parameterize accounting data according to the number of shares of the company. This procedure minimizes the discrepancies, despite not entirely eliminating them. These issues are common in the use of accounting variables, especially when one works with relatively small samples, which is a consequence of the size of the Brazilian stock exchange. As a result, the next step is testing the assumptions of multivariate analysis to make the necessary arrangements to guarantee the reliability of the study. Table 3 shows the results of the tests of the assumptions of regression.

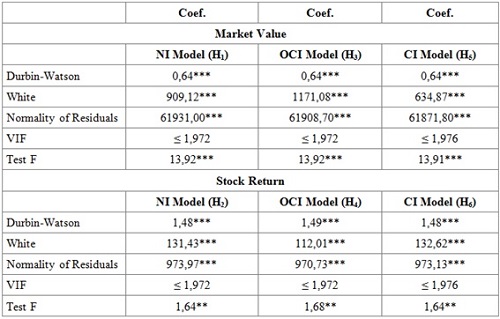

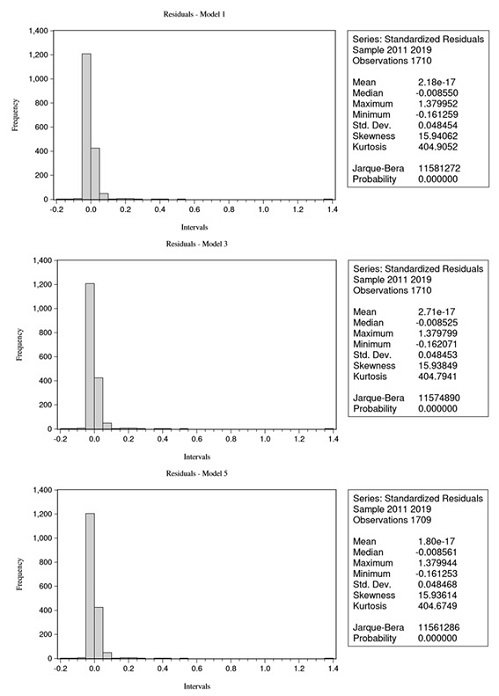

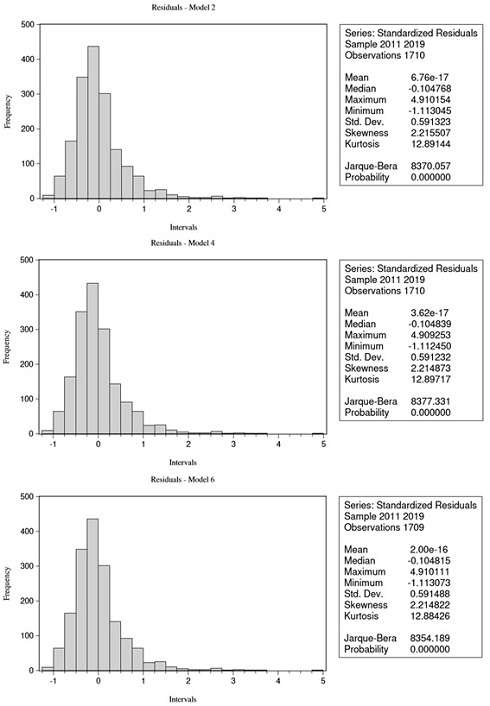

In table 3 we describe the results of the tests of the assumptions of the six linear regression models (Hair Jr et al., 2010), which presented similar results with regards to the statistical significance level of the tests for each model. The Durbin-Watson test showed the presence of autocorrelation in the residuals (p-value: ≥ 0.01). The graphical representation of the residuals in the models 1, 3, and 5 (Market Value) can be observed in figure 2, and that of the models 2, 4, and 6 (Return on Shares) can be observed in figure 3. The White Test (p-value: ≥ 0.01) indicated a rejection of the null hypothesis according to which the data presents no heteroscedasticity. The rejection of the null hypothesis of the two first tests is considered to be a serious violation of the assumptions of a multivariate analysis. Therefore, the use of all six models of robust standard errors (HAC estimators), since this methodology makes it possible to analyze data that goes against these assumptions. The test of the normality of residuals (p-value: ≥ 0.01) rejected the null hypothesis of the existence of a normal distribution, which is expected when working with accounting data. The Variance Inflation Factor (VIF), used to test the collinearity, had values under 10 for all research variables, indicating an absence of problems of multicollinearity, which is especially true due to values quite inferior to the parameter of 10. Finally, the F-Test showed that the models have a global relevance (models 1, 3, and 5 had a significance level of 1%, and models 2, 4, and 6 had a significance level of 5%), since they reject the null hypothesis of model equality, which uses only the intercept of assumed models with different intercept points.

