APA

ISO 690-2

Harvard

Haga clic en un formato de citación

Management of Supply Chain Finance Business Operations, Considering Credit Risk Evaluation *

Gestión de las operaciones comerciales de financiación de la cadena de suministro, teniendo en cuenta la evaluación del riesgo crediticio

Zhe Wu ![]()

Management of Supply Chain Finance Business Operations, Considering Credit Risk Evaluation *

Ingeniería y Universidad, vol. 30, 2026

Pontificia Universidad Javeriana

Zhe Wu a zhewuwz@outlook.com

Zhejiang Business College, Hangzhou, China

Received: 28 february 2025

Accepted: 21 november 2025

Published: 26 february 2026

Abstract: Objectives: With the advancement of supply chain finance, the consideration of credit risk evaluation has become increasingly important. Materials and methods: This paper provides a brief analysis of supply chain business operations and management and establishes a credit risk evaluation system. Then, the support vector machine (SVM) was chosen as the evaluation method for credit risk, and an improved salp swarm algorithm (ISSA) was proposed to search for the optimal SVM parameters. Thus, the ISSA-SVM algorithm was developed. Experiments were conducted using data from the manufacturing supply chain finance sector. Results and discussion: The results demonstrated that the ISSA performed well in obtaining the optimal solution. Moreover, the ISSA-SVM exhibited superior performance in credit risk evaluation, achieving an accuracy rate of 0.981, along with F1 and area under the curve (AUC) values of 0.975 and 0.912, respectively. Conclusions: These results surpassed those of logistic regression and other algorithms, thereby validating the reliability of the ISSA-SVM for credit risk evaluation. The proposed method applies to the operational management of practical supply chain finance.

Keywords:Credit Risk Evaluation, Supply Chain Finance, Business Operation Management, Support Vector Machine.

Resumen: Objetivos: con el avance de las finanzas de la cadena de suministro, la consideración de la evaluación del riesgo crediticio ha cobrado cada vez más importancia. Materiales y métodos: este artículo ofrece un breve análisis de las operaciones y la gestión de las cadenas de suministro y establece un sistema de evaluación del riesgo crediticio. A continuación, se eligió la máquina de vectores de soporte (SVM) como método de evaluación del riesgo crediticio y se propuso un algoritmo mejorado de enjambre de salpas (ISSA) para buscar los parámetros óptimos de la SVM. Así, se desarrolló el algoritmo ISSA-SVM. Se realizaron experimentos utilizando datos del sector de las finanzas de la cadena de suministro de la industria manufacturera. Resultados y discusión: los resultados demostraron que el ISSA funcionó bien a la hora de obtener la solución óptima. Además, el ISSA-SVM mostró un rendimiento superior en la evaluación del riesgo crediticio, alcanzando una tasa de precisión del 0,981, junto con valores F1 y área bajo la curva (AUC) de 0,975 y 0,912, respectivamente. Conclusiones: estos resultados superaron a los de la regresión logística y otros algoritmos, lo que valida la fiabilidad del ISSA-SVM para la evaluación del riesgo crediticio. El método propuesto se aplica a la gestión operativa de la financiación práctica de la cadena de suministro.

Palabras clave: evaluación del riesgo crediticio, financiación de la cadena de suministro, gestión de operaciones comerciales, máquina de vectores de soporte.

