APA

ISO 690-2

Harvard

Haga clic en un formato de citación

Are Voluntary Auditor Changes Relevant for the Brazilian Market? An Analysis Based on Return and Stock Trading Volume*

¿Son relevantes los cambios voluntarios de auditores para el mercado brasileño? Un análisis basado en el rendimiento y el volumen de negociación de acciones

As mudanças voluntárias de auditores são relevantes para o mercado brasileiro? Uma análise baseada no desempenho das ações e no volume de negociação

Anderson Monteiro de Andrade ![]() , Adolfo Henrique Coutinho e Silva

, Adolfo Henrique Coutinho e Silva ![]() , Moacir Sancovschi

, Moacir Sancovschi ![]()

Are Voluntary Auditor Changes Relevant for the Brazilian Market? An Analysis Based on Return and Stock Trading Volume*

Cuadernos de Contabilidad, vol. 24, 2023

Pontificia Universidad Javeriana

Anderson Monteiro de Andrade anderson.monteiro.andrade@gmail.com

Federal University of Rio de Janeiro, Brasil

Adolfo Henrique Coutinho e Silva adolfocoutinho@uol.com.br

Federal University of Rio de Janeiro, Brasil

Moacir Sancovschi msancov@facc.ufrj.br

Federal University of Rio de Janeiro, Brasil

Received: 22 october 2022

Accepted: 14 march 2023

Abstract:

This paper explores the market and investor reaction to the announcement of Voluntary Auditors’ Changes (VACs) of Brazilian public companies between 2012 and 2019. To this end, the event study method was applied on return and stock trading volume against a sample of 80 VACs carried out by 66 companies. The main sample was also segregated into subsamples according to the audit size and opinion issued by the replaced auditor. The results indicate that, in general, there is no market nor investors' reaction to the VACs’ announcement. In addition, we identified that many Brazilian companies did not disclose their reasons for the VACs or gave vague justifications. This finding is relevant because it shows that institutional settings which have mandatory auditor changes in short periods, like Brazil, may reduce the surprise effect of the disclosure of VACs. This fact added to the opacity of auditor changes reasons consequently would minimize VAC relevance to the market.

JEL codes: G12; G14; M42; N26.

Keywords:voluntary auditor change, market reaction, investors’ reaction, event study.

Resumen: Este trabajo explora la reacción del mercado y de los inversores al anuncio de Cambios Voluntarios de Auditores (CVAs) para las empresas públicas brasileñas entre 2012 y 2019. Para ello, se aplicó el método de estudio de eventos sobre rentabilidad y volumen de negociación de acciones, frente a una muestra de 80 CVAs realizados por 66 empresas. La muestra principal también se separó en submuestras de acuerdo con el tamaño de la auditoría y la opinión emitida por el auditor reemplazado. Los resultados indican que, en general, no hay reacción del mercado ni de los inversores al anuncio de los CVAs. Además, identificamos que muchas empresas brasileñas no revelaron las razones de los CVAs o dieron razones genéricas. Este hallazgo es importante porque muestra que los entornos institucionales que tienen cambios obligatorios de auditor en períodos cortos, como Brasil, pueden reducir el efecto sorpresa de la divulgación de los CVAs. Este hecho, sumado a la opacidad de los cambios del auditor, minimizaría la relevancia del CVAs para el mercado.

Palabras clave: Cambios Voluntarios de Auditores (CVA), reacción del mercado, reacción del inversor, estudio de eventos.

Resumo: Este artigo explora a reação do mercado e dos investidores ao anúncio das Mudanças Voluntárias de Auditores (VAC) em empresas brasileiras de capital aberto entre 2012 e 2019. Para isso, o método de estudo de eventos foi aplicado ao desempenho e ao volume de negociação das ações de uma amostra de 80 VACs realizadas por 66 empresas. A amostra principal também foi dividida em subamostras de acordo com o tamanho da auditoria e o parecer emitido pelo auditor substituído. Os resultados indicam que, em geral, não há reação do mercado ou dos investidores ao anúncio de VACs. Além disso, identificou-se que muitas empresas brasileiras não divulgaram as razões para as VACs ou apresentaram justificativas vagas. Esse achado é relevante porque mostra que regulamentações institucionais que exigem mudanças de auditor em períodos curtos, como no Brasil, podem reduzir o efeito surpresa do anúncio de VAC. Isso, aliado à opacidade das razões para a mudança de auditor, consequentemente minimizaria a relevância dos VACs para o mercado.

Palavras-chave: mudança voluntária de auditor, reação do mercado, reação do investidor, estudo de evento.

1. Introduction

The external audit service is fundamental to the capital market efficiency and the independence of the audit firm concerning their client is a crucial factor in the quality of the audit service (DeAngelo, 1981). Several accounting scandals in large public companies in recent decades have sparked a great discussion about the independence of audit firms and has triggered the implementation of distinct systems of mandatory auditor rotation around the world (DeFond & Francis, 2005; Cameran, Prencipe & Trombetta, 2014; Bronson, Harris & Whisenant, 2016). In Brazil, the USA and the European Union, for example, the mandatory auditor rotation standards are significantly different as we explain in detail in section 2.

Beyond that, public companies also make Voluntary Auditors’ Changes (VAC) that may arise from the initiative of the audit firm (resignations) or the company’s own initiative (dismissals). In both cases, VAC’s announcements are not expected by the market. Notably, the reasons for carrying out a VACs are different from the mandatory auditor rotation, but both impact the auditors-client relationship.

Previous studies show that a VAC can influence the markets’ and investors’ perception, impacting the return and the trading volume of the shares. For example, some studies show that the market may react negatively when there is a voluntary change from a BigN audit firm to a non-BigN firm, when the replaced audit firm issued a modified auditor’s opinion or when an auditors’ resignation occurs (Dunn, Hillier & Marshall 1999; Whisenant, Sankaraguruswamy & Raghunandan 2003; Knechel, Naiker & Pacheco 2007). In addition to that, VACs can also impact the trading volume of shares, which portrays the individual investor reaction (Beaver, 1968).

However, previous studies on market reaction (abnormal returns) for VAC’s announcement showed inconclusive results (Schneider, 2015, p. 40). Besides, few studies have analyzed the effect of voluntary changes on the trading volume. (Hagigi, Kluger & Shields, 1993). Thus, the main motivation for this study stems from the fact that little is known about the relevance of the phenomenon of voluntary change of audit firms to the capital market, reflected by stock returns and its respective effects on investor behavior, measured by stock volume. A second motivation arises from a practical perspective, considering that recent changes in European Union regulation about auditor changes bring more demand for understanding market behavior in an environment with mandatory audit firm change, especially when voluntary auditor changes are allowed. Our findings may be helpful for the European regulator in realizing future VAC effects on the capital market, in a scenario in which public companies have already begin to compulsorily rotate audit firms. Furthermore, just a few studies examine the importance of this phenomenon in a context different from that observed in the United States. The results may be quite different in countries with different mandatory auditor rotation rules, as observed in developing countries.