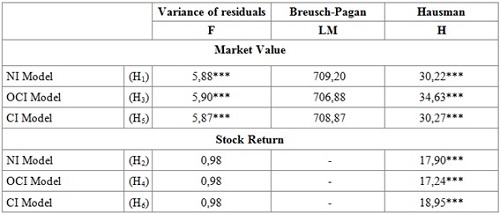

Therefore, it is possible to give continuity to the test to verify whether research data is adequate for the use of the Ordinary Least Squares –OLS–, Random Effects, and Fixed Effects. That means that any result indicated by the Residue Variance, Breusch-Pagan, and Hausman tests should consider the insertion of RSE. That is due to the negation of the assumptions of autocorrelation and heteroscedasticity.

Table 4 shows the tests carried out to verify the diagnostic of the panel that is more adequate to the data of the research.

We found that the models 1, 3, and 5 presented statistical significance for the test of Residual Variance (p-value: ≥ 0.01) and for Hausman’s test (p-value: ≥ 0.01), which indicates that the data in the model is adequate for the analysis of the data in a fixed-effect panel. Models 2, 4, and 6, on the other hand, only permitted the Residual Variance and Hausman’s tests, diminishing the possibility of random effects. Also, Residual Variance and Hausman's tests pointed at the opposite directions, the first suggesting the use of the pooled OLS and the second suggesting the use of fixed effects. As a result, we decided to adopt a more conservative approach and use the test that requires the most from the data, that is, the fixed-effects model. Additionally, since the six models lead to an analysis of regression in a panel with fixed effects and robust standard errors, they will, consequently, lead to more robust results. Besides, that makes it possible for comparative and pooled analyses of the models to be carried out.

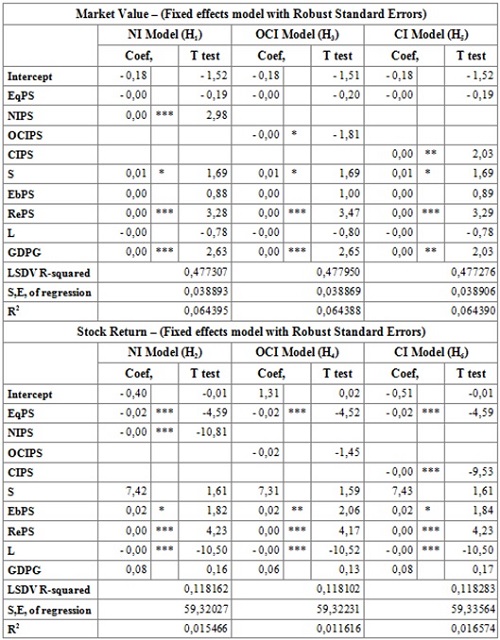

Table 5 shows the results found with the three models using the data analysis in a panel with Fixed Effects and Robust Standard Errors.

As shown in table 5, the models do not present statistics related to the variable “Industry”. This is because the analysis of the fixed-effect panel does not consider dummy variables, which do not change over time. However, the models, as a whole, are relevant, and statistically noticed by the F-Test presented in table 3. It also has a substantial relevance for literature on Accounting Sciences; both in Brazil and in other countries that are have recently adopted international accounting standards and/or have a relatively small stock market. That is because investors waited for cleaner information that reflected the real economic situation of the company and provided certain expectancy about making public NI, CI, and OCI values. Furthermore, other variables that the existing literature highlighted as important were added.