Introduction

Facing the important role that small and medium-sized enterprises (SMEs) play in the economic system [1], supply chain finance (SCF), as an innovative financing method [2], has significantly supported the financing needs of SMEs [3]. SCF refers to the financing business provided by financial institutions that relies on the supply chain and centers around core enterprises, targeting SMEs in the upstream and downstream of the chain [4]. Credit risk evaluation constitutes a crucial component in the operational management of financial institutions, and various methods have been employed. Xie et al. [5] developed a random forest-weighted naive Bayes (RF-WNB) model for assessing enterprise credit risk within the supply chain. They verified its effectiveness through a case study on 1,363 listed enterprises. Zhang [6] introduced a model combining long short-term memory, a convolutional neural network, and soft attention. They found through comparisons that the proposed model achieved high accuracy in most cases, meeting the requirements of enterprise credit risk assessment. Qiao et al. [7] conducted a study on risk management in SCF. They discovered, through analyzing survey data from 286 SMEs, that the capability of supply chain risk management significantly influences financing performance. Yang et al. [8] employed the Lasso-Logistic model to examine the factors influencing SMEs’ credit risk and discovered that transaction credit and reputation regulation have a significant impact on credit risk. Wei et al. [9] established a comprehensive network of SMEs and employed network micro-structure along with machine learning to construct a credit evaluation model. They found that network-based features could significantly enhance credit risk assessment. Additionally, they pointed out that if SMEs are closely connected to micro-lending institutions through various relationships, their default probability will increase. Li et al. [10] proposed a hybrid credit risk assessment model based on a stacked ensemble method. Experiments showed that this method could classify samples more effectively. Li et al. [11] proposed an improved multi-criteria optimization classifier based on LASSO. Through experiments on four real-world credit risk datasets, it was found that this method was more effective for credit risk assessment, offering better efficiency and interpretability. It can be seen that current research on credit risk assessment mostly focuses on one or a specific type of enterprise, and machine learning methods are widely used. Although research on credit risk evaluation in SCF remains limited, its rapid growth makes it imperative to develop robust credit risk assessment frameworks. Therefore, this paper screened credit risk evaluation indicators specific to SCF and developed a support vector machine (SVM)-based method for assessing corporate credit risk, intending to support credit decision-making in financial institutions. By incorporating financial indicators within the SCF context, this study addresses the oversight of supply-chain-related factors in traditional enterprise credit risk evaluation methods, thereby enriching the theoretical dimension of SCF credit risk research. Through empirical validation of SVM performance and comparisons with traditional machine learning methods, the theoretical advantages of SVM in handling complex SCF credit risks are highlighted. This paper also provides theoretical support for the interdisciplinary integration of machine learning algorithms and SCF, laying a methodological foundation for subsequent research.

Supply Chain Business Operations Management

Financing Issues for SMEs

SMEs often face challenges in meeting the loan requirements of financial institutions due to insufficient capital [12]. These enterprises often lack real estate collateral, exhibit limited debt servicing capacity, and are subject to higher interest rates on credit loans, which further increases their financing costs. Stringent listing requirements also make it difficult for SMEs to raise funds through direct financing in the securities market. Additionally, the financing needs of SMEs are characterized by small amounts, short-term durations, and high frequency, making the operation and management of such transactions time-consuming and labor-intensive. As a result, financial institutions tend to prefer larger and higher-quality customers, exacerbating the financing challenges faced by SMEs [13].

SCF offers a novel approach to SME financing [14]. Financial institutions leverage the core enterprise as collateral, evaluate the repayment capacity of SMEs based on inter-enterprise transactions within the supply chain, and adopt methods such as accounts receivable financing and inventory pledges to meet the financing requirements of the entire supply chain. In this scenario, risk management extends throughout every link in the supply chain, effectively mitigating lending risks and addressing the financing challenges between SMEs and financial institutions [15].

Credit Risk Evaluation Indicators

In the management of supply chain business operations, credit risk refers to the potential default that may arise in financing activities. Credit risk arises when an enterprise fails to repay a loan on time due to various reasons. Within the context of SCF, credit risk can be transmitted to partners, triggering a chain reaction throughout the entire supply chain and resulting in losses for financial institutions. Therefore, it is necessary to consider the vulnerability of the supply chain network in the management of supply chain business operations, and evaluating the credit risk of SMEs is also an important element. In the analysis of SCF, credit risk may stem from the following sources:

(1) SMEs: SMEs are susceptible to defaults due to inadequate operational and risk management practices;

(2) core enterprise: A core enterprise with a weakened credit profile and an inability to provide guarantees can disrupt the functioning of SCF;

(3) supply chain: Insufficient communication and information exchange among supply chain enterprises lead to information asymmetry, hindering capital providers from timely understanding how SMEs utilize loans, thereby increasing credit risk.