Examining capital market reactions to VACs in an emerging country like Brazil is important for two main reasons. Firstly, there is a lack of empirical evidence on the effect of VACs on market reaction in Brazil, where dual mandatory auditor rotation rule has been held for over 20 years. Although the Brazilian environment is conducive to research focused on audit changes due to its regulatory development, more recent studies have examined the relationship between the regulation of auditor changes and earnings management as an indicator of earnings quality (Silvestre, Costa & Kronbauer, 2018; Parreira et al. 2021). Secondly, prior studies in this area were mostly conducted in non-mandatory settings (Schiff, 1981; Smith, 1988; Johnson & Lys, 1990; Klock, 1994; Schwartz & Soo, 1996; Griffin & Lont, 2010; Chang, Cheng & Reichelt, 2010). Audit firm switching entails certain costs that are borne by both the client and the firm (Cameran, Negri & Pettinnicchio, 2015), so that a voluntary change would bring additional costs in the medium term in an environment where there are mandatory auditor changes. Thus, incurring in additional costs to change auditors voluntarily can be seen as a red flag for investors, not only for impairing integrity but also for reflecting low managerial efficiency (Hossain, Mitra & Rezaee, 2014).

In this context, our objective is to assess the impact of the VAC’s announcement on the abnormal return and abnormal trading volume of the shares of Brazilian public companies from 2012 to 2019. Our analysis also includes subsamples tests for change in auditors’ size and the different types of auditor’s opinion issued by the replaced audit firm.

Our results indicate that there is neither market nor investors’ reaction to the announcement of the VAC for public companies in Brazil, even when it entails a change in the auditors’ size or when the replaced audit firm issued a modified opinion. The qualitative analysis demonstrates that several Brazilian companies had made both voluntary auditor changes and mandatory auditor rotations. We identified 1.92 auditors’ changes per company and 1.29 VACs per company in eight years. The audit contract duration with VAC is 3.1 years, while the Brazilian mandatory auditor rotation occurs, in general, every five years. In addition, we can observe that 34 companies (42.5% events) did not disclose the reasons for the VACs or disclosed vague ones.

In summary, our evidence allows us to conclude that Brazilian investors do not perceive changes in the quality of auditors’ services when there is a VAC. The possible explanations for this result can be the high frequency of VACs, the short period to the mandatory audit rotation applied in Brazil and the low degree of transparency about the reasons presented by the companies for voluntary switch the audit firms. These aspects may increase the opacity of this phenomenon for Brazilian investors in general.

Our results are relevant for several reasons. Firstly, they analyzed the market reaction and investor reaction to the VACs’ announcement in an important developing country with different rules for audit changes, such as dual mandatory auditor rotation rule, which can bring different perception about audit quality (Horton, Livne, & Pettinicchio, 2021). Secondly, our study provides evidence about the trading volume associated with VACs in the Brazilian context. In addition, our findings contribute to the literature by providing evidence that even when there is a comprehensive regulation mandating the disclosure of reasons for all types of auditor changes, there is no guarantee that the market will react to voluntary audit switching. So, when analyzing stock returns and volume, it is possible to state that both the market as a whole and the individual investor anticipate bad news effects in the face of a situation of low level of efficiency and managerial integrity, to the point of minimizing fluctuations in the capital market at the time of voluntary change of auditors.

The main implication of our study is that in the Brazilian institutional setting, which has a mandatory auditor rotation every five years, may reduce the surprise effect of the disclosure of VACs and consequently explain the lack of market and investors’ relevance to the VACs’ announcement. This fact contributes to the literature by providing evidence that when voluntary auditor changes occur in a setting in which mandatory audit rotation has already been implemented, auditor changes can be interpreted as a routine practice that does not provoke stock market reaction due to the difficulty of distinguishing VACs that occurred due to problems with management from those in ordinary business situations.

2. Brazilian Institutional Setting

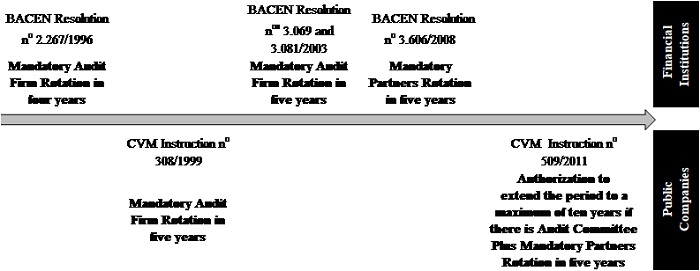

Brazil has specific rules for mandatory rotation of audit firms, which influence the relationship between external auditors and their clients. The mandatory change of audit firms was introduced on March 29, 1996, by the Central Bank of Brazil (Resolution n. 2,267). The decision to implement mandatory auditor rotation was made after the crisis caused by the bankruptcy of two important financial institutions that adopted dubious accounting practices and were audited by Big-four firms with a long-standing relationship with them (Quevedo & Pinto, 2014). This rule established that the mandatory auditor rotation should occur every four years, starting on January 1, 1997, and that the rehiring could only occur after 3 years (BACEN, 1996).

On March 23, 2003, BACEN issued Resolution n. 3,069/2003, which allowed the increase of the audit firm’s term from 4 to 5 years (BACEN, 2003a). Subsequently, on May 29, 2003, BACEN implemented additional requirements to be observed in the hiring of audit firms and demanded that every company create an audit committee (BACEN, 2003b).

Five years later, BACEN decided to replace the mandatory rotation of audit firms with mandatory partner rotation along with the director, manager, or supervisor involved in the audit service every five years, with a three-year cooling-off period for the return of these professionals (BACEN, 2008).

Regarding public companies, on May 14, 1999, the Brazilian Securities and Exchange Commission (CVM) determined that the change of audit firm should be carried out every five years, with a three-year cooling-off period for rehiring the same audit firm (CVM, 1999a). At the time, the CVM justified that the auditor rotation was necessary because the provision of audit services to the same client for a long period could compromise the auditor’s independence and, consequently, the quality of the auditors’ service (CVM, 1999b).

Subsequently, on November 16, 2011, the CVM extended the term of the mandatory rotation of external auditors from five to ten years for companies that had a Statutory Audit Committee and that performed the replacement of the person technically responsible, director, and supervisor in period not exceeding five consecutive years, with a minimum cooling-off period of three years for its return (CVM, 2011).

The CVM also required the audited company’s management to disclose to the market the justification for the voluntary replacement of the audit firm (Instruction n. 308/1999) and inform the CVM about the replacement, as established in Instruction n. 216/1994.

In summary, Brazilian public companies are required to change their audit firm every five years or, at least, the partner when they have a statutory audit committee. Figure 1 shows the chronological evolution of the regulation of auditors’ mandatory rotation applicable in Brazil. Until 2011, most countries did not practice the mandatory rotation of audit firms (Vourc’h & Morand, 2011).

In the European Union, Regulation n. 537/2014 (article 17) established that the independent audit firm could remain providing services to the same public company for 10 years. This period could be extended for another 10 years if a public tender is undertaken or extended for another 14 years if a joint audit is adopted. In addition, this rule still requires the mandatory partner’s rotation after the seventh year of commitment and extended the cooling off period from two years to three years for the previous key audit partner’s return (EU, 2014). This standard specified transition rules until 2023 and allows member states to implement a shorter rotation period.