The Net Equity per Share –EqPS– did not present statistical significance for the Market Value per Share (H1, H3, and H5, whose p-values were not significant). The variable was adherent to models with returns on shares (H2, H4, and H6, whose p-value was significant at a 1% level). That shows that the higher the EqPS, the lower the return on stocks since regression coefficients were negative. However, it must be considered that we maintained, in our sample, companies whose Net Equity was negative, which could be because they have been facing economic crises during the period considered. However, investors seem to expect improvements for these companies, since the negotiation of their shares has been generating positive returns. Therefore, our study found that the EqPS is an explanatory variable for returns on stocks, but not for market value, as was expected.

Net Income per Share –NIPS– had a 1% statistical significance for both models (H1 and H2). However, the relation was positive for the first and negative for the second. The first result was expected. It indicates that the greater the value of the NIPS, the greater the value of the company. However, the second result was surprising, as it indicates that the greater the NIPS, the lower the return on shares. This result can show that the investors have no confidence in the NI reported, meaning that it increases the value of the company, but lowers the interest in negotiations.

The Other Comprehensive Income per Share –OCIPS– presented a statistical significance for model 3, but not for model 4. Still, the significance of model 3 was negative, with a confidence level of 10% (considered to be weak). However, the result seems to make sense, since adjustments, in general, reduce the value of income and, consequently, the value of the company.

The Comprehensive Income per Share –CIPS–, as well as the NIPS, showed a 1% statistical significance for both models (H5 and H6), but in opposite directions. Model 5 shows that the higher the comprehensive income, the higher the value of the company, or, the opposite, that the lower the comprehensive income, the lower the value of the company. This was the expected result. However, model 6 shows an inversely proportional relation. That is, the higher the comprehensive income, the lower the return on shares in the period. These findings may reinforce the evidence according to which shareholders see an implicit subjectivity in the methods used to measure assets and liabilities, which impacts the results.

The Size –S– had a weak statistical significance for the models related to hypotheses 1, 3, and 5, with a 10% significance level, but did not have statistical significance for the models related to hypotheses 2, 4, and 6. These results suggest that the bigger the company, the higher its corresponding market value, which is also suggested by how the proxy was measured (Natural Logarithm of the Total Asset). Still, it indicates that the size of the company does not imply in market expectations, since it has no relation to the returns of the company.

The EBITDA per Share –EbPS– was significant in the three models that aim to explain the returns on action (H2, H4, and H6). Models 2 and 6 presented a positive low significance (p-value: ≥ 0.10), while model 4, the OCIPS model, had a greater statistical significance (p-value: ≥ 0.05), pointing at the same direction of the expected relation. Simultaneously, the models relative to the market value found no significance in the variable, suggesting that it is not an explanatory variable of market value. The EBITDA is a good indicator of operational efficiency, measuring the capacity of generating cash flow. Therefore, it makes sense to consider this value when buying and selling shares, generating higher returns to the shareholders when the EBITDA made public is higher.

The Revenue per Share –RePS– had statistical significance at a 1% level of confidence for all models, both in market value and in returns. These results are in accordance to the expectations as they were included in the model. It can be noted that the T-Test is quite above the 2.27 limit, suggesting an extremely low p-value, much lower than 1%, and that the variable contributes strongly for both models. These results show that net revenue contributes for the generation of market value and return on shares, meaning that the higher the revenue, the higher the value of the company and the positive returns from one period to the next.

Liquidity had no significance for the models with the dependent variable market value per Share (H1 – t test: - 0.78; H2 – t test: - 0.80; and H3 – t test: - 0.78), but it was expressively negative for the models related to returns per action (H2 – t test: - 10.50; H4 – t test: - 10.52; & H6 – t test: - 10.50). These results show that, for this study, liquidity does not explain market value, but the more liquid a company is, the more their actions have been negotiated in the market, and the lower their return on actions has been. Put in another way, there were less transactions involving the stocks of companies in the stock market, and they found better returns from one period to the other. This behavior is in accordance to what we expected.

The Brazilian GDP growth contributed statistically to form the market value of the company positively, showing a confidence level of 1% for models 1 and 3, and of 5% for model 5. However, it did not seem to contribute for the formation of returns in the same period. These results show that the value of the company follows the growth of the economy. That means that, when there is a general economic growth, companies show better returns, but when there is a period of economic decline, there are also negative impacts in the values of companies. However, the economic situation of the country in the period does not provoke significant oscillation in the returns on stocks. That can be because the market reacts to the future expectancies of the company. That can be understood as quite different from the current situation of the company, related to the economic situation of the country.

