APA

ISO 690-2

Harvard

Haga clic en un formato de citación

Corporate Governance and Management Accounting to Reduce Agency Conflicts*

Gobernanza corporativa y contabilidad gerencial para reducir los conflictos de agencia

Governação empresarial e contabilidade de gestão para reduzir os conflitos de agência

Pedro Solana-González ![]() , Adolfo Alberto Vanti

, Adolfo Alberto Vanti ![]() , Sérgio de Iudícibus

, Sérgio de Iudícibus ![]()

Corporate Governance and Management Accounting to Reduce Agency Conflicts*

Cuadernos de Contabilidad, vol. 24, 2023

Pontificia Universidad Javeriana

Pedro Solana-González pedro.solana@unican.es

University of Cantabria, España

Adolfo Alberto Vanti adolfo.vanti@gmail.com

Universal Project Researcher, Brasil

Sérgio de Iudícibus siudicibus@pucsp.br

Pontifical Catholic University of São Paulo, Brasil

Received: 08 january 2021

Accepted: 13 june 2023

Abstract:

This paper aims to discover priority alternatives involved in decisional-making processes to reduce agency problems considering Corporate Governance (CG) and Management Accounting (MA) criteria. Using the Multi-Criteria Decision-Making (MCDM) methodology, it is possible to model the hierarchy structure to determine the ranking of decisional priorities using the Analytic Hierarchy Process (AHP) method. CG and MA are the main criteria for decision-making to reduce problems between ownership and capital control. Thus, engaging agents is the first alternative to reduce agency conflicts considering a general approach. Strategic accountability should be a priority to reduce agency problems focusing on CG and confidence is the main variable to consider from the MA standpoint. The research provides a multiple criteria system to reduce agency problems in decision-making. This work contributes to information asymmetry’s minimization and has implications on value preservation and creation for stakeholders. The decisional structure and the alternatives related to CG and MA have direct practical applications for managers and actors involved in business decisions to reduce agency conflicts. This paper provides evidence on the importance of CG and MA variables to reduce information asymmetry and agency problems and sets out the main priorities in a context of decision making for managers.

JEL codes: M1, D21

Keywords:corporate governance, management accounting, agency conflicts, multi-criteria decision making, analytic hierarchy process.

Resumen: Este trabajo tiene por objeto descubrir las alternativas prioritarias que intervienen en los procesos de toma de decisiones para reducir los problemas de agencia teniendo en cuenta los criterios de Gobernanza Corporativa (CG) y Contabilidad Gerencial (MA). Utilizando la metodología de Toma de Decisión Multicriterio (MCDM), es posible modelar la estructura jerárquica para determinar la clasificación de las prioridades de decisión utilizando el método del Proceso Analítico de Jerárquico (AHP). La CG y la MA son los principales criterios de toma de decisión para reducir los problemas entre la propiedad y el control del capital. Así pues, comprometer a los agentes es la primera alternativa para reducir los conflictos de agencia considerando un enfoque general. La rendición de cuentas estratégica debe ser una prioridad para reducir los problemas de agencia centrándose en la CG y la confianza es la principal variable para considerar desde el punto de vista de la MA. La investigación proporciona un sistema multicriterio para reducir los problemas de los organismos en la toma de decisiones. Este trabajo contribuye a la minimización de la asimetría de la información y tiene implicaciones en la preservación y creación de valor para las partes interesadas. La estructura decisoria y las alternativas relacionadas con la CG y la MA tienen aplicaciones prácticas directas para los gestores y los actores que participan en las decisiones empresariales para reducir los conflictos de agencia. Este artículo presenta pruebas de la importancia de las variables de CG y MA para reducir los problemas de asimetría de la información y de agencia, y establece las principales prioridades en un contexto de toma de decisiones para los gestores.

Palabras clave: gobernanza corporativa, contabilidad gerencial, conflictos de agencia, toma de decisión multicriterio, proceso analítico jerárquico.

Resumo: Este trabalho tem como objetivo descobrir alternativas prioritárias envolvidas em processos decisórios para reduzir problemas de agência, considerando critérios de Governança Corporativa (GC) e Contabilidade Gerencial (CG). Utilizando a metodologia Multi-Criteria Decision-Making (MCDM), é possível modelar a estrutura hierárquica para determinar o ranking de prioridades decisórias utilizando o método Analytic Hierarchy Process (AHP). A GC e a CG são os principais critérios de decisão para reduzir os problemas entre a propriedade e o controle do capital. Assim, o envolvimento dos agentes é a primeira alternativa para reduzir os conflitos de agência, considerando uma abordagem geral. A responsabilização estratégica deve ser uma prioridade para reduzir os problemas de agência, com foco na GC, enquanto a confiança é a principal variável a ser considerada do ponto de vista da CG. A investigação fornece um sistema de critérios múltiplos para reduzir os problemas de agência na tomada de decisões. Este trabalho contribui para a minimização da assimetria de informação e tem implicações na preservação e criação de valor para os stakeholders. A estrutura de decisão e as alternativas relacionadas à GC e à CG têm aplicações práticas diretas para os gestores e atores envolvidos nas decisões empresariais, visando a redução dos conflitos de agência. Este artigo fornece evidências sobre a importância das variáveis de GC e CG para reduzir a assimetria de informação e os problemas de agência. Apresenta as principais prioridades no contexto da tomada de decisões para os gestores.

Palavras-chave: governação empresarial, contabilidade de gestão, conflitos de agência, tomada de decisões com critérios múltiplos, processo analítico hierárquico.

Introduction

Organisational socio-economic growth has been characterised by management difficulties, mainly related to economics with separation of ownership and capital control (Morck & Steier, 2005). Such separation enables the inclusion of non-shareholders into organizations to help the expansion and the complexity of their activities. In this context, a wide and complex research field comes out and seeks to place the principal (capital owner) and the agent (which creates possessions on behalf of the principal) as the most important actors (Abdallah & Ismail, 2017; Garanina & Kaikova, 2016).

That movement to decision-making power has pointed out the improvements in the process to protect the rights of the concerned parties, in other words, advances in the corporate organizations’ governance system (Miglani, Ahmed & Henry, 2015; Saltaji, 2013). That happens because the utility functions of actors (principal and agent) are different and a natural information asymmetry will exist between them. Thus, the first actor will use an objective function that would tend to maximize its usefulness, at the expense of the second actor’s objective function. The principal does not manage to have access to the agent's informational model. Therefore, the information asymmetry exists. In that regard, Iudícibus (2015, p.73) emphasises that this issue can become an opportunity since it leads the accounting, including the management accounting, to large developments to better understand the stakeholders’ decision-making model of accounting and management information.