In the USA, the Sarbanes-Oxley Act (SOX), Public Law 107-204 from July 30, 2002 (article 203), established the mandatory partner rotation every 5 years. Even though the mandatory audit firm rotation was discussed by the Public Company Accounting Oversight Board (PCAOB) and the General Accounting Office (GAO), it was never adopted (Reid and Carcello, 2017).

Litt et al. (2014, p. 59) argue that SOX accelerated the U.S. partner rotation period from seven to five years and expanded the cooling-off period from two to five years, but the effects on financial reporting quality are virtually non-existent, especially because of the lack of publicly available information on audit partners. In addition, Laurion, Lawrence and Ryans (2017, p. 209) provide evidence that U.S. partner rotations support a fresh look at the audit engagement.

Notably, the regulation of mandatory rotation of audit firms followed different directions in Brazil, in the European Union and the United States. The European Union has adopted the mandatory change of firms and partners, as well as Brazil, but with considerably longer periods. Thus, as mandatory auditor changes occur more frequently in the Brazilian context, it is expected that this unique institutional environment may, somehow, affect the frequency and relevance of VACs. It is important to highlight that the Brazilian mandatory audit rotation has been effective for more than two decades.

Further, Velozo et al. (2013) provide evidence of a huge concentration on the Brazilian audit market. They identify that 94 of 100 big Brazilian public companies were audit by big4 firms in 2012. Furthermore, Gisbert and Salotti (2015, p. 3) argue that the Brazilian institutional setting is characterized not only by weak governance mechanisms but also by a lack of strong oversight and enforcement mechanisms, the fact that may harm the expected role of the auditors in the capital markets.

In other words, in an environment where there are only mandatory partners rotation (USA) or mandatory auditor changes take longer to occur (EU), the impact on the return and trading volume of VACs may differ from the Brazilian context, where there are mandatory changes in smaller periods.

3. Prior Studies and Hypotheses

Public companies can voluntarily switch audit firm for several reasons. Regarding the common reasons that lead public companies to carry out the VAC, the following stand out: (a) the possibility of issuing a modified opinion or ongoing concern issues; (b) auditor-client disagreements; (c) changes in senior management; (d) management’s reputation or auditors’ reputation/experience; (e) client’s business strategy; (f) the auditors’ conservative position about earnings management; and (g) cost reduction of audit fees. (Turner, Willians & Weirich, 2005; Schneider, 2015; Guo, Wang, Gao & Sun, 2017). In this line, previous research shows that VAC may occur in situations that bring suspicion about management’s or for benign business reasons, in other words, companies may change audit firm for red flag or non-red flag issues, respectively. (Hossain, Mitra & Rezaee, 2014; Francis et al. 2017).

Regarding market perception about VACs, Hossain, Mitra and Rezaee (2014) states that when companies promote voluntary audit firm rotations for non-red flag issues, it is unlikely that this information damages management’s reputation. Similarly, when VACs are motivated by a reason which signals enhancing company integrity or efficiency, capital market does not react negatively.

Nichols and Smith (1983), for example, found no significant market reaction between 1973 and 1979, neither for listed companies that migrated from non-Big eight audit firm to Big eight audit firm or the other way around. Johnson and Lys (1990) also found no significant reaction from North American public companies in the period between 1973 and 1982. Both studies showed similar results in an environment where client switched to auditors of higher quality due to structural reasons such as growth, changes in capital structure, or better operating performance by reducing audit costs. Another interpretation is that the absence of a significant impact on the capital market stems from the lack of relevant information about VACs (Johnson & Lys, 1990; Klock, 1994; Schwartz & Soo, 1996).

On the other hand, when VACs occur for red flag issues, or for events that are interpreted as “bad news”, capital market negatively reacts. Fried and Schiff (1981), for example, found a negative market reaction to VACs between 1973 and 1979. Similarly, Smith (1988) also found a negative market reaction between 1975 and 1982. Although both studies showed evidence of negative market reaction, Fried and Schiff (1981) states that upgrading audit quality did not reflect any particularly good news to investors, whereas Smith (1988) found that market reacted worse to VAC when companies disclosed a disagreement or qualified opinion. All things considered, some of the first studies that tried to capture the market’s reaction to VACs showed inconclusive results, which can be explained by the lack of enough information regarding reasons that led companies to change auditing firms in that context (Calderon, Ofobike & Cheh, 2007, Hossain, Mitra & Rezaee, 2014).

Along the same lines, Albrecht (1990) argues that the prior qualified opinion or disagreement between the audit firm and client partly explains the negative market reaction to VACs’ announcement. Additionally, more recent studies have shown that when the VAC is due to the auditors’ resignation, the market reacts negatively (Griffin & Lont, 2010; Khalil, Cohen, & Trompeter, 2011). However, Whisenant et al. (2003, p. 43) argue that investors do not distinguish the difference between resignations and dismissals: there is evidence that abnormal stock returns are positively associated with the disclosure of non-verifiable reasons for auditor dismissals but are unrelated to disclosures of verifiable reasons (Sankaraguruswamy & Whisenant, 2004). Hennes, Leone, and Miller (2014) examined how market responds to dismissal announcements after accounting restatements. Findings have shown that market reaction is better following more severe restatements when the client engages a comparably sized auditor. Authors argue that positive market reaction means that public companies have restored financial reporting credibility by replacing their auditors. So, when the reason given for changing auditors reflects new information the market may react to VACs disclosure.

Another type of study linked to red flags issues are those aimed at analyzing to VACs the switch from a Big Four firm to a Non-Big Four. Downward audit firm changes may thus be viewed as leading to a decline in audit quality (Hossain, Mitra & Rezaee, 2014). Eichenseher, Hagigi and Shields (1989) and Dunn et al. (1999) showed evidence that this type of audit switch may damage management’s reputation, causing negative market reaction. On the other hand, Chang, Cheng and Reichelt (2010) analyzed the market’s response to the switch from a Big Four firm to a Non-Big Four firm in the period from 2002 to 2006. The results showed that the stock prices of public companies that migrated to smaller audit firms showed positive returns in the post-SOX period (Chang, Cheng & Reichelt, 2010). In Hong Kong (HK), market reacted negatively to VAC from HK non-Big4 to China non-Big4, but did not react to switches from HK Big4 to China Big4, suggesting that investors differentiate audit quality according to audit firm origin. (Liu & Lin, 2019)

Another aspect that deserves highlighting is the lack of studies on the impact of the VAC on stock volume traded, which has a different informational relevance to stock returns (Beaver, 1968, p. 69). While stock returns are used to verify how the market as a whole reacts to an event, stock volume should be used to verify whether an event is relevant to influence individual investor reaction (Beaver, 1968, p. 69; Bamber et al., 2011). As such, the importance of analyzing the trading volume comes from its potential to yield insights about informational asymmetry and investors’ disagreement on the disclosed event, being of interest not only to accounting researchers but also to policymakers (Bamber et al., 2011, p. 433).