It was not possible to control the Industry for the models, since data showed adherence to the model of fixed effects, which does not accept dummy variables. However, we understand that many accounting and market values have specific behaviors with regards to Industry classification. To this end, we express a preoccupation for future work to consider the possibility of including this variable in studies, especially if data allows working with a model that includes random effects. Still, the use of fixed effects means that the work is more robust, making it possible to assure the relevance of accounting variables of interest. That means that our results allow us to strongly accept Hypotheses 1 and 5, showing that the market value of the company incorporates the NI and CI values made public in the period.

The general results of our models, given by the LSDV R-squared and by the standard error of the regression and the R2, presented for each model in table 5, show that the market gives a similar importance to each of our variables of interest (NIPS, OCIPS, and CIPS), since the values are relatively close among the models that have the same dependent variables. That means that the models (1, 3, and 5) that seek to explain the market value of the company have a value that is relatively close to 0.48 for the LSDV R-squared, to 0.04 for the standard regression error, and of 0.06 for the R2. Also, the models (2, 4, and 6) that seek to explain returns on company stocks have a value that is relatively close to 0.12 for LSDV R-squared, to 59.32 for standard regression error, and 0.02 for the R2. These results are not statistical coincidences, resulting from similar regression models, because all models use the same control variables and only one independent variable of interest is different between the models whose dependent variable is also the same.

Additionally, contrary to our expectations, we found that the interest variables, on occasion, offer opposite contributions for the Market Value and the Returns on Stocks. Associated to this discovery, we found that the there was a higher relevance for the models of Returns on Stocks (LSDV R-squared: 0.48) than for the Market Values (LSDV R-squared: 0.12), since only the dependent variable changed (between the models: 1 and 2; 3 and 4; and 5 and 6), because we work with the same sample. Since the model of fixed effects uses the least squares of the dummy variables, also named differential intercept dummies, and all other models used fixed effects with robust standard errors, it is natural that these values, which represent the explanatory powers of the same dependent variables, are relatively close. That helps us understand that the little variation among these values results from stability, especially between NI and CI, showing little variability of results from one model to the other.

Discussion of the results

As we did here, Wang et al. (2006) found evidence that the NI and the CI are valued due to their relevance on variable dependent stocks prices and their returns. However, the authors found a positive explanatory strength in both dependent variables, while in our case, data showed that the high NI and CI had a positive effect on the value of the company, but a negative one on the returns on stocks in the period. This result can be a consequence of the fact that investors perceived and disagreed with the level of subjectivity inherent to the changes in the international accounting standards, although the adoption of these standards had the positive intention of presenting the real situation of the company. This can lead investors to analyze other aspects that make them feel safer about the information made available, such as the use of independent audits from renowned companies. The study by Wang et al. (2006) considers a sample of companies from the Netherlands which, as in Brazil, had gone through a recent restructuring of accounting statements, which led to the adoption of Comprehensive Income Statements. However, the accounting legislation of the Netherlands had an important difference from the model that had been adopted in Brazil. Brazil went through severe changes, since it went from a legal form to the economic substance of the results. The Netherlands, on the other hand, already had an accounting system in which economic substance was over legal form, similarly to the models adopted in the United Kingdom and the United States.

The research by Wang et al. (2006) also shows that the CI has a stronger predictive force than the NI, since it is considered by investors to be the economic profit that is closer to reality. Although our results presented a significance level of 1% for both value models of the companies for these variables, the T-Test for the NI variable, in model 1, was a little higher (2.98) than the T-Test for the CI variable in model 5 (2.04). That could express the idea that the NI information may be slightly more relevant than CI information in Brazil. Once we perceived this and observed the corresponding LSDV R-squared value for each model, we found that model 1 stands out slightly above the corresponding value in model 5, reinforcing our intuition. Therefore, although international literature shows that, in other markets, the CI has a greater explanatory strength for the value of the company and return on stocks (Wang et al., 2006; Kanagaretnam et al., 2009). In Brazil the investors still lack this understanding. Maybe it will be possible to detect a better understanding of investors with regards to the informational value of these accounting variables after a longer period, once the changes are better accepted and applied. Kanagaretnam et al. (2009) also show that the OCI is a weak predictor of future profitability, and as such, should have a lower impact in the value of the company and the return on its stocks. It should be noted that these authors analyzed a sample made up of Canadian companies listed in the USA, suggesting the use of accounting that is targeted at the economic substance. Still, despite this considerable difference, we also found that the OCI information had lower importance in our study.