According to the document issued by CGMA (2014), “management accounting is at the heart of high-quality decision making because it brings to the fore the most relevant information and analysis to create and preserve value” (p. 3). It adds that management accounting by itself can’t resolve the entire range of issues that organizations face in response to information. However, it seeks to provide an organizational management approach that favours the development and execution of organizational strategy. High-quality decision-making has never been so important and/or so difficult since the volume and the speed of unstructured data are increasing the process complexity. Therefore, impulsive decisions often replace evidence-based ideas so far as organizations struggle to keep the rate of growth in their operation market.

In order to contribute to information asymmetry’s minimization between the actors and improve the decision-making process, the Multi-Criteria Decision Making (MCDM) method was used to model the hierarchy in smaller parts and structure the way of calculation using the Analytic Hierarchy Process (AHP). The AHP identifies the dominance of an element over other one (attributes, sub-attributes, and alternatives) in different hierarchic levels. To this effect, the priorities of initiatives such as those related to strategic accountability and operational accountability were visualized. In addition, management accounting was implemented in the decision-making process that reduces agency conflicts. The model was applied in a management case study of an Accounting Science course in a higher education institution. Above-mentioned application didn’t have any commercial purposes.

The contribution of this article consists in improving the decision-making process that reduces agency problems. To that end, the AHP method is used to model governance and management accounting. The research has created a multiple criteria system to reduce agency problems in decision-making that covers governance and management accounting factors. The existence of other important factors to reduce agency problems is highlighted. These factors can be observed and remain as suggestions for future research about the subject. These other factors are related to the analysis, for example, of information asymmetry.

The following pages present the review of literature that supports the empirical research, the methodological modelling, the instrument for collecting and analysing the results, the research application context, as well as the results analysis and the concluding remarks.

Literature Review

This literature review analyses some aspects related to agency conflicts and some ways to minimize them through governance, in the strategic structure and through management accounting, in the inner operational structure of the organization.

The agency theory focuses on the determination to have optimal contracts that control the relationship between principal and agent by mainly involving owners and senior management. Nevertheless, it doesn’t restrict itself to this organizational structure level (Eisenhardt, 1989). According to Boe, Gulbrandsen and Sorebo (2015, p. 376), agency theory is an omnipresent theory that has been implemented to several relationship types and explains transaction arrangements among parts with own interests, incongruous aims and uncertainty. Saam (2007, p. 826) remembers that agency theory has been implemented to the analysis of research fields as diverse as the company structure.

As reported by Eisenhardt (1988), agency theory’s goal is to explain the relationship between the principal, which delegates an activity, and the agent, which performs it on behalf of the principal. Such relationship was defined by Jensen and Meckling (1976, p. 310). In theory, the agency problem arises when the agent does not maximize the principal’s welfare, that is, it does not perform in the interest of the principal (Jensen & Meckling, 1976). Other writers, following the example of Eisenhardt (1989), Laffont & Martimort (2001), Saam (2007) and Linder and Foss (2013), understand that the agency problem’s origin is based upon conflicts of interest, risk aversion and information asymmetry between principal and agent.

Berle and Means (1932) previously broached the separation of ownership and control resulting from the change process in organizations because of capital search in the market. Almost simultaneously, Coase (1937) highlighted that the size of organizations varies as their transactions vary. To that end, the organizational structures need to be adjusted. According to Jensen and Meckling (1976) and Fama and Jensen (1983), those adjustments can result in delegation of power to agents, given the needed structure’s size, creating agency problems which arise from the separation of ownership and control.

In that regard, the agent will not always act in the interests of the principal since both actors maximize their own wealth. In other words, it is virtually impossible to ensure that the agent will make an optimal decision from the point of view of shareholders, since the perfect contract is not possible (Jensen & Meckling, 1976). Therefore, the principal is responsible for setting controls that minimize the agency costs by monitoring the agent’s behaviour and setting incentives, while trying to balance the interests through the corporate governance.

Corporate governance features the implementation of internal and external controls by means of mechanisms and principles that aim to minimize conflicts of interests between the agents, managers, and the principals, owners and shareholders of organizations (Jensen & Meckling, 1976; La Porta, Lopez-De-Silanes, Shleifer & Vishny, 2000; Morck, 2005). It also aims to protect the interests of other stakeholders by controlling the social contract compliance, acknowledged with the partnership in which organizations are involved (O'Donovan, 2002; Parmar et al., 2010; Suchman, 1995).

In order to minimize agency problems good governance practices are required, particularly in relation to internal controls related to organizations’ administration councils and to their managers (Garanina & Kaikova, 2016). Some of those good practices result in incentives to managers: structure and independence of councils and advisers, gender diversity in the councils, interaction between councils and risk management specialists from the organizations (Benkraiem, Hamrouni, Lakhal & Toumi, 2017; Hong, Li & Minor, 2016; Lozano, Martínez & Pindado, 2016; Mathew, Ibrahim & Archbold, 2018; Teti, Dell’acqua, Etro & Volpe, 2017; Titova, 2016; Xia & Beelde, 2018).

In addition, according to the agency theory, it is possible to state that the organizations’ economic performance is related to their control levels set by the governance. Organizations establish economic policies based on a suitable governance structure to meet the desired results (Akbar, Poletti-Hughes, El-Faitouri & Shah, 2016; Bhatt & Bhatt, 2017; Briano-Turrent & Rodríguez-Ariza, 2016; Funchal & Pinto, 2018; Shawtari, Salem, Hussain, Alaeddin & Thabi, 2016). On this point, besides the concern over councils and managers, controls regarding the organizations’ ownership structure are needed (Abdallah & Ismail, 2017; Ararat, Black & Yurtoglu, 2017; Ducassy & Guyot, 2017).

On the other hand, agency problems deepen because of the information asymmetry among the parties to a contract. The level of information is not the same among the parties because the agent is usually better informed than the principal. In other words, information asymmetry is a premise that makes the completeness of contracts impossible (Arrow, 1974; Stiglitz, 2000; Williamson, 1979). Recognizing the existence of information asymmetry changes the "mindset” of organizations and makes the introduction of controls possible, mainly over the agent in order to minimize the asymmetry.

Information asymmetry appears when an economic agent has more information than its counterpart and arises because of two main sources of agency problems, adverse selection and moral hazard (Arrow, 1985; Linder & Foss, 2013). Thus, adverse selection is related to hiding information or knowledge (ex-ante). Agents have information that is unknown to the principal (Eisenhardt, 1989). The agent makes observations that the principal cannot make and uses them in the decision-making process. However, the principal cannot verify if the agent has used his/her information the best way to meet his/her interests (Arrow, 1985, p.39).