Regarding voluntary change of auditors, Keller and Davidson (1983) detected a significant increase in the abnormal trading volume after the replaced audit firm issued a modified opinion around the VACs’ announcement between 1973 and 1977. Hagigi et al. (1993) analyzed the effect of the announcement of the VAC in 122 in the USA companies on investor expectations between July 1980 and December 1982, considering the market model, a 52-week estimation window and three different event windows (1, 3 and 5 weeks). Findings suggests a significant decrease in the abnormal trading volume for the sample and subsamples with and without changes in the auditors’ size (Big8 to Non-Big8 and Non-Big8 to Big8). These announcements lead to greater agreement among investors (consensus effect) and a reduction of information asymmetry among market participants (information effect) (Hagigi et al., 1993, p. 800).

In general, the reasons why VACs occur are shown to be relevant information for the market. Despite this, Calderon, Ofobike & Cheh (2007, p. 61) argue that companies adopt a check-the-box approach to disclosing the reason for auditors’ change and there is a lack of transparency and little insight about the reasons for auditor changes. In these cases, market response may be reduced by lack of information content about VAC (Ferguson, Lam & Ma, 2018).

In the Brazilian context, Corrêa, Andrade and Silva (2021) analyzed the frequency of voluntary audit firms changes in Brazilian non-financial public companies in the period between 2012 to 2016 and the justifications presented by the administrators for the voluntary changes of independent auditors implemented. The results showed that from 125 VACs, 34 cases companies did not disclose audit firm rotation reason and in another 12 cases, companies disclosed generic reasons such as "business circumstances". In this context, the opportunity arises to investigate the market and investor reaction to the VACs in an environment where there is a considerable level of opacity about the reasons that led to the change, even though disclosure is required by law.

So, considering that the voluntary change of audit firms can impact the market perception and that the results of previous studies are inconclusive, we propose to analyze the following hypotheses:

H1: Companies that voluntarily switched audit firms will present a negative Abnormal Return on the date of the VACs’ announcement.

H2a (H2b): Companies that voluntarily switched from (to) a Big4 audit firm to (from) a non-Big4 will present a negative (positive) Abnormal Return on the date of the VACs’ announcement.

H3: Companies that voluntarily switched from an audit firm to another of the same size will present an Abnormal Return equal to zero on the date of the VACs’ announcement.

The H1 is sustained in view that voluntary audit firm changes may be a consequence of undisclosed conflicts on accounting issues that are more directly related to events or changes in the economic situation of the audited company (Fried & Schiff, 1981; Smith, 1988). Analogously, hypotheses H2a and H2b and H3 are sustained by previous evidence that if the audit service is performed by a Big Four company can generate relevance in the information in Brazilian capital market (Macedo et al., 2014), which means that audit reputation based on the auditors’ size can have a significant impact on stock returns (Eichenseher et al.,1989; Dunn et al., 1999).

In view of the small number of studies that evaluated the impacts of the VAC on the stock volume, this study also intends to analyze the following hypotheses:

H4: Companies that voluntary switched audit firms experience abnormal trading volume equal to zero around the date of the VAC’s announcement.

(a) For the entire sample.

(b) For each auditor change class (Big4 to Non-Big4 or Non-Big4 to Big4)

(c) For another audit firm of the same size.

The fourth hypothesis theoretically based on evidence that suggests that disclosure event informational relevance may be measured by stocks trading volume (Beaver, 1968), to the point of bringing consensus to the opinion of investors about VACs, when the companies maintained or changed the auditors’ size, migrating to minor and to larger ones (Hagigi et al., 1993).

Finally, modified auditor’s opinion issue has a positive relationship with the change of independent auditor, as it impacts the company’s decision to maintain the audit firm (Sprenger, Silvestre & Laureano 2016; Dantas, Barreto & Carvalho, 2017). Taking into accounting that issue of a modified opinion may be an explanatory variable for the relationship between the announcement of the change of audit firm and the market’s reaction (Albrecht, 1990), the analysis of hypothesis H5a is proposed.

H5a (H5b): Companies that voluntarily switched audit firms and that received a modified opinion experience negative abnormal return (abnormal trading volume different from zero) on the date of the VACs’ announcement.

About H5b, its proposal is sustained by evidence that there was a reaction in trading volume on the days close to the issuance of the modified report (Keller & Davidson, 1983) and that disclosure of a report with an emphasis paragraph linked to going-concern problems may cause a reaction on the volume of shares of Brazilian companies (Silva, Lourenço & Sancovschi, 2017).

4. Sample and Research Design

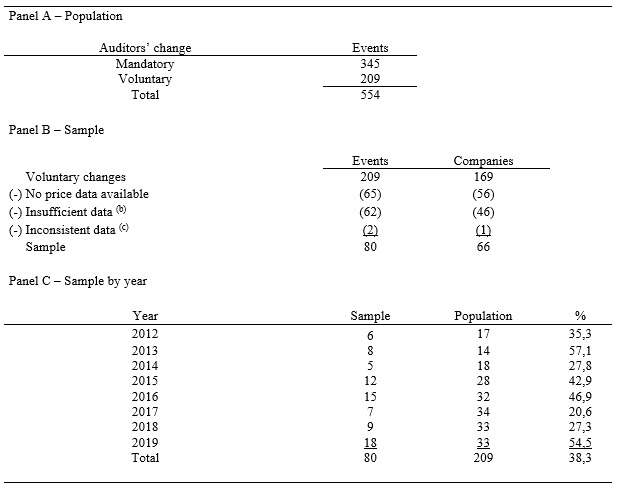

Our analysis focuses on VACs made by Brazilian public companies, which have their shares traded on the Brazilian Stock Exchange (B3). We identified 554 audit firm switches (209 voluntary and 345 mandatories) in 380 public companies from January 2012 to December 2019 (see panel A of Table 1), which comprises the years after the IFRS adoption in Brazil and before the COVID-19 pandemic. Following Schwartz and Soo (1996), we excluded from the sample events where information was not available or inconsistent. We also dropped events with less than 100 observations for prices or trading volume in the estimation window.

Panel B in Table 1 shows that the sample is composed of 80 events (70 events related to common shares and 10 events related to preferred shares), related to 66 public companies with available information to carry out the research.

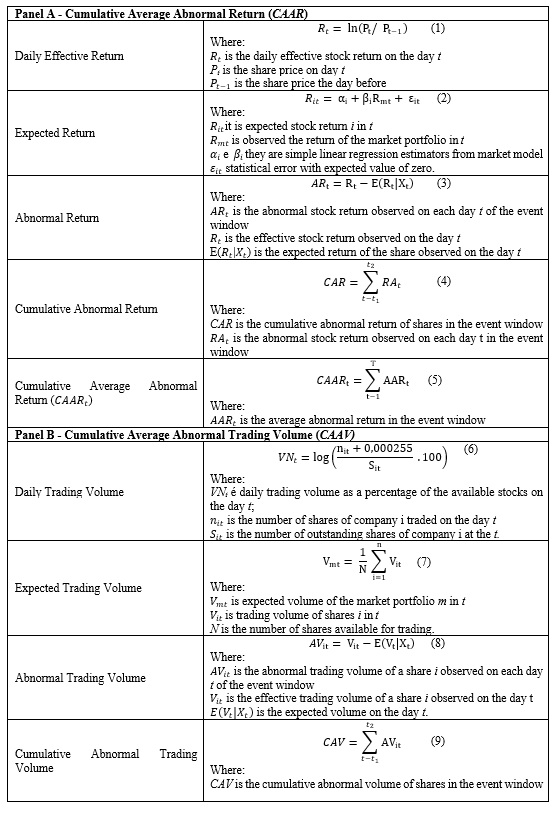

We carried out event study analyses with three different windows to assess the consistency of the results. The event window comprising the day of the event announcement (d0), the two-day period (d0 and d+1) and the three-day window (d-1, d0 and d+1). We use short-term event windows to prevent the effects of the analyzed event from getting confused with other events (Knechel et al., 2007; Arioglu & Tuan, 2015).