Final considerations

Our results showed that there was statistical significance between the independent variables of interest, the net profit, the OCI, and the CI with regards to the dependent variables Market Value and/or Returns on Stocks. However, some of the relations went in a direction opposite to the one expected. Therefore, our results allowed us to consider as true hypotheses 1 and 5 of our study, meaning that NI and CI contribute to explain the market value of a company. However, our statistical analyses allowed us to observe certain stability in the variables of interest, since we did not find great differences between the values of the general results of our models, found using the LSDV R-squared, the Standard Error of the regression, and the R2. This finding shows that the values that correspond to the accounting data are observed by the market, be it for the valuing of the company or for obtaining returns, but in a different way. Also, it was found that the market uses said information to confirm what was already expected since these values cannot provoke great variations in explanatory power between the models. As a result, we believe that this is the greatest contribution of this study, with regards to its possible economic interpretation.

Our research agrees with the existing literature on the relevance of value, according to which accounting information may predict other market information through Ohlson’s model (1995) and adaptations made from this important study. Previous researchers who use the model found evidence that accounting information is relevant in regards to its value, especially regarding stock price (Kanagaretnam et al., 2009; Alali & Foote 2012; Devalle & Magarini, 2012), stock returns (Kousenidis et al., 2009; Serrat et al., 2011), and cash flow (Wang et al., 2006; Goncharov & Hodgson 2011). However, few studies seek evidence on the market value as explained by CI (Serrat et al., 2011), OCI, and net profit. Furthermore, studies that investigate the impact of accounting variables, especially after the convergence to international accounting standards, are necessary in countries in which this convergence took place recently and in countries whose stock market is still relatively small. That is because the broader information offered by the new forms of accounting should be explored, and its relevance should be perceived by its users. Therefore, as we consider these elements and seek possible solutions, we will be able to contribute to the expansion of the market, so that its participants, companies, and investors have informational safety.

Acknowledgments

Financing: This work was carried out with the support of the Higher Level Personnel Improvement Coordination (CAPES) - Financing Code 001.

References

Acuña, B. C., Cruz, C. F., Oviedo, T. G., Salotti, B. M., & Martins, E. (2013). Impactos da Transição de Normas Contábeis sobre o lucro e o patrimônio líquido de Companhias Brasileiras Componentes do IBrX-100. Contabilidade, Gestão e Governança, 16(3), 138-154. https://www.revistacgg.org/contabil/article/view/617

Alali, F. A., & Foote, P. S. (2012). The Value Relevance of International Financial Reporting Standards: Empirical Evidence in an Emerging Market. The International Journal of Accounting, 47(1), 85-108. https://doi.org/10.1016/j.intacc.2011.12.005

Amihud, Y. (2002). Illiquidity and stock returns: cross-section and time-series effects. Journal of Financial Markets, 5(1), 31-56. https://doi.org/10.1016/S1386-4181(01)00024-6

Anandarajan, A., & Hasan, I. (2010). Value relevance of earnings: Evidence from Middle Eastern and North African Countries. Advances in Accounting, 26(2), 270-279. https://doi.org/10.1016/j.adiac.2010.08.007

Barth, M. E., Beaver, W. H., & Landsman, W. R. (2000). The Relevance of Value Relevance Research. Journal of Accounting and Economics, (650), 1-41. https://dx.doi.org/10.2139/ssrn.246861

Beisland, L. A. (2009). A Review of the Value Relevance Literature. The Open Business Journal, 2(1), 7-27. https://doi.org/10.2174/1874915100902010007

Biddle, G. C., & Choi, J.-H. (2006). Is Comprehensive Income Useful? Journal of Contemporary Accounting, & Economics, 2(1), 1-32. https://doi.org/10.1016/S1815-5669(10)70015-1