Moral hazard is related to hiding actions (ex-post). In other words, the principal does not know the agents’ actions, or it is difficult to observe them because the agent can make observations that the principal cannot make since he/she is far from the process (Arrow, 1985). Saam (2007, p. 828) adds that the hidden action takes place after the agent’s recruitment as the agent can choose among different actions. He/she can choose to work less and pretend that he/she has worked more, since the principal cannot assess it easily. According to Segatto-Mendes (2001, p. 38), in moral hazard, the agent’s action, which is hidden to the principal, involves the agent’s effort and the principal cannot identify the level of actual effort applied to meet his/her interests.

The presence of asymmetric information among the parties in an economic transaction contributes to dishonesty. As maintained by Saam (2007, p. 827), information asymmetry arises because the principal cannot monitor the agent’s skills, purposes, information and actions, since they are hidden and can be monitored only with high costs. The principal and the agent’s utility functions are separable over time and information structures can change as time goes by, creating a natural information asymmetry between principal and agent (Laffont & Martimort, 2001).

Due to incomplete information, some people can obtain larger profits than others (Stiglitz, 2000). This situation can injure the organizational outcomes. Therefore, information asymmetry would lead to opportunistic behaviour that would create pressure from the stakeholders to reduce it. In that regard, the will or the need for reducing the information asymmetry goes through the organization’s communication to transparency and accountability, since there is a strong link between information disclosure and asymmetry reduction (Verrecchia, 2001; Xiao, Yang & Chow, 2004).

The disclosure’s role is to level out the information for the parties to a contract (Cunha, Frankenberger, Povoa & Silva, 2015; Stiglitz, 2000; Verrecchia, 2001). Thus, organizations must be transparent and account for their activities to their stakeholders in accordance with the standards. Especially to capital providers and those who legitimize the community where they are present (Albu & Girbina, 2015; Christensen, Kent, Routledge & Stewart, 2015; El-Diftar, Jones, Ragjeb & Soliman, 2017), and to other stakeholders interested in organizations, such as associates, customers, providers and government, considered as overriding groups (Mitchell, Agle, & Wood, 1997).

That way of thinking of organizations is related to a continuing decision-making process in which simplistic or dual methods cannot be used. They can only be used when the process gradually moves forward and considers the decision-makers’ subjectivity. In that regard, Management Accounting concurs with the corporate governance principles of transparency and accountability, by minimizing information asymmetry and by monitoring the agents’ behaviour, mainly because it is strongly directed to internal accountability.

The main goal of management accounting is to provide information for the internal decision-making, related to processes, people and investments, at planning and control stages (Lunkes, Schnorrenberger & Rosa, 2013). Weber (2011) highlights that the provision of information is not enough. It is necessary to interpret and advise managers with actions focused on spreading the understanding about organizational strategies. According to Weissenberger and Angelkort (2011), in order to contribute to organizational management it is necessary to take into consideration the form, comprehensibility and quality presented in financial and management information.

To Iudícibus (2015), management accounting involves few people, essentially the internal decision-makers of the organization. In addition, it is a strength of accounting for the decision-making processes in the short term, which gets closer to costs, to computer science, to operations management, to efficiency and effectiveness. Management accounting does not only exist as a structured administrative body. It must be also considered as an area of knowledge which justifies the execution of diverse planning and control activities in an organization (Cavalcante, Luca, Ponte & Gallon, 2012). According to Cinquini and Mitchell (2005) a profile of evidence is the most appropriate basis on which to make success judgements about management accounting.

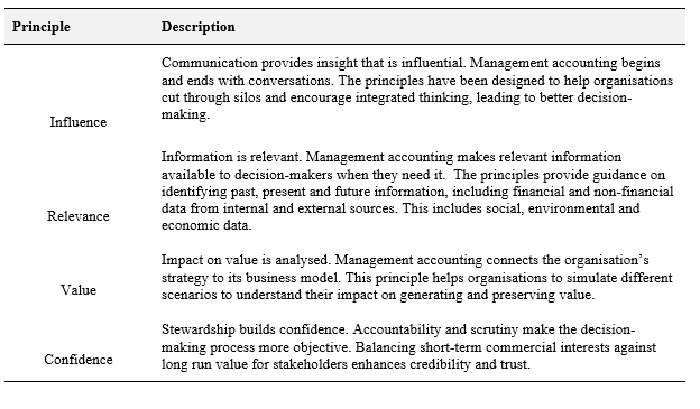

Management accounting has four global principles, shown in Table 1, that are understood as guides for good practices that reflect the perspectives of academics and professionals (CGMA, 2014).

The principles are intended to be universally applicable to help organisations large and small, public and private to extract value from the increasing volume of available information (CGMA, 2014). One of the tasks of management accounting is improving decision-making process in organizations. This is because people communicate to every decision-maker in the organization their relevant ideas and analyses, while being alert to the organization’s social and environmental duties. Management accounting influences the company’s strategic decisions, operating directly or indirectly at the management process stages supported by a synergistic information system. It assumes a systemic view of the organization about information requests (Cavalcante et al., 2012), considering, according to Warren, Reeve and Fess (2008), historical and estimated data used in conducting daily operations, planning of future operations and developing integrated business strategies (Warren et al., 2008).

Lunkes et al. (2013) emphasize that a good performance in accounting information does not only depend on relevance, accuracy and technique, but also on consistency towards the user’s point of view. A large amount of information, rather than being positive, can be debilitating for an organization, since it can lead to decision paralysis or to rash action. Available information has never been more plentiful, complex, unstructured or more difficult to interpret (CGMA, 2014). Therefore, defining the planning and control processes of organizational information becomes relevant.

Planning and control processes are equivalent to a system that allows all management levels to integrate functional and operational aspects with measures created by those responsible for its execution. It must also include the appropriate control stages (Lunkes et al., 2013). According to Fonseca (2007), goals and policies are chosen at a strategic level and they are considered as inputs to control process. They serve as controllers and enablers to the other hierarchic levels with the creation of mechanisms that level out the expenditure of resources.

In addition, according to Anthony and Govindarajan (2008), a management control system is the result of a conscious planning process that represents the actions that the organization must undertake, as well as the amount of resources to be hired. This system allows a comparison between defined and accomplished goals. Management accounting actively participates in the process of planning and control of companies by giving access to information that justifies their users’ actions (Cavalcante et. al., 2012).

Budgeting is an important and widely used planning and control tool for organizations. It represents a plan of action proposed by the management department for a specified period. It is understood as the process of allocating an organization’s financial resources to its activities (Uyar & Bilgin, 2011). Budgeting coverage begins with the development of the organization’s strategic planning and finishes with the definition of the activities needed for its application. It creates a plan of goals and resources that guide its implementation by aiming to analyse the variances and to implement adaptation measures (Lunkes et al., 2013).