The event day was manually identified in the current reports disclosed by public companies. We defined 6:00 pm as the time limit for the event to be considered to happen on the same day of disclosure. From that time onwards, events were considered to take place on the next business day.

The estimation window includes data from 120 days before the event window, as recommended by MacKinlay (1997, p. 15). In addition, we performed robustness tests with estimation windows of 90 and 60 days. As suggested by MacKinlay (1997), we adopted the following procedures in table 2:

To verify whether the abnormal returns and volumes were significant, the statistical test developed by Boehmer, Musemeci, and Poulson (1991) was applied. In cases with less than 30 observations, the non-parametric test proposed by Corrado (1989) was performed. Finally, we performed a Mann-Whitney test on the CARs and on the CAVs of the subsamples to assess whether there was a difference in the market and/or investor reaction regarding the audit firm size and the auditor’s opinion issued by the replaced firm.

The data about VACs, the audit firm size, and the types of auditor’s opinion issued by the replaced audit firm were collected manually from March 2018 to July 2020 on the Brazilian SEC website (www.cvm.gov.br). Prices and trading volume data were obtained automatically from the Yahoo! Finance website (www.yahoofinance.com). The statistical tests were performed with the support of the software Event Study Metrics©.

We also did a complementary qualitative analysis. We explored the documents to verify whether the company informed the reason for the auditor change and the name of the audit firms involved in the process.

5. Results

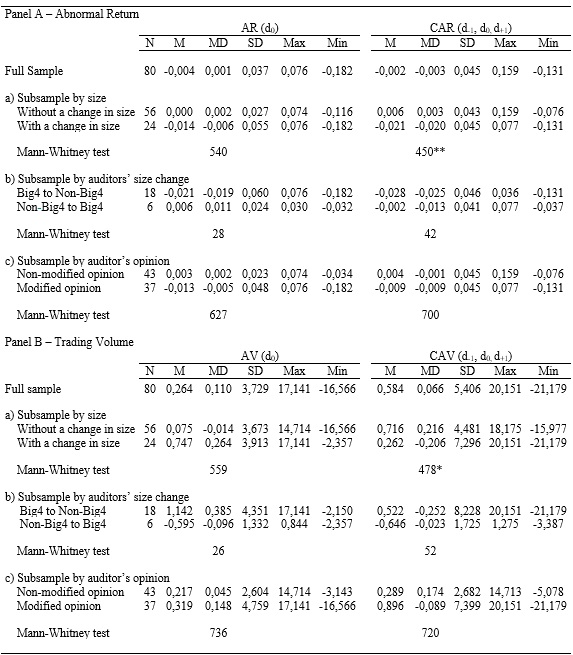

Table 3 presents the descriptive statistics and the preliminary statistical analysis of the Abnormal Returns and Abnormal Traded Volumes for the sample and subsamples.

In Panel A, we can see that there is a significant difference in the average CAR from the subsample with or without change in the auditors’ firm size. Panel B shows that the average CAV is significantly different from the subsample with or without change in auditors’ firm size. So, this result suggests that the market and investors notice the difference between VAC in which there was a change in the size of the audit firm, from those in which there was not.

The CAAR and CAAV statistical analysis are presented in table 4. Panel A shows negative market reaction (CAAR) in all event windows, but the reaction is not statistically significant in any of them (H1 hypothesis is rejected). It is noteworthy that the results are consistent across all estimation and event windows and that the CAAR is higher on the day of the event (d0) than on the 2-day (d0, d+1) or 3- day (d-1, d0, d+1) event windows.

Regarding investor reaction, Panel B in table 4 shows that the CAAV is also not statistically significant in every case (H4a Hypothesis is not rejected). These results are not sensitive to changes in the size of the estimation window but show a considerable increase in the 3-day event window.

Table 5 presents the statistical analysis of the CAAR and CAAV for the subsamples, considering an estimation window of 120 days. Table 5 shows that there is a statistically significant market reaction when the audited companies migrated from a Big4 audit firm to a smaller audit firm. However, this result is sensitive to changes in the size of the estimation window. Using a 90-day estimation window, both cases are not statistically significant. In a 60-day estimation window, only the Average Abnormal Return is statistically significant.

Thus, it is not possible to state categorically that the market reacts negatively when the audit firm is replaced by a smaller firm (H2a Hypothesis is inconclusive). In addition, there is no evidence of market reaction when audited companies migrate from a Non-Big4 to a Big4 or when companies switch from an audit firm to another of the same size (H2b hypothesis is rejected and H3 is not rejected). These results are compatible with prior studies of Nichols and Smith (1983), Johnson and Lys (1990), Klock (1994), Schwartz and Soo (1996) and Arioglu and Tuan (2015).

Regarding the investor reaction (CAAV), table 5 shows that there is no statistical significance for the VACs in cases of a change from a Big4 to a Non-Big4 and vice versa (H4b hypothesis are not rejected).When there was no size change in contracting another audit firm, the results indicate that there is a statistically significant increase in the CAAV in the three-day window, but there was no statistically significant reaction on the day of the event (H4c hypothesis is inconclusive). Our results are convergent with those of Hagigi et al. (1993).

Concerning subsamples by type of auditor’s opinion, Table 5 shows that that there is no market nor investor reaction when public companies disclose their VACs (H5a and H5b hypothesis are rejected). These results diverge from the findings of Albrecht (1990) and Keller and Davidson (1983), which focused on the USA stock market and used event windows longer than 30 days.

It is important to highlight that during the analyzed period, several companies made more than one voluntary auditor change and that these companies also made mandatory auditor rotation in the same period. Table 6 presents VACs classified by disclosed reasons for the change of the audit firm, auditors’ firm size, and auditor’s opinion issued by the replaced auditor.

We see that about 42,5% of cases showed opacity, due to some companies did not disclose the reasons for the VAC and others giving vague justifications like “business circumstances”, corroborating Turner et al. (2005) and Corrêa, Andrade and Silva (2021). Figure 2 illustrates the length of auditors’ contracts from the 66 companies from our sample. The average duration of auditors’ contracts with VAC is 3.1 years, the longest one lasting 9.2 years and the shortest lasting 121 days. The average duration of auditors’ contracts with VAC is 3.1 years, the longest one lasting 9.2 years and the shortest lasting 121 days. We observe that 11 contracts (12.9%) were voluntarily finished before one year and 18 contracts (21.2%) were finished before 2 years. Figure 2 also shows 1.92 auditors’ change by company and 1.29 VACs by company.