Black, B. S., Carvalho, A. G., & Sampaio, J. O. (2014). The evolution of corporate govenance in Brazil. Emerging Markets Review, 20, 17-195. https://doi.org/10.1016/j.ememar.2014.04.004

Clarkson, P., Hanna, J. D., Richardson, G. D., & Thompson, R. (2011). The impact of IFRS adoption on the value relevance of book value earnings. Journal of Contemporary Accounting, & Economics, 7(1), 1-17. https://doi.org/10.1016/j.jcae.2011.03.001

Da Costa, F. M., & Freitas, K. C. (2015). Escolhas contábeis na adoção inicial das normas internacionais de contabilidade no Brasil: direcionadores da aplicação do custo atribuído para ativos imobilizados. Revista Contabilidade Vista, & Revista, 25(3), 38-56. https://revistas.face.ufmg.br/index.php/contabilidadevistaerevista/article/view/2391

De Farias, J. B., Ponte, V. M. R., Oliveira, M. C., & De Luca, M. M. M. (2014). Impactos da adoção do IFRS nas demonstrações consolidadas dos bancos listados na BM&FBovespa. Revista Universo Contábil, 10(2), 63-83. https://doi.org/10.4270/RUC.2014212

Demir, E., & Ersan, O. (2017). Economic Policy uncertainty and cash holdings: Evidence from BRIC countries. Emerging Markets Review, 33, 189-200. https://doi.org/10.1016/j.ememar.2017.08.001

Devalle, A., & Magarini, R. (2012). Assessing the value relevance of total comprehensive income under IFRS: an empirical evidence from European stock exchanges. International Journal of Accounting, Auditing and Performance Evaluation, 8(1), 43-68. https://doi.org/10.1504/IJAAPE.2012.043965

Dhaliwal, D., Subramanyam, K. R., & Trezevant, R. (1999). Is comprehensive income superior to net income as a measure of firm performance? Journal of Accounting and Economics, 26(1-3), 43-67. https://doi.org/10.1016/S0165-4101(98)00033-0

Elshandidy, T. (2014). Value relevance of accounting information: Evidence from an emerging market. Advances in Accounting, 30(1), 176-186. https://doi.org/10.1016/j.adiac.2014.03.007

Filipin, R., Teixeira, S. A., Bezerra, F. A., & Da Cunha, P. R. (2012). Análise do nível de conservadorismo condicional das empresas brasileiras listadas na BM&FBOVESPA após a adoção do IFRS. Contabilidade e Controladoria, 4(2), 24-36. http://dx.doi.org/10.5380/rcc.v4i2.28041

Franzen, L., & Radhakrishnan, S. (2009). The value relevance of R&D across profit and loss firms. Journal Accounting and Public Policy, 28(1), 16-32. https://doi.org/10.1016/j.jaccpubpol.2008.11.006

Goncharov, I., & Hodgson, A. (2011). Measuring and Reporting Income in Europe. Journal of International Accounting Research, 10(1), 27-59. https://doi.org/10.2308/jiar.2011.10.1.27

Hair Jr, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2010). Multivariate Data Analysis, 6º ed. São Paulo: Ed. Pearson.

Hendriksen, E. S., & Van Breda, M. F. (1999). Teoria da contabilidade. São Paulo: Atlas.

Isaksson, L. E., & Woodside, A. G. (2016). Modeling firm heterogeneity in corporate social performance and financial performance. Journal of Business Research, 69(9), 3285-3314. https://doi.org/10.1016/j.jbusres.2016.02.021

Johnson, L. T., Reither C. L., & Swieringa, R. (1995). Toward reporting comprehensive income. American Accounting Association. Accounting Horizons, 9(4), 128-137. http://faculty.etsu.edu/pointer/johnson_1.pdf

Kanagaretnam, K., Mathieu, R., & Shehata, M. (2009). Usefulness of comprehensive income reporting in Canada. Journal of Accounting and Public Policy, 28(4), 349-365. https://doi.org/10.1016/j.jaccpubpol.2009.06.004

Kousenidis, D. V. Ladas, A. C., & Negakis, C. I. (2009). Value relevance of conservative and non-conservative accounting information. The International Journal of Accounting, 44(3), 219-238. https://doi.org/10.1016/j.intacc.2009.06.006