Anthony and Govindarajan (2008) propose four stages for its development, namely, i) adjusting the strategic planning, ii) helping to coordinate the different parts of the organization, iii) assigning responsibilities and iv) obtaining the engagement of the agents involved. The provision of strategic information contributes to the users’ management process. It is important to remember that budget and management accounting should use the same terminology system to compare the prediction and the accomplishment.

Methodology

Analytic Hierarchy Process (AHP) is a Multi-Criteria Decision Making (MCDM) methodology that defines a prioritization ranking among different attributes, sub-attributes and alternatives (initiatives) that communicate with each other as it happens in localization problems or selection of logistic providers (Bianchini, 2018). Therefore, it reduces organizational complexity by allowing the manager to make management accounting decisions that ensure the accomplishment of corporate governance principles. This way, agency conflicts are reduced, and the impact of each hierarchy element is measured.

The AHP method is structured in six different steps (Saaty, 1980) and it allows to break down and reduce criteria relationships to achieve prioritizations of all the variables involved in the model. This happens by mixing different levels of hierarchies until the general goal is reached, thanks to different weights that work to reach it. Thus, peer-to-peer comparison arrays are established with validations that involve the Consistency Index, Consistency Ratio and Random Consistency Index to carry out sensitivity analyses.

The most cited creator and author of this method is Prof. Saaty whose works (Saaty, 1980; Saaty & Vargas, 2001) made their mark in the whole AHP trajectory; ranging from the first applications of military planning and transports to current investments in technology and projects under uncertainty. This method has been combined with other ones to further increase the strength and intangibilities that are part of complex decision-making processes, especially in aspects related to converting verbal scale to numerical scale. The AHP combines well with fuzzy, statistics and even with Analytic Network Process (ANP), developed by Prof. Saaty’s team.

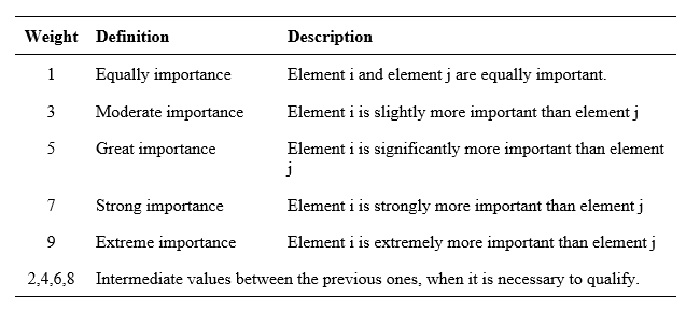

The steps recommended by Saaty (1980) for the application of this method are: define the problem and its specific goals or attributes in a hierarchic process; identify the criteria to achieve the sub-goals or sub-attributes related to the main goal; make peer-to-peer comparisons of the decision elements by creating comparison arrays that set peer-to-peer importance’s until reaching the alternative level; check the consistency characteristics of the completed arrays (recommended below 0.1); calculate the weights for each decision element and evaluate the alternatives based on the weights of decision elements. It can be completed with an “assessment” analysis by linking, for example, costs to each alternative.

The importance of the elements is measured according to the table below.

Table 2, using the 1-9 scale, defines well the data input with the AHP method and it can set the importance judgement between two elements (attributes, sub-attributes and alternatives). Thus, the less important element in each peer-to-peer comparison is defined as inverse from the integer value of the more important elements (reciprocal value in the array position).

AHP works well with intangible variables that, it can be said, are common in the context of corporate governance and agency theory. Therefore, by a peer-to-peer comparison between elements (attributes, sub-attributes and alternatives) it is possible to define decision weights that lead to better knowledge and a better alternative in order to decide (psychological judgement of seven positions of difference with variability points). Additionally, it is necessary to measure the inconsistency of answers in the peer-to-peer comparison and to ensure the judgement stability.

The research was developed with the participation of 3 experts in accounting and corporate governance. The evaluation of the model elements was provided by the experts by means of consistent judgements and paired comparisons that were validated through a process of discussion and consensus.

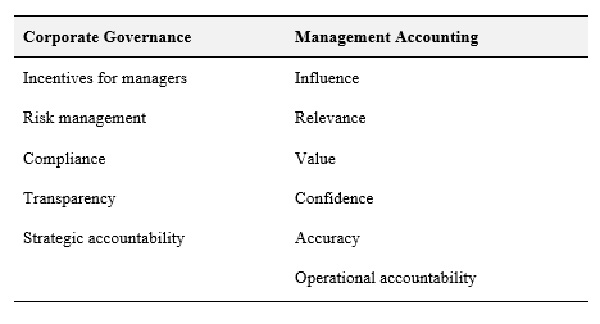

The data collection instrument considers the Management Accounting and Corporate Governance principles. They are defined bellow in the Table 3.

Table 3 refers to the attributes of Agency Theory, Corporate Governance and Management Accounting that were grouped to reduce the conflict between owner and agent. The model does not include Influence because it is an attribute of extreme intangibility. Influence is constituted by key ideas, dialogues, overcoming barriers between its units and encouraging integrated thinking that leads to a better decision making, which was virtually impossible to make the interviewed understand it. Nevertheless, all these characterizations were included when mapping the other attributes (Influence, Relevance, Value, Confidence, Accuracy and Operational accountability).

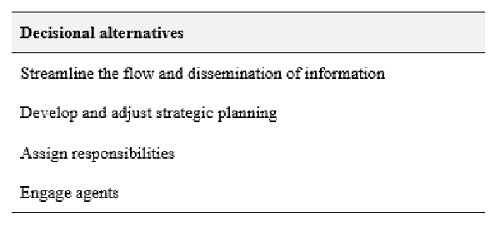

The alternatives related to each sub-attribute of Corporate Governance and Management Accounting, also in the context of planning/control and budgeting, are presented in the Table 4.

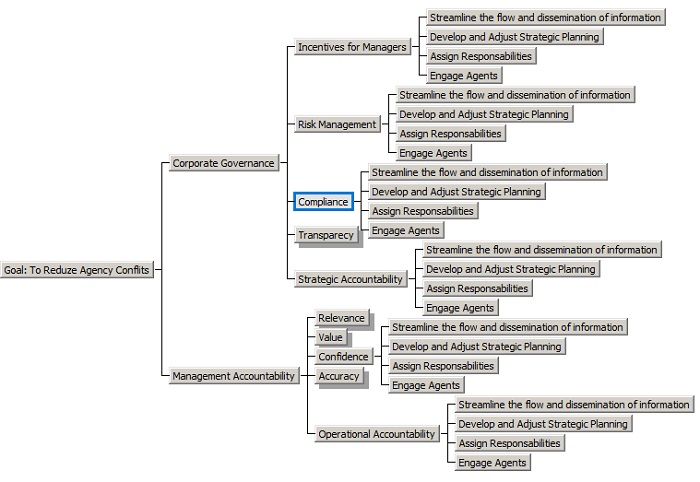

Figure 1 shows hierarchically all theoretical-logical structuring between the goal of reducing agency conflicts and the attributes of corporate governance and management accounting, as well as the respective alternatives. Even if the alternatives are linked to the highest hierarchic level, in other words, corporate governance and management accounting, they also link calculations and compare each attribute and sub-attribute peer-to-peer. The hierarchy and the different comparison matrices were created with the academic version of Expert Choice, a software that creates a decision-making support system to hierarchize and define priorities.