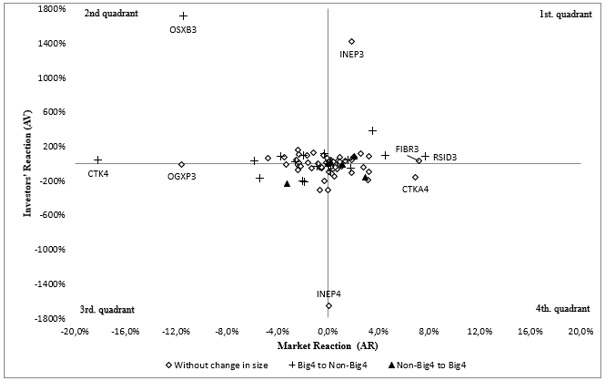

Figure 3 shows the dispersion of the market reaction (ARd0) and investor reaction (AVd0) for the sample. This graph shows that a lot of events are close to zero, but that there are also extreme cases with relevant market and investor reactions.

Notes: (1) This graph shows all voluntary (grayscale bars) and mandatory (black bars) auditors’ change from 66 sample companies (2) The Y-axis represents the days of the auditors’ contract for the baseline on January 1, 2012. (2) The X-axis represents voluntary and mandatory events from each analyzed company. It comprises of 85 voluntary changes (five changes were excluded in our sample because of the lack of data) and 42 mandatory changes.

Notes: (1) AR - Abnormal Return (d0) and AV - Abnormal Trading Volume (d0). (2) Without a change in auditors’ size included change from Big4 to Big4 and Non-Big4 to Non-Big4.

For example, Rossi Residencial common shares (1st quadrant) showed a positive market reaction (RSID3AR = 7.6%) on April 13, 2016, when it announced the VAC from a Big4 (Deloitte) to a non-Big4 (Grand Thornton) to reduce costs. Furthermore, the auditor’s opinion issued by the audit firm replaced on March 30, 2016, had presented a disclaimer paragraph warning about possible problems with ongoing concern.

Similarly, Fibria common shares (1st quadrant) had a significant positive market reaction (FIBR3AR = 7.2%) on March 15, 2016, when it migrated from a Non-Big4 (Baker Tilly) to another Non-Big4 (BDO), due to the incorporation of their old audit firm by the new one.

On the other hand, Karsten preferred shares (2nd quadrant) showed the most negative market reaction (CTKA4AR = -18.2%) in the VAC carried out on May 23, 2017, when the company migrated from a Big4 audit firm (Deloitte) to a Non-Big4 (BDO) due to audit service contract end. The replaced audit firm had issued an auditor’s opinion with a disclaimer paragraph about the uncertainty regarding the company’s ongoing concern two months before the announcement of the VAC (March 28, 2017).

Another event that showed negative market reaction occurred on April 27, 2015, when OGX (3rd quadrant, OGXP3AR = -11.56%) migrated from a Big4 (PWC) to another Big4 (KPMG) due to “business circumstances”. Its last audit report included a disclaimer paragraph due to ongoing concern issues, clarifying that the restructuring of the company would depend on the success of the judicial reorganization plan.

OSXB3 company (2nd quadrant) had the greatest positive investor reaction (OSXB3AV = 1713.9%). On May 9, 2016, the company announced the change from a Big4 audit firm (EY) to a Non-Big4 (BDO), without stating the reason for the VAC. In the last auditors’ opinion, issued on April 13, 2016, the replaced audit firm issued a limitation of scope audit report due to ongoing concern because the client filed for bankruptcy protection for the holding and its subsidiaries.

Finally, Inepar (1st and 4th quadrants) had both positive investor reaction (INEP3AV = 1,422.3%) and negative ones (INEP4AV = -1,657.5%). In the first change, which took place on April 12, 2012, the company migrated from a non-Big4 audit firm (Matinelli Auditores) to a non-Big4 (Baker Tilly) and disclosed that the change occurred due to “business circumstances”. In the prior auditors’ opinion, released 10 days before the auditor change (April 4, 2012), the replaced audit firm issued a qualified opinion due to the recognition of financial assets related to credits with the government for 2001, 2002, and 2008 that still depended on a judicial decision for their respective achievements. In the second VAC, which took place on February 5, 2018, the company replaced a non-Big4 audit firm (BDO auditores) with another non-Big4 (RSM) due to “business circumstances”. In the last report of the auditors, released on July 13, 2017, the audit firm had issued an opinion with a disclaimer paragraph, due to loans receivable from the parent company and problems with ongoing concern.

Although the statistical analysis carried out in the previous section did not reveal a significant market and investor reaction, we could observe, in the qualitative analysis, that some isolated cases did have relevant effects. However, these effects may have occurred due to very specifics aspects associated with the companies’ situation and not necessarily only due to the disclosure of the VACs. In extreme cases, it was possible to observe that these companies were experiencing serious problems related to ongoing concern. This pattern is consistent with Calderon et al. (2007, p. 71).

6. Summary and Final Comments

Our results indicate that there is neither market reaction (CAAR) nor investor reaction (CAAV) to the VACs’ announcement of Brazilian public companies between 2012 and 2019. The subsample analysis for changes in auditors’ size also supports these conclusions, although the result is sensitive to the estimation, the event window size and the small subsample size.

Although the statistical tests carried out in the previous section did not reveal a significant market and investor reaction, we could observe that some outliers showed a significant impact, especially when the companies were experiencing serious problems related to their ongoing concern issues.

The result of this study is relevant because it contributes to the understanding of the market and investor reaction to VACs’ announcement in the Brazilian context, which has different characteristics from the USA and European Union context.

Therefore, our study is important because it shows that institutional settings which have mandatory auditor changes in short periods, like Brazil, may reduce the surprise effect of the disclosure of VACs. This fact, added to the opacity of auditor changes reasons, would consequently minimize VAC relevance to the market. This finding is relevant for capital market regulators from emerging economies since it allows observing the experiences applied in other countries with similar characteristics.

In addition, our study brought to light the need to improve the disclosure of information about the change of audit firm, given that, in many cases, companies either present vague reasons for the exchange or no reason at all.

The main limitation of our research is the reduced number of events analyzed caused by the lack of information on prices and trading volumes, as well as the non-disclosure of important information about VACs in the companies’ current reports.

Like Smith (1988), Hagigi, Kluger and Shields (1993), and Arioglu and Tuan (2015), we also used univariate analysis to evaluate market reaction to audit firm change with subsamples analysis to do the robustness test. However, we are aware that univariate analysis represents a limitation in this paper for not using other control variables. For this reason, we suggest that future studies use a multivariate approach, using control variables such as size, profitability, leverage and sector to improve the analysis of the behavior of stock returns and trading volume due to audit firm changes.

References

Albrecht, D. (1990). The determinants of the market reaction to an announcement of a change in auditor. Unpublished Ph.D. Dissertation, Virginia Polytechnic Institute and State University. http://hdl.handle.net/10919/39947

Arioglu, E., & Tuan, K. (2015). Auditor Rotation at Borsa Istanbul Firms: An Event Study. Journal of Economics Finance and Accounting 2(3), pp. 397-408.