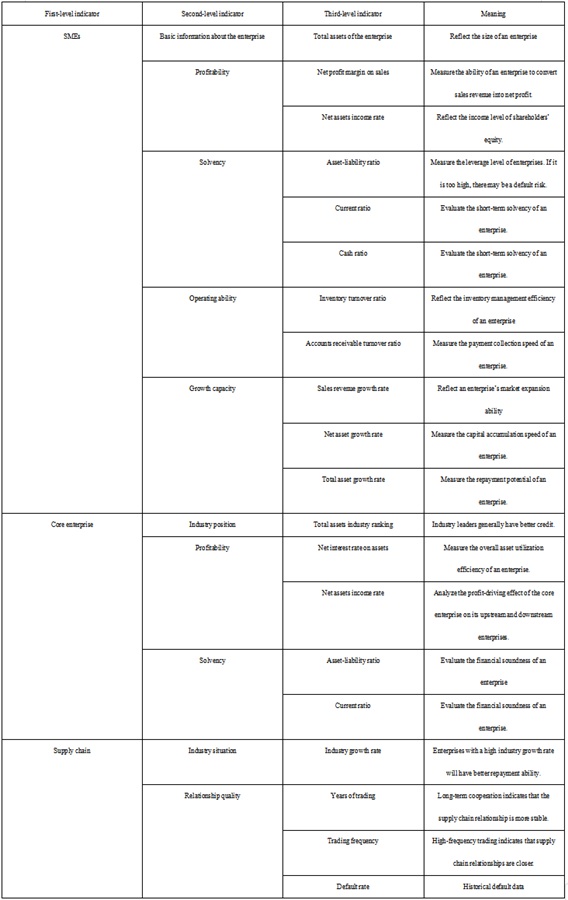

Combined with the above analysis and existing research on credit risk evaluation indicators, this paper designed a set of evaluation indicators based on the characteristics of SCF (Table 1). The indicators in the table cover three dimensions: individual SMEs, core enterprises, and the supply chain. Moreover, all the indicators can be obtained from financial statements or transaction data, which is convenient for calculation.

Credit Risk Evaluation Methods

Problem Statement

The objective of credit risk evaluation is to determine the availability of a loan, which can be seen as a binary classification problem. The credit risk assessment of SCF plays an important role for financial institutions and enterprises in the supply chain. Traditional credit risk assessment methods, such as logistic regression and decision trees, may have problems of linear inseparability or overfitting when facing the nonlinear and high-dimensional characteristics of the credit risk assessment index data of SCF. Moreover, neural networks are also prone to overfitting when dealing with small sample size problems. SVM has shown good performance in solving binary classification tasks and is widely used in various scenarios [16]. It can also handle high-dimensional data and small sample data efficiently. The parameters of SVM are often optimized by a genetic algorithm (GA) or a particle swarm optimization (PSO). However, GA has the defect of being prone to premature convergence, and PSO is prone to falling into a local optimum. Salp swarm algorithm (SSA), which has an excellent global search ability, can avoid premature convergence and has the advantages of fewer parameters and easy tuning, which is more suitable for optimizing the parameters of SVM.

Based on this, this paper proposed a method that uses an improved salp swarm algorithm (ISSA) to optimize the parameters of SVM, established the ISSA-SVM-based credit risk evaluation model to obtain more accurate evaluation results, and took the manufacturing supply chain as an example to verify the proposed model using empirical data.

Support Vector Machine

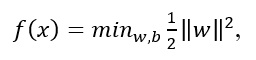

The objective of SVM is to identify an optimal classification hyperplane to divide a sample into two parts. The mathematical model is written as:

(1)

(1)where w is the normal vector of the hyperplane and b is the bias term.

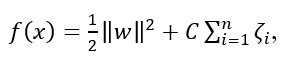

If the sample is linearly indivisible, it is mapped to a high-dimensional space to create a hyperplane:

(2)

(2)where C is the penalty factor and ζi is the slack variable.

The Lagrange function is introduced to solve the problem, and the optimal classification function is written as:

(3)

(3)where ai is the Lagrange multiplier.

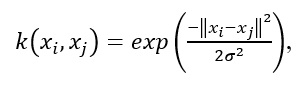

Credit risk evaluation indicator data has high-dimensional and nonlinear characteristics. SVM maps the sample data to the high-dimensional space through a kernel function k [17]. Radial basis function (RBF) and polynomial functions are commonly used kernel functions. However, when solving a nonlinear problem, the RBF generally demonstrates better performance. Therefore, this paper uses the RBF:

(4)

(4)where σ is the Gaussian kernel bandwidth.