All the hierarchy converges to achieve the main goal, which is reducing agency conflicts without losing coherence among attributes, sub-attributes and alternatives. By creating different data input arrays and interviewing one or more managers, it is possible to complete the peer-to-peer comparisons.

Instrument for data collection and analysis

The data analysis instrument was implemented via AHP approach and Expert Choice software. For structuring the method an implementation for a given time was used by considering:

- The priorities.

- The peer-to-peer structures.

- The comparison inconsistencies that should be within the method suggested limits.

In this sense, it should be noted that the application advanced in an adequate Consistency Index (CI) <0.1 since each time the inconsistency was different, above 0.1, the research was stopped and the filling in of the peer-to-peer comparison data was re-analysed.

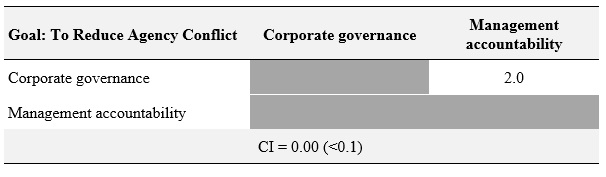

The main array of comparison between attributes, in other words, Corporate Governance versus Management Accounting is presented below with a 2x2 array. This main array of data input, as shown in Table 5, structures the highest and closest level to the main goal of reducing agency conflicts.

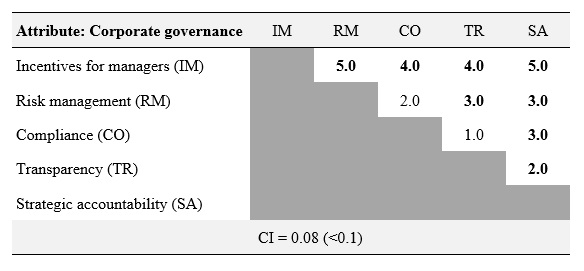

Table 6 is presented below like a 5x5 array that reflects the Corporate Governance approach and involves the sub-attributes of Incentives, Risk Management, Compliance, Transparency, and Strategic Accountability.

The crossing between Incentives for Managers and Risk Management is highlighted in the array above.

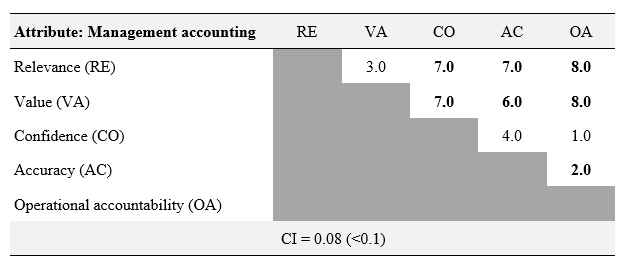

The data input array related to the Management Accounting attribute considers the sub-attributes comparisons, namely, relevance, value, confidence, accuracy and operational accountability. In Table 7 the peer-to-peer comparison and the crossing attributes can be seen.

The data input array of the MA attribute is presented with the respective peer-to-peer crossings and it highlights the intersection between relevance and value.

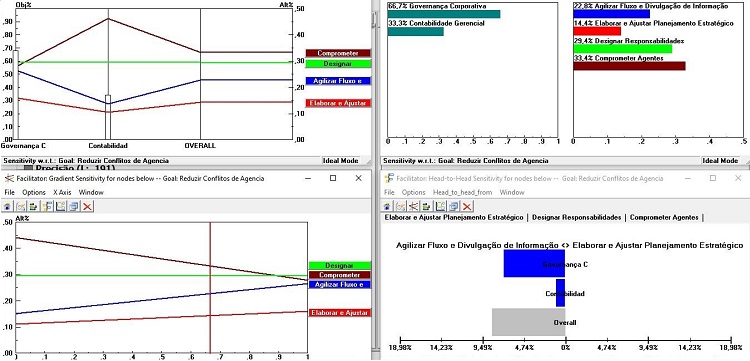

Additionally, it was possible to make analyses with the support of the sensitivity graphs: dynamic, performance, gradient, head-to-head and 2D that make it much easier to understand the priority ranking of all the variables. That is, the attributes, sub-attributes and especially the alternatives which have the main role in the decision-making process for reducing agency problems.

Results Analysis

Once data arrays were presented and data collected, the prioritizations found, including the ones of each alternative, are presented below in a synthetic way due to the number of graphs that have been created. The calculation of each array followed the adjustments recommended by the AHP methodology.

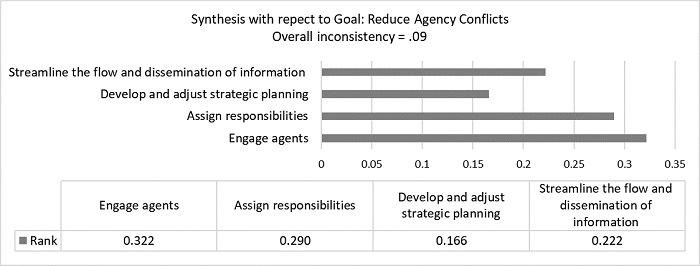

Figure 2 presents the ranking of alternatives to reduce the agency conflict general approach, in other words, it considers the corporate governance and management accounting. Therefore, Engage agents is the first alternative in the ranking with 0.322 followed by the assignment of responsibilities as a second alternative with 0.222.

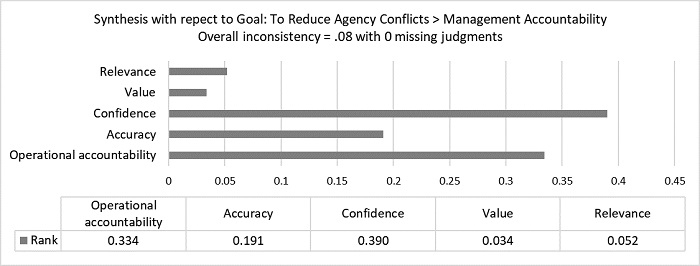

The ranking of alternatives to reduce the agency conflict focusing on management accounting is shown in Figure 3. Thus, Confidence is the first alternative in the ranking with 0.390, followed by issues affecting Operational accountability.