Lischewski, J., & Voronkova, S. (2012). Size, value and liquidity. Do They Really Matter on an Emerging Stock Market? Emerging Markets Review, 13(1), 8-25. https://doi.org/10.1016/j.ememar.2011.09.002

Mironiuc, M., Carp, M., & Chersan, E.-C. (2015). The relevance of financial reporting on the performance of quoted Romanian companies in the context of adopting the IFRS. Procedia Economics and Finance, 20, 404-413. https://doi.org/10.1016/S2212-5671(15)00090-8

Ohlson, J. A. (1995). Earnings, Book Values, and Dividends in Equity Valuation. Contemporary Accounting Research, 11(2), 661-687. https://doi.org/10.1111/j.1911-3846.1995.tb00461.x

Pamplona, J. B., & Cacciamali, M. C. (2017). O paradoxo da abundância: recursos naturais e desenvolvimento na América Latina. Estudos Avançados, 31(89), 251-270. https://dx.doi.org/10.1590/s0103-40142017.31890020

Rodrigues, L. L., Schmidt, P., & Dos Santos, J. L. (2012). The origins of modern accounting in Brazil: Influences leading to the adoption of IFRS. Research in Accounting Regulation, 24(1), 15-24. https://doi.org/10.1016/j.racreg.2011.12.003

Roggi, O., & Giannozzi, A. (2015). Fair value disclosure, liquidity and stock returns. Journal of Banking, & Finance, 58, 327-342. https://doi.org/10.1016/j.jbankfin.2015.04.011

Salotti, B. M., Murcia, F. D.-R., Carvalho, N., & Flores, E. (2015). IFRS no Brasil - Temas avançados abordados por meio de casos reais, 1º ed. São Paulo: Atlas.

Sampaio, R. B. Q., Lima, B. C. C., Cabral, A. C. A., & De Paula, A. L. B. (2014). A governança corporativa e o retorno das ações de empresas de controle familiar e de controle não familiar no Brasil. REGE – Revista de Gestão, 21(2), 219-234. https://doi.org/10.5700/rege527

Schaberl, P. D., & Victoravich, L. M. (2015). Reporting location and the value relevance of accounting information: The case of other comprehensive income. Advances in Accounting, 31(2), 239-246. https://doi.org/10.1016/j.adiac.2015.09.006

Serrat, N. A., Gutierrez, S. M., & Perez, G. R. (2011). Relevancia valorativa del resultado global y sus componentes frente al resultado neto. Revista de Contabilidad - Spanish Accounting Review, 14(2), 145-173. https://doi.org/10.1016/S1138-4891(11)70031-0

Skinner, D. J. (1999). How well does net income measure firm performance? A discussion of two studies. Journal of Accounting and Economics, 26(1-3), 105-111. https://doi.org/10.1016/S0165-4101(99)00005-1

Tsalavoutas, I., André, P., & Evans, L. (2012). The transition to IFRS and the value relevance of financial statements in Greece. The British Accounting Review, 44(4), 262-277. https://doi.org/10.1016/j.bar.2012.09.004

Veloso, G. G., & Malik, A. M. (2010). Análise do desempenho econômico-financeiro de empresas de saúde. RAE - eletrônica, 9(1). https://dx.doi.org/10.1590/S1676-56482010000100003

Yeh, I-C, & Hsu, T-K. (2014). Exploring the dynamics model of the returns from value stocks and growth stocks using time series mining. Expert Systems with Applications, 41(17), 7730-7743. https://dx.doi.org/10.1016/j.eswa.2014.06.036

Wang, Y., Buijink, W., & Eken, R. (2006). The value relevance of dirty surplus accounting flows in The Netherlands. The International Journal of Accounting, 41(4), 387-405. https://doi.org/10.1016/j.intacc.2006.09.005

Notes

*

Research paper.

Author notes

a Corresponding author. E-mail: cassianabortoli@gmail.com

Additional information

Cited as: Bortoli, C., Juaniha, A. M., Scarpin, J. E., Krespi M., N. T., & Edwards B., C. M. (2020). Value Relevance of net income, other comprehensive income, and comprehensive income in Brazil. Cuadernos de Contabilidad, 21. https://doi.org/10.11144/Javeriana.cc21.vrio