Salp Swarm Algorithm

The salp swarm algorithm (SSA) is inspired by the food-searching behavior of salps [18] and has been widely used in optimization design [19] and parameter estimation [20]. During the food search, salps use a head-tail connection between individuals to move toward the food source and finally encircle the prey. The algorithm divides the individuals into two categories: the leader, which actively searches for food, and the followers, which move sequentially behind the leader to encircle the food. Assuming that the food location is denoted as G and the position matrix of n salps in the d-dimensional space is represented as Snxd . The position of the leader is updated:

(5)

(5)

(6)

(6)Where Gj is the food position, r1 , r2 and r3 are adjustment factors, uj and lj refer to the upper and lower bounds of the j-dimensional space, t is the current iteration count, and tmax is the maximum number of iterations.

Followers move closer to the leader, and their positions are updated below:

(7)

(7)Where S i-1,j refers to the position of salp i-1. It can be noticed that the followers all move towards the previous salp.

SSA is simple in principle, has fewer parameters, and is easy to implement, but it is easy to fall into local optimality. To improve this, this paper improves SSA to get the improved SSA (ISSA) algorithm. The improvement is as follows.

(1) Self-adaptive weight w is added:

(8)

(8)where Wmax and Wmin are the maximum and minimum values of w.

(2) Levy flight perturbation [21] is added to change the leader position update formula to:

(9)

(9)

(10)

(10)where s is the Levy flight step length,μ and V are random variables in the Levy flight strategy.

ISSA-SVM for Credit Risk Evaluation

There are two important parameters in SVM: penalty factor C and kernel width σ values will affect the classification results. Therefore, this paper uses the ISSA algorithm to realize the optimization of SVM parameters, and the process is as follows.

(1) The salp position is initialized, and the search range for parameters C and σ is set.

(2) SVM parameters are initialized.

(3) The fitness of individual salps is calculated, and the position where the salp with the highest fitness is located is the food location.

(4) The location of individual salps is updated according to the equation.

(5) The fitness and food location are updated.

(6) Whether the maximum number of iterations is reached is determined. If not, return to step

(3); if it is, then output the optimal C and σ

Results and Analysis

Experimental Setup

Taking the manufacturing supply chain as the subject, index data of 92 companies from the upstream and downstream of the supply chain between 2022 and 2023 were collected from Windows and the GTA Wealth Management Database. One hundred and eighty samples were obtained after eliminating abnormal samples. Referring to the “Standard Values for Evaluation of Enterprise Performance”, the enterprise’s interest protection multiple was used to determine the presence of credit risk; 120 samples without credit risk were obtained, which were assigned a value of 0, and 60 samples with credit risk were also obtained, which were assigned a value of 1. The experiment adopted five-fold cross-validation. The results were expressed as mean ± standard deviation. Significance analysis was conducted on the outcomes of different methods, and the significance level was set at 0.05. The samples were transformed into dimensionless data:

(11)

(11)Let the size of the SSA population be 30, the maximum number of iterations be 50, and the value range of C and σ be [0.001,50]. C =35.12, σ = 1.88, were obtained by ISSA optimization, which was inputted into an SVM for credit risk evaluation.

Results Analysis

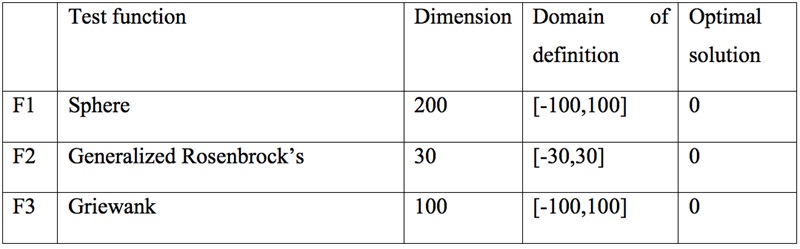

First, the optimization performance of the ISSA was analyzed based on five test functions (Table 2).