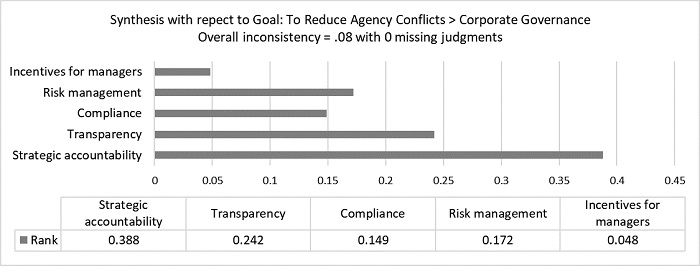

Figure 4 presents the ranking of alternatives to reduce the agency conflict focusing on corporate governance. Therefore, Strategic accountability is the first alternative in the ranking with 0.388, followed by the alternative of improving Transparency with a much lower priority, with 0.242.

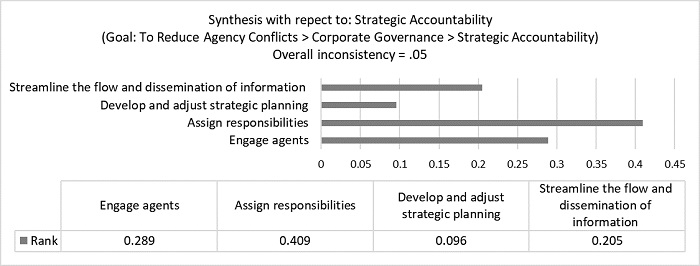

In addition, focusing on strategic accountability, the ranking of alternatives to reduce the agency conflict is show in Figure 5, reflecting that Assign responsibilities with 0.409 it would be the most outstanding alternative with quite a difference with respect to the others.

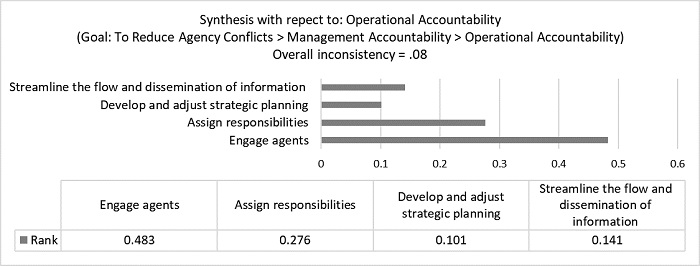

With respect to operational accountability, the Engage agents is the first alternative in the ranking with 0.483 (as is shown in Figure 6) and to a minor extend the alternative regarding the appropriate Assignment of responsibilities with 0.276.

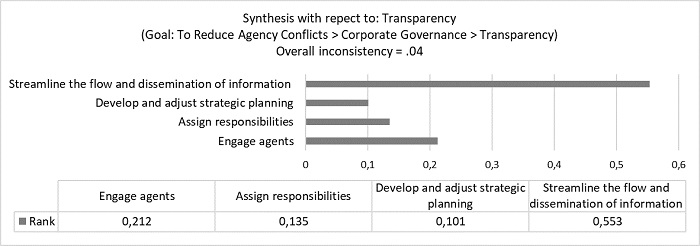

Focusing on transparency sub-attribute, Streamline the flow and dissemination of information is the first alternative in the ranking with 0.553 (as shown in Figure 7) being the difference with the rest of alternatives highly significant.

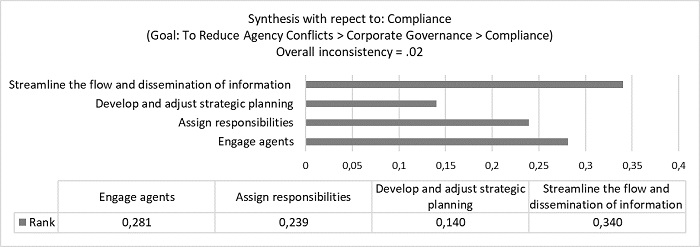

Figure 8 presents the ranking of alternatives to reduce agency conflict focusing on compliance. Thus, Streamline the flow and dissemination of information is also the first alternative in the ranking with 0.340 disputing the priority with the alternative relating to Engage agents with 0.281.

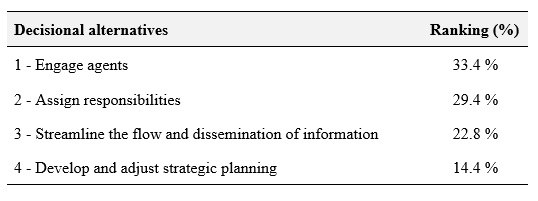

Finally, the grouped alternatives allowed us to visualize the ranking or the prioritization so that decisions can be made in a more coherent way, considering the complex multicriteria situations. For that purpose, the following results were obtained:

The following graphs, developed by using performance analysis and sensitivity analysis, are presented in the Figure 9 as a general consolidation.

Conclusions

The multicriteria decision making in CG and MA that reduces problems between ownership and capital control has been developed in this work by defining the priorities in different alternatives. These alternatives are related to: 1) streamlining the flow and dissemination of information, 2) developing and adjusting the strategic planning, 3) assigning responsibilities, and 4) engaging agents.

This paper provides evidence on the importance of CG and MA variables to reduce agency problems and determines the main priorities in a context of decision making for managers. This work also contributes to information asymmetry’s minimization and has implications on value creation and preservation for stakeholders.

Additionally, a comprehensive hierarchical structure of criteria, sub-criteria and decisional alternatives is used. Thus, by using the Multi-Criteria Decision-Making methodology it was possible to model the hierarchy in smaller parts and structure the way of calculation using the AHP.

The findings evidence that CG and MA are the main criteria for decision-making to reduce problems between ownership and capital control. Strategic Accountability should be a priority to reduce agency problems focusing on CG, with confidence being the main variable to consider from the MA viewpoint. Furthermore, engaging agents should be the first decisional alternative to reduce agency conflicts considering a general approach.

The decisional hierarchy structure and the ranking of priorities discovered related to CG and MA have direct practical applications for managers and actors involved in business decisions to reduce agency conflicts. This work is interesting as management case study of corporate governance and accounting science for Higher Education Institutions.

The complexity and specificity of the problem discussed make it necessary to carry out further research in this field through studies that expand the size and heterogeneity of the expert panel and the application of new decision-making methods together with other research techniques.

Therefore, it is possible to simulate investment variations in any of the attributes and to verify how the other attributes and alternatives behave. However, this work does not include this simulation or sensitivity analysis and it implements investments since these aspects are more suitable for a specific case, preserving the appropriate confidentiality. In future works it could be possible to present results related to financial aspects.