Bamber, L. S., Barron, O. E. & Stevens, D. E. (2011). Trading Volume Around Earnings Announcements and Other Financial Reports: Theory, Research Design, Empirical Evidence, and Directions for Future Research, Contemporary Accounting Research 28(2), pp. 431–471. https://dx.doi.org/10.2139/ssrn.1473439

Banco Central do Brasil – BACEN. (1996). Resolução nº 2267. Brasília, DF: BACEN. Available at: https://bityli.com/RpWa0T (last accessed February 18, 2020).

Banco Central do Brasil – BACEN. (2003a). Resolução nº 3069. Brasília, DF: BACEN. Available at: https://bityli.com/jplOe (last accessed May 2, 2020).

Banco Central do Brasil – BACEN. (2003b). Resolução nº 3081. Brasília, DF: BACEN. Available at: https://bityli.com/2KIY2M (last accessed May 2, 2020).

Banco Central do Brasil – BACEN. (2008). Resolução nº 3606. Brasília, DF: BACEN. Available at: https://bityli.com/nj64Z (last accessed May 2, 2020).

Beaver, W. H. (1968). The information content of annual earnings announcements. Journal of Accounting Research 6(3), pp. 67-92. https://doi.org/10.2307/2490070

Boehmer, E., Musemeci, J., & Poulson, A. B. (1991). Event-Study Methodology under Conditions of Event-Induced Variance. Journal of Financial Economics 30(2), pp. 253-272. https://doi.org/10.1016/0304-405X(91)90032-F

Bronson, S., Harris, K., & Whisenant, S. (2016). Mandatory Audit Firm Rotation: An International Investigation, In Working paper. University of Kansas.

Calderon, T. G., Ofobike, E., & Cheh, J. J. (2007). Is There Transparency in Auditor Change Disclosures? Journal of Applied Business Research 23(3), pp. 61-74. https://doi.org/10.19030/jabr.v23i3.1391

Cameran, M., Prencipe, A., & Trombetta, M. (2014). Mandatory Audit Firm Rotation and Audit Quality. European Accounting Review 25(1), pp. 35-58. https://doi.org/10.1080/09638180.2014.921446

Cameran, M., Negri, G., & Pettinicchio, A. K. (2015). The audit mandatory rotation rule: The state of the art. Journal of Financial Perspectives, 3(2). https://ssrn.com/abstract=3083484

Campbell, C. J., & Wasley, C. E. (1996). Measuring abnormal daily trading volume for samples of NYSE/ASE and NASDAQ securities using parametric and nonparametric test statistics. Review of Quantitative Finance and Accounting 6(3), pp. 309-326. https://doi.org/10.1007/BF00245187

Chang, H., Cheng, C. S. A., & Reichelt, K. J. (2010). Market Reaction to Auditor Switching from Big 4 to Third-Tier Small Accounting Firms. Auditing: a journal of practice & theory 29(2), pp. 83-114. https://doi.org/10.2308/aud.2010.29.2.83

Comissão de Valores Mobiliários – CVM. (1999a). Instrução nº 308. DF: CVM. Available at: https://bityli.com/YEyxd. (Last accessed February 18, 2020).

Comissão de Valores Mobiliários – CVM. (1999b). Nota explicativa à Instrução CVM nº. 308, de 14 de maio de 1999. DF: CVM. https://bityli.com/JOmDPD (last accessed October 24, 2020).

Comissão de Valores Mobiliários – CVM. (2011). Instruçãonº 509. DF: CVM. Available at: https://bityli.com/dCrZs (last accessed February 18, 2020).

Corrado, C. J. (1989). A Nonparametric Test for Abnormal Security-Price Performance in Event Studies, Journal of Financial Economics 23(2), pp. 385-396. https://doi.org/10.1016/0304-405X(89)90064-0

Corrêa, L. F. F. D. S. T., Andrade, A. M., & Silva, A. H. C. (2021). Mudanças de Firmas de Auditoria Independente: Por que Elas Ocorrem no Brasil?. Pensar Contábil, 23(80).

Dantas, J. A., Barreto, I. T., & Carvalho, P. R. M. (2017). Relatório com Modificação de Opinião: Risco para o Auditor? Revista Contemporânea de Contabilidade, 14(33), pp. 140-157. https://doi.org/10.5007/2175-8069.2017v14n33p140

DeAngelo, L. E. (1981). Auditor size and audit quality. Journal of Accounting and Economics 3(3), pp. 183-199. https://doi.org/10.1016/0165-4101(81)90002-1

Defond, M. L., & Francis, J. R. (2005). The Audit Research after Sarbanes–Oxley. Auditing: A Journal of Practice & Theory 24(s-1), pp. 5–30. https://doi.org/10.2308/aud.2005.24.s-1.5

Dunn, J., Hillier, D., & Marshall, A. P. (1999). The market reaction to auditor resignations. Accounting and Business Research 29(2), pp. 95-108. https://doi.org/10.1080/00014788.1999.9729572

Eichenseher, J., Hagigi, M., & Shields, D. (1989). Market reaction to auditor changes by OTC companies. Auditing: A Journal of Practice & Theory, 9(1), pp. 29-40.

European Union (EU) (2014). L 158: Regulation (EU) n. 537/2014 of the European parliament and of the council of 16 April 2014 on specific requirements regarding statutory audit of public-interest entities and repealing commission decision 2005/909/EC (1). Official Journal of the European Union. 57, pp. 77–112.

Ferguson, A., Lam, P., & Ma, N. (2018). Market reactions to auditor switches under regulatory consent and market driven regimes. Journal of Contemporary Accounting & Economics, 14(2), pp. 197-215. https://doi.org/10.1016/j.jcae.2018.05.001

Fried, D., & Schiff, A. (1981). CPA Switches and Associated Market Reactions. Accounting Review, 56 (2), pp. 326-341. http://www.jstor.org/stable/245816

Gisbert, A., & Salotti, B. (2015). Firm Incentives, Institutional Factors and Accounting Quality: The IFRS Adoption in Brazil (February 15, 2015). http://dx.doi.org/10.2139/ssrn.2565533

Griffin, P. A., & Lont, D. H. (2010). Do Investors Care About Auditor Dismissals and Resignations? What Drives the Response? Auditing: A Journal of Practice & Theory, 29(2), pp. 189-214. https://doi.org/10.2308/aud.2010.29.2.189

Guo, L., Wang, S., Gao, J., & Sun, W. (2017). The literature review of auditor changes, International Conference on Service Systems and Service Management, Dalian, pp. 1-6. https://bityli.com/tNXu63. (Last accessed September 13, 2020).