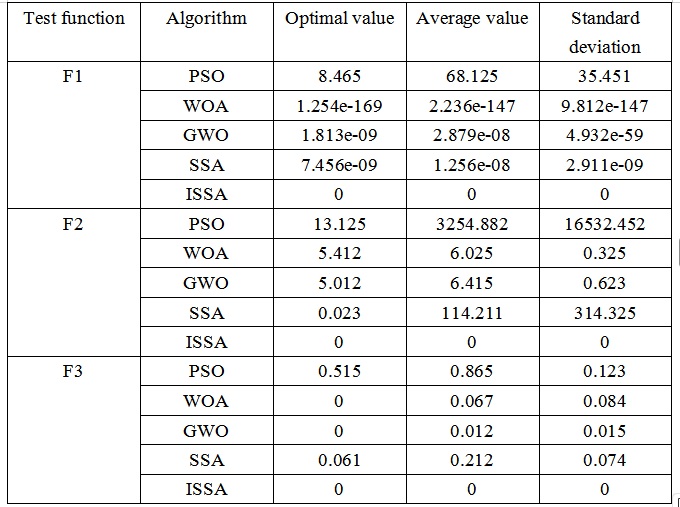

The ISSA was compared with several optimization algorithms, including the particle swarm optimization (PSO) algorithm [22], the whale optimization algorithm (WOA) [23], the gray wolf algorithm (GWO) [24], and the original SSA.

From Table 3, it can be observed that the ISSA was capable of identifying the optimal solution for all three test functions and effectively escaping local optima. In terms of optimal value, average value, and standard deviation, the ISSA outperformed other optimization algorithms, such as PSO, which confirms the optimization accuracy and solution effectiveness of the ISSA. The PSO performed poorly on three test functions. A significant gap was observed in the mean value and the standard deviation of PSO on F2, indicating that the PSO was prone to premature convergence. The WOA and GOA performed better than the PSO. They approached the optimal solution on some functions, but their stability was not as good as that of the ISSA. The comparison between SSA and ISSA further proves the effectiveness of the improvement of SSA. Overall, the ISSA exhibited good global search ability and stability.

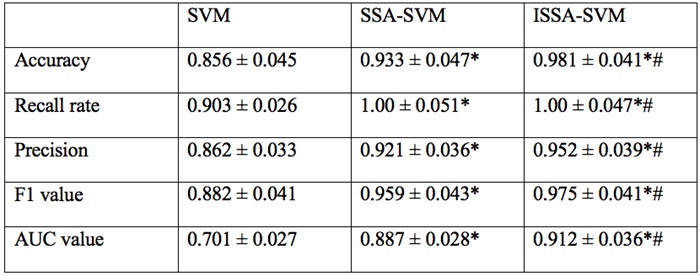

Then, the developed ISSA-SVM algorithm was employed to assess whether the samples in the test set pose a credit risk. Its classification performance was compared with the SVM, SSA-SVM, and ISSA-SVM algorithms.

According to Table 4, the SVM achieved an accuracy of only 0.856 ± 0.045, an F1 value of 0.882 ± 0.041, and an area under the curve (AUC) value of 0.701 ± 0.027 in credit risk evaluation. However, introducing SSA to optimize SVM parameters significantly enhanced its classification performance. The accuracy reached 0.933 ± 0.047, and the F1 value increased to 0.959 ± 0.043. The AUC value also rose to 0.887 ± 0.028. When compared with the SVM algorithm, p < 0.05. The combination of the SVM with the ISSA yielded the best performance in credit risk evaluation, with an accuracy of 0.981 ± 0.041. Additionally, the F1 value and AUC value were significantly higher than those of the SSA-SVM algorithm. These results validate the enhancements made to the SSA and confirm the effectiveness of the ISSA-SVM algorithm in assessing credit risk.

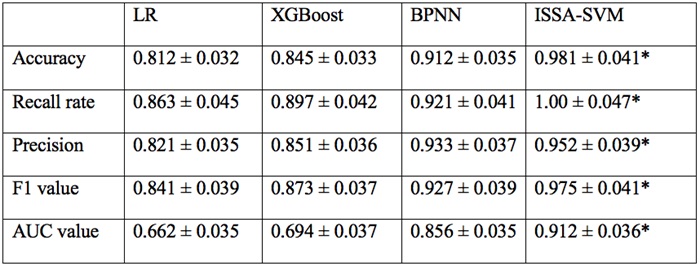

The ISSA-SVM algorithm was compared with several other current classification algorithms, including logistic regression (LR) [25], extreme gradient boosting (XGBoost) [26], and back-propagation neural network (BPNN) [27].