Finally, it should be highlighted the fact that CG and MA is at the heart of high-quality decision making to create and preserve value. This kind of decision works well with the volume and speed of unstructured data in complex processes. The research has created a multiple criteria system to reduce agency problems in decision-making that covers governance and management accounting factors. Other important factors to reduce agency problems can be observed and remain as suggestions for future research about the subject. These other factors are related to the specific analysis of information asymmetry problems.

References

Abdallah, A.A., & Ismail, A.K. (2017). Corporate governance practices, ownership structure, and corporate performance in the GCC countries. Journal of International Financial Markets, Institutions and Money, 46, pp. 98-115. https://doi.org/10.1016/j.intfin.2016.08.004

Akbar, S., Poletti-Hughes, J., El-Faitouri, R., & Shah, S.Z. (2016). More on the relationship between corporate governance and firm performance in the UK: Evidence from the application of generalized method of moments estimation. Research in International Business and Finance, 38, pp. 417-429. https://doi.org/10.1016/j.ribaf.2016.03.009

Albu, C.N., & Girbina, M.M. (2015). Compliance with corporate governance codes in emerging economies. How do Romanian listed companies “comply-or-explain”?. Corporate Governance: The International Journal of Business in Society, 15(1), pp. 85-107. https://doi.org/10.1108/CG-07-2013-0095

Anthony, R.N., & Govindarajan, V. (2008). Sistemas de Controle Gerencial. Mc Graw Hill.

Ararat, M., Black, B.S., & Yurtoglu, B.B. (2017). The effect of corporate governance on firm value and profitability: Time-series evidence from Turkey. Emerging Markets Review, 30, pp. 113-132. https://doi.org/10.1016/j.ememar.2016.10.001

Arrow, K.J. (1974). Limited knowledge and economic analysis. The American Economic Review, 64(1), pp. 1-10. https://www.jstor.org/stable/1814877

Arrow, K.J. (1985). The economics of agency, in Pratt, John W. and Zeckhauser, Richard J. (Eds.), Principals and agents. The structure of business. Harvard Business School Press, 37-51.

Benkraiem, R., Hamrouni, A., Lakhal, F., & Toumi, N. (2017). Board independence, gender diversity and CEO compensation. Corporate Governance: The International Journal of Business in Society, 17(5), pp. 845-860. https://doi.org/10.1108/CG-02-2017-0027

Berle, A.A., & Means, G.C. (1932). The modern corporation and private property. Macmillan.

Bhatt, P.R., & Bhatt, R.R. (2017). Corporate governance and firm performance in Malaysia. Corporate Governance: The International Journal of Business in Society, 17(5), pp. 896-912. https://doi.org/10.1108/CG-03-2016-0054

Bianchini, A. (2018). 3PL provider selection by AHP and TOPSIS methodology. Benchmarking: An International Journal, 25(1), pp. 235-252. https://doi.org/10.1108/BIJ-08-2016-0125

Boe, T., Gulbrandsen, B., & Sorebo, O. (2015). How to stimulate the continued use of ICT in higher education: Integrating information systems continuance theory and agency theory. Computers in Human Behavior, 50, pp. 375-384. https://doi.org/10.1016/j.chb.2015.03.084

Briano-Turrent, G.D., & Rodríguez-Ariza, L.R. (2016). Corporate governance ratings on listed companies: An institutional perspective in Latin America. European Journal of Management and Business Economics, 25(2), pp. 63-75. https://doi.org/10.1016/j.redeen.2016.01.001

Cavalcante, D.S., Luca, M.M., Ponte, V.M., & Gallon, A.V. (2012). Características da controladoria nas maiores companhias listadas na BM&FBOVESPA. Revista Universo Contábil, 8(3), pp. 113-134. https://bu.furb.br/ojs/index.php/universocontabil/article/view/2492

CGMA (2014). Global management accounting principles: Improving decisions and building successful organizations. Chartered Global Management Accountant.

Cinquini, L., & Mitchell, F. (2005). Success in management accounting: Lessons from the activity‐based costing/management experience. Journal of Accounting & Organizational Change, 1(1), pp. 63-77. https://doi.org/10.1108/18325910510635290

Coase, R.H. (1937). The nature of the firm. Economica, 4(16), pp. 386-405. https://doi.org/10.1111/j.1468-0335.1937.tb00002.x

Christensen, J., Kent, P., Routledge, J., & Stewart, J. (2015). Do corporate governance recommendations improve the performance and accountability of small listed companies? Accounting and Finance, 55(1), pp. 133-164. https://doi.org/10.1111/acfi.12055

Cunha, J., Frankenberger, F., Povoa, A., & Silva, W. (2015). Disclosure socioambiental e o impacto no custo de capital. Revista ADMpg Gestão Estratégica, 8(2), pp. 55-63.

Ducassy, I., & Guyot, A. (2017). Complex ownership structures, corporate governance and firm performance: The French context. Research in International Business and Finance, 39(A), pp. 291-306. https://doi.org/10.1016/j.ribaf.2016.07.019

Eisenhardt, K.M. (1989). Agency theory: An assessment and review. Academy of Management Review, 14(1), pp. 57-74. https://doi.org/10.5465/amr.1989.4279003

Eisenhardt, K.M. (1988). Agency-and institutional-theory explanations: The case of retail sales compensation. Academy of Management Journal, 31(3), pp. 488-511. https://www.jstor.org/stable/256457

El-Diftar, D., Jones, E., Ragjeb, M., & Soliman, M. (2017). Institutional investors and voluntary disclosure and transparency: The case of Egypt. Corporate Governance: The International Journal of Business in Society, 17(1), pp. 134-151. https://doi.org/10.1108/CG-05-2016-0112

Fama, E.F., & Jensen, M.C. (1983). Separation of ownership and control. Journal of Law and Economics, 26(2), pp. 301-325. https://doi.org/10.1086/467037

Fonseca, R.C. (2007). Como elaborar projetos de pesquisa e monografias: Guia Prático. Imprensa Oficial, Curitiba.

Funchal, B., & Pinto, J.P. (2018). Corporate events' performance and corporate governance: The Brazilian evidence. Corporate Governance: The International Journal of Business in Society, 18(1), pp. 14-34. https://doi.org/10.1108/CG-11-2016-0219

Garanina, T., & Kaikova, E. (2016). Corporate governance mechanisms and agency costs: Cross-country analysis. Corporate Governance: The International Journal of Business in Society, 16(2), pp. 347-360. https://doi.org/10.1108/CG-04-2015-0043

Hong, B., Li, Z., & Minor, D. (2016). Corporate governance and executive compensation for corporate social responsibility. Journal Business Ethics, 136(1), pp. 199-213. https://doi.org/10.1007%2Fs10551-015-2962-0

Iudícibus, S. (2015). Teoria da contabilidade. Atlas.