Hagigi, M., Kluger, B. D., & Shields, D. (1993). Auditor Change Announcements and Dispersion of Investor Expectations. Journal of Business Finance & Accounting 20(6), pp. 787-802. https://doi.org/10.1111/j.1468-5957.1993.tb00293.x

Hennes, K. M., Leone, A. J., & Miller, B. P. (2014). Determinants and market consequences of auditor dismissals after accounting restatements. The Accounting Review, 89(3), pp. 1051-1082. https://doi.org/10.2308/accr-50680

Horton, J., Livne, G., & Pettinicchio, A. (2021). Empirical evidence on audit quality under a dual mandatory auditor rotation rule. European Accounting Review, 30(1), pp. 1-29. https://doi.org/10.1080/09638180.2020.1747513

Hossain, M., Mitra, S., & Rezaee, Z. (2014). Voluntary disclosure of reasons for auditor changes and the capital market reaction to information disclosure. Research in Accounting Regulation, 26(1), pp. 40-53. https://doi.org/10.1016/j.racreg.2014.02.004

Johnson, W. B., & Lys, T. (1990). The Market for Audit Services: Evidence from Voluntary Auditor Changes. Journal of Accounting and Economics, 12(1-3), pp. 281-308. https://doi.org/10.1016/0165-4101(90)90051-5

Keller, S. B., & Davidson, L. F. (1983). An assessment of individual investor reaction to certain qualified audit opinions. Auditing: A Journal of Practice & Theory 3(1), pp. 1–22.

Khalil, S. K., Cohen, J. R., & Trompeter, G. M. (2011). Auditor resignation and firm ownership structure. Accounting Horizons, 25(4), pp. 703-727. https://doi.org/10.2308/acch-50061

Klock, M. (1994). The Stock Market Reaction to a Change in Certifying Accountant. Journal of Accounting, Auditing and Finance 9(2), pp. 339-347. https://doi.org/10.1177/0148558X9400900213

Knechel, W. R., Naiker, V., & Pacheco, G. (2007). Does Auditor Industry Specialization Matter? Evidence from Market Reaction to Auditor Switches. Auditing: A Journal of Practice & Theory, 26(1), pp. 19-45. https://doi.org/10.2308/aud.2007.26.1.19

Laurion, H., Lawrence, A., & Ryans, J. P. (2017). U.S. Audit Partner Rotations. The Accounting Review, 92(3), pp. 209-237. https://doi.org/10.2308/accr-51552

Litt, B., Sharma, D. S., Simpson, T., & Tanyi, P. N. (2014). Audit Partner Rotation and Financial Reporting Quality. Auditing: A Journal of Practice & Theory, 33(3), pp. 59-86. https://doi.org/10.2308/ajpt-50753

Liu, Z., & Lin, S. (2019). Determinants and consequences of voluntary switches to Chinese auditors in Hong Kong. Journal of Contemporary Accounting & Economics, 15(3), pp. 100-158 https://doi.org/10.1016/j.jcae.2019.100158

Macedo, M. A. S., Silva, D. T., Ayub, G. P., & Pacheco, L. O. (2014). Impacto de mecanismos de auditoria na precificação de ações: evidências sob a perspectiva da relevância e da tempestividade para o ano de 2010 no Brasil. Contabilidade, Gestão e Governança, 17(3), pp. 127-144. https://bityli.com/ioNabM (last accessed December 1, 2020).

Mackinlay, A. C. (1997). Event Studies in Economic and Finance. Journal of Economic Literature, 35(1), pp. 13-39. http://www.jstor.org/stable/2729691

Nichols, D.R., & Smith, D. B. (1983). Auditor Credibility and Auditor Changes. Journal of Accounting Research, 21(2), pp. 534-544. https://doi.org/10.2307/2490789

Parreira, M. T. S., Nascimento, E. M., Puppin, L., & Murcia, F. D. R. (2021). Rodízio de auditoria independente e gerenciamento de resultados: uma investigação entre empresas de capital aberto no Brasil. Enfoque: Reflexão Contábil, 40(1), pp. 67-86. https://doi.org/10.4025/enfoque.v40i1.44318

Quevedo, M. C., and Pinto, L. J. S. (2014). Percepção do Rodízio de Auditoria sob o Olhar dos Auditores Independentes. Revista Catarinense da Ciência Contábil, 13(38), pp. 9–22.

Reid. L. C., & Carcello, J. V. (2017). Investor Reaction to the Prospect of Mandatory Audit Firm Rotation. The Accounting Review, 92(1), pp. 183-211. https://doi.org/10.2308/accr-51488

Rocha Júnior, F. R., Rodrigues Sobrinho, W. B., & Bortolon, P. M. (2016). Fatores determinantes da mudança voluntária da empresa de auditoria externa no mercado brasileiro. Enfoque Reflexão Contábil, 35(3), pp. 53-67. https://doi.org/10.4025/enfoque.v35i3.29460

Sankaraguruswamy, S., & Whisenant, J. S. (2004). An empirical analysis of voluntarily supplied client‐auditor realignment reasons. Auditing: A Journal of Practice & Theory, 23(1), pp. 107-121. https://doi.org/10.2308/aud.2004.23.1.107

Schneider, A. (2015). Does information about auditor switches affect investing decisions?. Research in Accounting Regulation, 27(1), pp. 39–44. https://doi.org/10.1016/j.racreg.2015.03.004

Schwartz, K. B., & Soo, B. S. (1996). The Association Between Auditor Changes and Reporting Lags. Contemporary Accounting Research, 13(1), pp. 353-370. https://doi.org/10.1111/j.1911-3846.1996.tb00505.x

Silva, A. H. C., Lourenço, T. S., & Sancovschi, M. (2017). Reação do Mercado aos Pareceres dos Auditores Sobre Incertezas Quanto à Continuidade Operacional de Empresas de Capital Aberto após a Adoção do IFRS. Pensar Contábil, 19(70), pp. 4-13.

Silvestre, A. O., Costa, C. M., & Kronbauer, C. A. (2018). Rodízio de auditoria e a qualidade dos lucros: Uma análise a partir dos accruals discricionários. BBR. Brazilian Business Review, 15(5), pp. 410-426. https://doi.org/10.15728/bbr.2018.15.5.1

Smith, D. B. (1988). An Investigation of Securities and Exchange Comission Regulation of Auditor Change Disclosures: The Case of Accounting Series Release No. 165. Journal of Accounting Research, 26(1), pp. 134-145. https://doi.org/10.2307/2491117

Sprenger, K. B., Silvestre, A. O., & Laureano, R. V. (2016). Relatório de Auditoria Independente Modificado e o Rodízio de Firma de Auditoria. XVI Congresso USP de Controladoria e Contabilidade, São Paulo. Anais do Congresso USP de Controladoria e Contabilidade, 2016.

Turner, L., Williams, J., & Weirich, T. (2005). An inside look at auditor changes, The CPA Journal, 1, pp. 12-21.

Velozo E. J., Pinheiro, L. B., Santos, M. J. A., & Cardozo., J. S. S. (2013). Concentração de Firmas de Auditoria: Atuação das Big Four no Cenário Empresarial Brasileiro. Revista Pensar Contábil, 15(58), pp. 55-61.

Vourc’h, J., & Morand, P. (2011). Executive Summary — Study on the Effects of the Implementation of the Acquis on Statutory Audits of Annual and Consolidated Accounts Including the Consequences on the Audit Market. ESCP Europe, Paris. Available at: https://bityli.com/PZ1Fb (last accessed December 1, 2020).

Whisenant, J. S., Sankaraguruswamy, S., & Raghunandan, K. (2003). Market Reactions to Disclosure of Reportable Events. Auditing: A Journal of Practice & Theory, 22(1), pp. 181-194. https://doi.org/10.2308/aud.2003.22.1.181

Notes

*

Artículo de investigación