According to Table 5, the LR algorithm demonstrated low effectiveness in credit risk evaluation, with an accuracy rate of only 0.812 ± 0.032, an F1 value of 0.841 ± 0.039, and an AUC value of 0.662 ± 0.035. Using LR for credit risk evaluation may lead to many judgment errors, which is not conducive to the management of SCF’s business operations. The XGBoost algorithm achieved an accuracy rate of 0.845 ± 0.033, an F1 value of 0.873 ± 0.037, and an AUC value of 0.694 ± 0.036, respectively. The BPNN algorithm had an accuracy rate of 0.912 ± 0.035, an F1 value of 0.927 ± 0.035, and an AUC value of 0.856 ± 0.035. The performance of both algorithms was inferior to that of the ISSA-SVM algorithm. These results highlight the reliability of the ISSA-SVM algorithm for credit risk evaluation, providing solid support for the business operation management of SCF.

Conclusion

This paper focuses on credit risk evaluation for the business operation management of SCF. An evaluation index system was established, and an ISSA-SVM method was developed. Through the analysis of the experimental data, it was found that the ISSA demonstrated strong performance in optimization. In the evaluation of credit risk, the ISSA-SVM algorithm also exhibited excellent classification effectiveness, indicating its potential applicability in the actual business operation management of SCF.

However, the research in this paper also has some limitations. For example, it only studied the manufacturing supply chain and did not consider the universality of the proposed method in other industries. The sample scope was relatively small, and the selection of financial indicators was not comprehensive enough. In future research, the supply chains of more industries will be analyzed to verify the applicability of the proposed method. More quantitative and qualitative financial indicators will be considered, and experiments will be carried out on a larger and more diverse sample to improve the proposed classification model.

References

[1] N. Yoshino and F. Taghizadeh-Hesary, “Analysis of Credit Ratings for Small and Medium-Sized Enterprises: Evidence from Asia,” Asian Dev. Rev., vol. 32, no. 2, 2021, 18-37.

[2] M. Jia, “Research on Supply Chain Finance Profit Model Based on E-commerce Platform,” International Conference on E-Commerce and Internet Technology, 2021, 117-120.

[3] W. Liu, Z. Chen, and T. Liu, “Model analysis of smart supply chain finance of platform-based enterprises under government supervision,” Ann. Oper. Res., vol. 336, no. 3, 2024, 1929-1963.

[4] P. Xiao, M. I. Salleh, B. B. Zaidan and Y. Xuelan, “Research on risk assessment of blockchain-driven supply chain finance: A systematic review,” Comput. Ind. Eng., vol. 176, 2023, 108990-.

[5] X. Xie, J. Zhang, Y. Luo, J. Gu, and Y. Li, “Enterprise credit risk portrait and evaluation from the perspective of the supply chain,” Int. T. Oper. Res., vol. 31, no. 4, 2024, 2765-2795.

[6] L. Zhang, “The Evaluation on the Credit Risk of Enterprises with the CNN-LSTM-ATT Model,” Comput. Intel. Neurosc., vol. 2022, 2022, 6826573.

[7] R. Qiao and L. Zhao, “Highlight risk management in supply chain finance: effects of supply chain risk management capabilities on financing performance of small-medium enterprises,” Supply Chain Management, vol. 28, no. 5, 2023, 843-858.

[8] Y. Yang, X. Chu, R. Pang, F. Liu, and P. Yang, “Identifying and Predicting the Credit Risk of Small and Medium-Sized Enterprises in Sustainable Supply Chain Finance: Evidence from China,” Sustainability, vol. 13, no. 10, 2021, 1-19.

[9] L. Wei, J. Lin, and W. Cen, “Stronger relationships higher risk? Credit risk evaluation based on SMEs network microstructure,” Emerging Markets Review, vol. 62, 2024, 101189.

[10] Y. Li, R. Zhao, and M. Sha, “A Hybrid Credit Risk Evaluation Model Based on Three-Way Decisions and Stacking Ensemble Approach,” Computational Economics, 2024, 1-24.

[11] X. Li, Z. Zhang, L. Li, and H. Pan, “Combining Feature Selection and Classification Using LASSO-Based MCO Classifier for Credit Risk Evaluation,” Computational Economics, vol. 64, no. 5, 2024, 2641-2662.

[12] S. Gherghina, M. A. Botezatu, A. Hosszu, and L. N. Simionescu, “Small and Medium-Sized Enterprises (SMEs): The Engine of Economic Growth through Investments and Innovation,” Sustainability, vol. 12, no. 1, 2020, 1-22.