Jensen, M. C., & Meckling, W.H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), pp. 305-360. https://doi.org/10.1016/0304-405X(76)90026-X

La Porta, R., Lopez-De-Silanes, F., Shleifer, A., & Vishny, R. (2000). Investor protection and corporate governance. Journal of Financial Economics, 58(1-2), pp. 3-27. https://doi.org/10.1016/S0304-405X(00)00065-9

Laffont, J., & Martimort, D. (2001). The theory of incentives: The principal-agent model. Princeton University Press.

Linder, S., & Foss, N.J. (2013). Agency theory. SSRN eLibrary, 7, pp. 1-35. http://dx.doi.org/10.2139/ssrn.2255895

Lozano, M.B., Martínez, B., & Pindado, J. (2016). Corporate governance, ownership and firm value: Drivers of ownership as a good corporate governance mechanism. International Business Review, 25(6), pp. 1333-1343. https://doi.org/10.1016/j.ibusrev.2016.04.005

Lunkes, R.J., Schnorrenberger, D., & Rosa, F.S. (2013). Controllership functions: An analysis in the Brazilian scenario. Revista Brasileira de Gestão de Negócios, 15(47), pp. 283-299. https://doi.org/10.7819/rbgn.v15i47.1185

Mathew, S., Ibrahim, S., & Archbold, S. (2018). Corporate governance and firm risk. Corporate Governance: The international Journal of Business in Society, 18(1), pp. 52-67. https://doi.org/10.1108/CG-02-2017-0024

Miglani, S., Ahmed, K., & Henry, D. (2015). Voluntary corporate governance structure and financial distress: Evidence from Australia. Journal of Contemporary Accounting & Economics, 11(1), pp. 18-30. https://doi.org/10.1016/j.jcae.2014.12.005

Mitchell, R.K., Agle, B.R., & Wood, D.J. (1997). Toward a theory of stakeholder identification and salience: Defining the principle of who and what really counts. Academy of Management Review, 22(4), pp. 853-886. https://doi.org/10.5465/amr.1997.9711022105

Morck, R.K. (2005). A history of corporate governance around the world. University of Chicago Press.

Morck, R.K., & Steier, L. (2005). The global history of corporate governance: an introduction. National Bureau of Economic Research, Working Paper 11062, pp. 1-47. https://doi.org/10.3386/w11062

O'Donovan, G. (2002). Environmental disclosure in the annual report: Extending the applicability and predictive power of legitimacy theory. Accounting, Auditing, Accountability Journal, 15(3), pp. 344-371. https://doi.org/10.1108/09513570210435870

Parmar, B.L., Freeman, R.E., Harrison, J.S., Wicks, A.C., Purnell, L., & Colle, S. (2010). Stakeholder theory: The state of the art. The Academy of Management Annals, 4(1), pp. 403-445. https://doi.org/10.5465/19416520.2010.495581

Saltaji, I. Mf. (2013). Corporate governance and agency theory how to control agency costs. Internal Auditing and Risk Management, 32(1), pp. 51-64.

Saam, N.J. (2007). Asymmetry in information versus asymmetry in power: Implicit assumptions of agency theory? The Journal of Socio-Economics, 36(6), pp. 825-840. https://doi.org/10.1016/j.socec.2007.01.018

Saaty, T.L. (1980). The analytical hierarchy process: Planning, priority setting, resource allocation. Mc Graw-Hill.

Saaty, T.L., & Vargas, L.G. (2001). Models, methods, concepts & applications of the analytic hierarchy process. Kluwer Academic Publishers. https://doi.org/10.1007/978-1-4614-3597-6

Segatto-Mendes, A.P. (2001). Teoria de agência aplicada à análise de relações entre os participantes dos processos de cooperação tecnológica universidade-empresa. Doctoral Thesis, University of São Paulo.

Shawtari, F.A., Salem, M.A., Hussain, H.I., Alaeddin, O., & Thabi, O.B. (2016). Corporate governance characteristics and valuation: Inferences from quantile regression. Journal of Economics, Finance and Administrative Science, 21(41), pp. 81-88. https://doi.org/10.1016/j.jefas.2016.06.004

Stiglitz, J.E. (2000). The contributions of the economics of information to twentieth century economics. The Quarterly Journal of Economics, 115(4), pp. 1441-1478. https://doi.org/10.1162/003355300555015

Suchman, M.C. (1995). Managing legitimacy: Strategic and institutional approaches. Academy of Management Review, 20(3), pp. 571-610. https://doi.org/10.5465/amr.1995.9508080331

Teti, E., Dell’acqua, A., Etro, L., & Volpe, M. (2017). The impact of board independency, CEO duality and CEO fixed compensation on M&A performance. Corporate Governance: The International Journal of Business in Society, 17(5), pp. 947-971. https://doi.org/10.1108/CG-03-2017-0047

Titova, Y. (2016). Are board characteristics relevant for banking efficiency? Evidence from the US. Corporate Governance: The International Journal of Business in Society, 16(4), pp. 655-679. https://doi.org/10.1108/CG-09-2015-0124

Uyar A., & Bilgin, N. (2011). Budgeting practices in the Turkish hospitality industry: An exploratory survey in the Antalya region. International Journal of Hospitality Management, 30(2), pp. 398-408. https://doi.org/10.1016/j.ijhm.2010.07.011

Verrecchia, R.E. (2001). Essays on disclosure. Journal of Accounting and Economics, 32(1-3), pp. 97-180. https://doi.org/10.1016/S0165-4101(01)00025-8

Warren, C., Reeve, J., & Fess, P. (2008). Contabilidade gerencial. Thomson Learning.

Weber, J. (2011). The development of controller tasks: Explaining the nature of controllership and its changes. Journal of Management Control, 22, pp. 25-46. https://doi.org/10.1007/s00187-011-0123-x

Weissenberger, B.E., & Angelkort, H. (2011). Integration of financial and management accounting systems: The mediating influence of a consistent financial language on controllership effectiveness. Management Accounting Research, 22(3), pp. 160-180. https://doi.org/10.1016/j.mar.2011.03.003

Williamson, O.E. (1979). Transaction-cost economics: The governance of contractual relations. Journal of Law and Economics, 22(2), pp. 233-261. https://doi.org/10.1086/466942

Xia, B.S., & Beelde, I. (2018). Corporate governance and management incentives: Evidence from the Scandinavian countries. Corporate Governance: The International Journal of Business in Society, 18(1), pp. 1-13. https://doi.org/10.1108/CG-04-2017-0075

Xiao, J.Z., Yang, H., & Chow, C.W. (2004). The determinants and characteristics of voluntary internet-based disclosures by listed Chinese companies. Journal of Accounting and Public Policy, 23(3), pp. 191-225. https://doi.org/10.1016/j.jaccpubpol.2004.04.002

Notes

*

Artículo de investigación