[13] Q. Ma, “Research on Financing Difficulties of Small and Medium-sized Enterprises in Anhui Province under the Background of Big Data,” 2020 Management Science Informatization and Economic Innovation Development Conference (MSIEID), 2020, 17-20.

[14] A. Jafarnejad, G. Abdoli, H. A. Mahdiraji, and S. K. Esbouei, “Optimization of supply chain finance based on Stackelberg model,” Ind. Eng. Manag., vol. 8, 2021, 72-88.

[15] X. Chen, C. Wang, and S. Li, “The impact of supply chain finance on corporate social responsibility and creating shared value: a case from the emerging economy,” Supply Chain Manag., vol. 28, no. 2, 2022, 324-346.

[16] V. Mcfarlane, M. Loewen and F. Hicks, “Field measurements of suspended frazil ice. Part I: A support vector machine learning algorithm to identify frazil ice particles,” Cold Reg. Sci. Technol., vol. 165, 2019, 1-9.

[17] R. M. Schuhmann, A. Rausch, and T. Schanze, “Parameter estimation of support vector machine with radial basis function kernel using grid search with leave-p-out cross validation for classification of motion patterns of subviral particles,” Curr. Direct. Biomed. Eng., vol. 7, no. 2, 2021, 121.

[18] D. Bairathi and D. Gopalani, “Salp Swarm Algorithm (SSA) for Training Feed-Forward Neural Networks,” International Conference on Soft Computing for Problem Solving, 2019, 521-534.

[19] Ł. Knypiński, M. Kurzawa, R. Wojciechowski, and M. Gwóźdź, “Application of the Salp Swarm Algorithm to Optimal Design of Tuned Inductive Choke,” Energies, vol. 17, no. 20, 2024, 1-15.

[20] Q. Cai, R. Yang, and K. C. Y. Shen, “A modified Salp Swarm Algorithm for parameter estimation of fractional-order chaotic systems,” Int. J. Mod. Phys. C, vol. 34, no. 10, 2023, 1-15.

[21] S. Tadigotla and J. K. Murthy, “Energy aware multiobjective levy flight artificial rabbits optimization based clustering and routing for mobile wireless sensor networks,” J. Ambient Intell. Human. Comput., vol. 15, no. 12, 2024, 4023-4041.

[22] B. Revathi, S. K. K. Elizabeth, P. Nagaraj, S. S. Birunda, and D. Nithya, “Particle Swarm Optimization based Detection of Diabetic Retinopathy using a Novel Deep CNN,” 2023 Third International Conference on Artificial Intelligence and Smart Energy (ICAIS), 2023, 998-1003.

[23] S. S. Krishnegowda and H. P. Periapandi, “Optimal coding unit decision for early termination in high efficiency video coding using enhanced whale optimization algorithm,” Int. J. Electr. Comput. Eng. (2088-8708), vol. 13, no. 6, 2023, 6378.

[24] M. Sakib, S. Ahmad, K. Anwar, and M. Saqib, “Optimizing support vector regression using grey wolf optimizer for enhancing energy efficiency and building prototype architecture,” Cluster Comput., vol. 28, no. 1, 2025, 1-25.

[25] N. R. Bhardwaj, A. Atri, U. Rani, and A. K. Roy, “A Logistic Regression Model for Predicting Sclerotinia Stem Rot in Egyptian Clover (Trifolium alexandrinum L.),” Legume Res., vol. 47, no. 1, 2024, 99-105.

[26] S. K. Patel, J. Surve, V. Katkar, J. Parmar, F. A. Al-Zahrani, K. Ahmed and F. M. Bui, “Encoding and Tuning of THz Metasurface-Based Refractive Index Sensor With Behavior Prediction Using XGBoost Regressor,” IEEE Access, vol. 10, 2022, 24797-24814.

[27] A. Li, L. Niu, and Y. Zhou, “Prediction method of construction land expansion speed of ecological city based on BP neural network,” Int. J. Environ. Technol. Manag, vol. 25, no. 1/2, 2022, 108-121.

Notes

*

Research

article

Author notes

a Corresponding author. E-mail: zhewuwz@outlook.com

Additional information

How to

cite this article: Z Wu, “Management

of Supply Chain Finance Business Operations, Considering Credit Risk Evaluation” Ing. Univ.

vol. 30, 2026. https://doi.org/10.11144/Javeriana.iued30.mscf